Asian Indices:

- Australia's ASX 200 index rose by 43.6 points (0.6%) and currently trades at 7,294.40

- Japan's Nikkei 225 index has fallen by -82.58 points (-0.31%) and currently trades at 26,735.47

- Hong Kong's Hang Seng index has fallen by -512.7 points (-2.38%) and currently trades at 20,988.53

- China's A50 Index has fallen by -115.58 points (-0.85%) and currently trades at 13,508.77

UK and Europe:

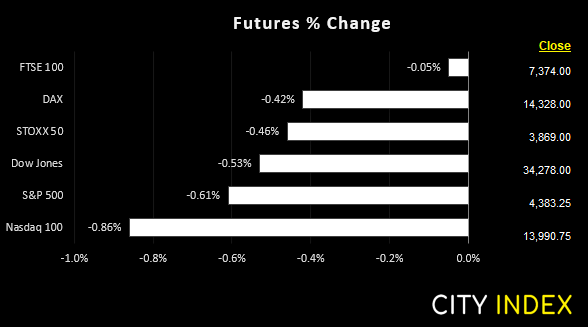

- UK's FTSE 100 futures are currently down -3.5 points (-0.05%), the cash market is currently estimated to open at 7,381.84

- Euro STOXX 50 futures are currently down -17.5 points (-0.45%), the cash market is currently estimated to open at 3,867.82

- Germany's DAX futures are currently down -68 points (-0.47%), the cash market is currently estimated to open at 14,320.06

US Futures:

- DJI futures are currently down -181 points (-0.53%)

- S&P 500 futures are currently down -119 points (-0.84%)

- Nasdaq 100 futures are currently down -27 points (-0.61%)

According to the White House Statement, Biden and Xi will discuss “managing the competition between the two countries as well as Russia’s war against Ukraine and other issues of mutual concern”. That is a broad set of topics which potentially covers trade, war and sanctions and could pave the way for tensions between US and China to either thaw or intensify. It remains up for debate as to which side of the fence China is deemed to sit on regarding Russia’s invasion of Ukraine, although it has been publicly denied by China that they received a request for help from Russia. With any luck, Biden and Xi will present a positive, constructive and unified message, which could provide sentiment another boost heading into the weekend if confirmed by both sides after the call.

US index futures are trading lower, seemingly striking a cautious tone ahead of the call. But then again, we’ve seen three solid days of gains and it is not uncommon to see minor retracements against a preceding move ahead of the open.

The ASX couldn’t quite reach our 7300 target today, but I think many traders are just happy the exchange is open without any technical difficulties. But it has closed at a 4-week high, with energy stocks putting on a good show today as they bounced in line with oil prices. And a quick look at the sector suggests it has seen its corrective low and momentum has realigned with its bullish trend.

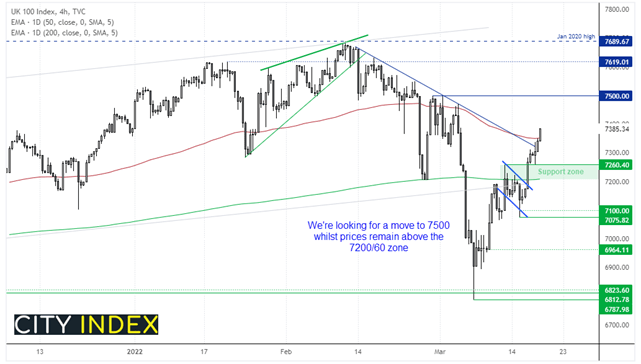

FTSE 100 eyes move to 7500

We’re just over halfway through March and it’s already been the most volatile month in 16. The fact that it has almost recouped most of its initial losses also underscores how it has been a game of two halves.

By yesterday’s close the FTSE has recovered back above its 50 and 100-day eMA, having closed back above the 200-day eMA on Wednesday. Furthermore, it closed at the high of the day and above trend resistance, which is why we have a bullish bias heading into the weekend.

