Asian futures:

- Australia’s ASX 200 index rose by 55.7 points (0.82%) to close at 6,818

- Japan’s Nikkei 225 index has fallen by 135.98 points (-0.46%) and currently trades at 29,544.27

- Hong Kong’s Heng Seng index has risen by 551.12 points (1.89%) and currently trades at 29,646.98

FTSE 100:

- UK’s FTSE 100 futures are currently up 35 points (0.53%), the cash market is currently estimated to open at 6648.75

European futures:

- Euro STOXX 50 futures are currently up 13 points (0.35%), the cash market is currently estimated to open at 3720.72

- Germany’s DAX futures are currently up 51 points (0.36%), the cash market is currently estimated to open at 14090.8

- Dow Jones fell -143.99 points (-0.46%) to close at 31,391.52

- S&P 500 fell -31.53 points (-0.81%) to close at 3,870.29

- Nasdaq 100 fell -252.2 points (-0.19%) to close at 13,059.949

Indices broadly higher overnight

Europe is set for a positive open after sentiment remained buoyant overnight. The Hang Seng was a top performer with financials, consumer cyclicals and energy leading the pack whilst consumer non-cyclicals and healthcare were the only sectors in the red. The daily chart produced a bullish inside day and prices have remain above their 50-day eMA.

Australia’s stronger-than-expected GDP report bolstered the ASX 200 which was led higher by materials and financials, although all other sectors underperformed the index. Information technology was the biggest laggard and traded -1.6% for the session.

The Nikkei has been an underperformer in Asia and trades effectively flat. But whilst it holds above 28,980 then the bias remains for momentum to realign with its dominant bullish trend in due course.

Index futures across Europe and North America are also tracking sentiment higher with Nasdaq and STOXX 600 futures currently taking the lead.

Oil prices stabilise on vaccine progress

Joe Biden claims the US will have enough vaccines for all American adults by May. And the combined forces of rivals Johnson and Johnson and Merck & Co, alongside Biden’s implementation of the Defence Production Act, could very well expediate the vaccination’s rollout. And that should bode well for oil prices as demand could rise sooner than expected.

Oil prices are trading slightly higher after three consecutive bearish sessions. WTI has found support at its 20-day eMA and remains above its prior swing of 58.58 on the daily chart. Brent is slightly lower for the session but also holding its 20-day eMA.

Australian GDP Points to V-Shape Recovery

Australian GDP blew past expectations, rising 3.1% in Q4 verses 2.5% expected. Whilst it’s a tad lower than Q3’s 3.3% we doubt the RBA will complain given parts of Australia went back into lockdown in the second half of December.

The rise was driven mostly by household spending and recent data such as manufacturing PMI, retail sales and employment point towards a strong start for 2021. The RBA currently expect growth to average around 3.5% this year. And they may just get that at this rate.

China Services PMI slips

The service PMI expanded at its slowest rate in 10-months over February, with the employment index contracting at 47.9 as businesses cut back on staff expenditure. As it’s the first contraction in 6 months the weaker figure cannot be fully attributed to temporary businesses closures over Chinese New Year. So, unless we see employment bounce back soon then perhaps it could be part of a slowdown in China. Still, the average of January and February’s headline PMI sits around 51.75, but the world will be watching to see if incoming data and subsequent PMI reports edge closer to that 50 threshold.

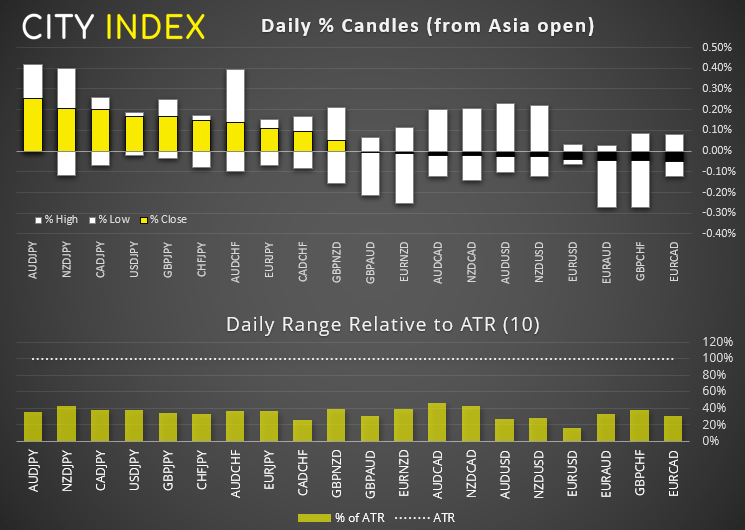

Forex: GBP and EUR defend their lows

Several clues point towards the potential for US dollar weakness today; higher index futures, AUD and JPY are stronger whilst JPY is weaker, and several majors printed single candle reversals yesterday (and not in the dollar’s favour!).

USD/CHF reached out 0.9200 target overnight, although its shooting star below 0.9107 resistance warns of bullish fatigue. And if prices break beneath yesterday’s low it will also take out the 200-day eMA, which increases the odds of a correction from a technical standpoint. We would only be interested in long positions above 0.9207.

EUR/USD produced a bullish hammer with a failed break below 1.2000. Given the significance of this level and reversal patterns elsewhere, we expect 1.2000 to hold over the coming session/s. A bullish hammer also appeared on GBP/USD and closed above its 20-day eMA, making it of interest to bullish swing traders.

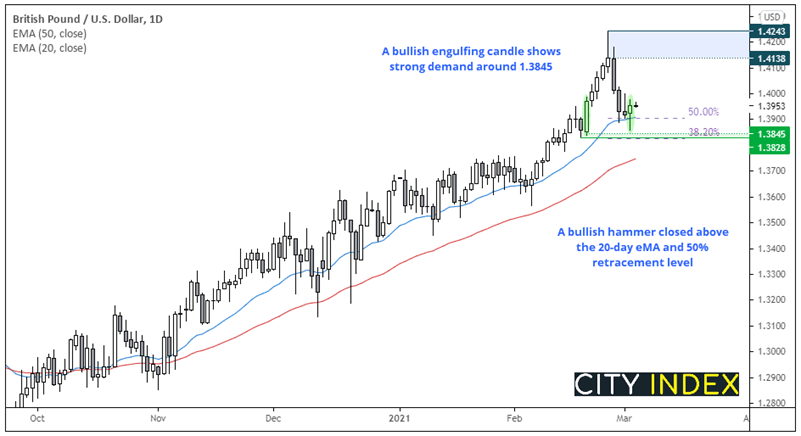

GBP/USD: Its swing low could be in place

The daily chart remains within a strong bullish trend despite its bout of bearish volatility from its multi-year highs. Following two days of turbulence, an inverted hammer and bullish hammer formed on the daily chart, both of which closed above the 20-day eMA and 50% retracement level.

The bullish hammer low also failed to test 1.3845 support, which can be seen as a sign of strength for bulls. This level also coincides with a 38.2% Fibonacci ratio.

- Bulls could wait for a break above the bullish hammer to assume bullish continuation

- An alternative approach is to use limit orders within yesterday’s range to enter on dips. This increases the potential reward to risk, but is also a risker entry

- A break below 1.3828 invalidates the bullish bias

- The 1.4138 – 1.4243 highs are the next major resistance zone, making them a viable bullish target