We can see on the four-hour chart it broke out of a consolidation below its 200-day eMA and respected 7260 as support. Whist prices remain above the 7200/60 support zone we favour a run to 7500.

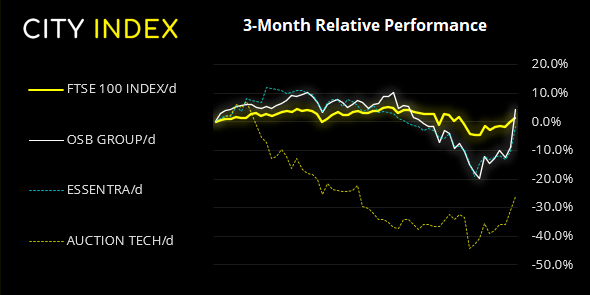

FTSE 350: Market Internals

FTSE 350: 4149.97 (1.28%) 17 March 2022

- 223 (63.53%) stocks advanced and 116 (33.05%) declined

- 2 stocks rose to a new 52-week high, 2 fell to new lows

- 31.05% of stocks closed above their 200-day average

- 56.13% of stocks closed above their 50-day average

- 15.67% of stocks closed above their 20-day average

Outperformers:

- + 14.49% - OSB Group PLC (OSBO.L)

- + 9.98% - Essentra PLC (ESNT.L)

- + 7.27% - Auction Technology Group PLC (ATG.L)

Underperformers:

- -14.09% - Petropavlovsk PLC (POG.L)

- -11.24% - Helios Towers PLC (HTWS.L)

- -8.18% - Ocado Group PLC (OCDO.L)

2-year high for Japan’s CPI

Japan’s consumer prices rose at their fastest pace in 2-years, helped higher by rising food and energy costs. The Bank of Japan (BOJ) kept policy unchanged, which is no surprise that even their 2-year high inflation rate remains significantly below target. The yen was the weakest major and GBP was the strongest although volatility was capped. But with the baulk of economic data of interest now behind us for the week, it was always likely to be a quiet session overnight for currency markets.

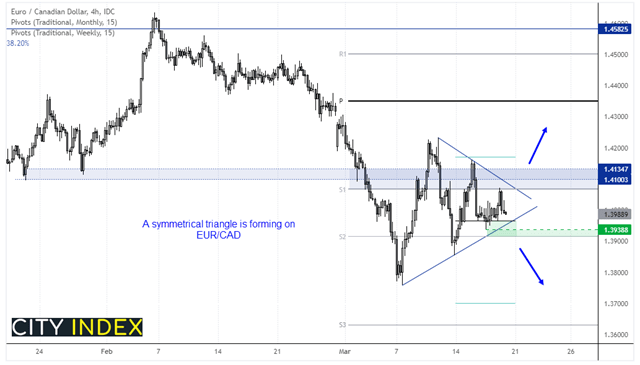

Symmetrical triangle on EUR/CAD

EUR/CAD is coiling up into a triangle formation as volatility subsides after a strong move lower. And that means that we’re no on guard for volatility to erupt once more for a breakout of the triangle. As they’re usually continuation patterns, the bias is for a downside breakout, although we’d want to see prices break below 1.3900 as this would also clear the monthly S1 pivot point. However, that’s not to say they do not breakout counter to the trend, in which case we’d use a break above 1.4100 to confirm a bullish breakout from the pattern. Take note that Canada release retail sales at 12:30, which could provide a news-driven reaction CAD pairs.

Base metals

Gold and silver pulled back from yesterday’s highs but, with no obvious catalyst, we suspect traders are squaring up positions ahead of the weekend. However, base metals are trading higher, as Xi Jin Ping has asked officials to minimise the impact of Covid, but with minimal impact to the economy and people’s lives. This, alongside promise of further stimulus, has given copper and palladium another boost heading into the weekend.

Up Next (Times in GMT)

How to trade with City Index

You can easily trade with City Index by using these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Forex articles

Yesterday 12:17 AM

July 25, 2024 10:39 PM

July 25, 2024 03:59 PM

July 25, 2024 04:37 AM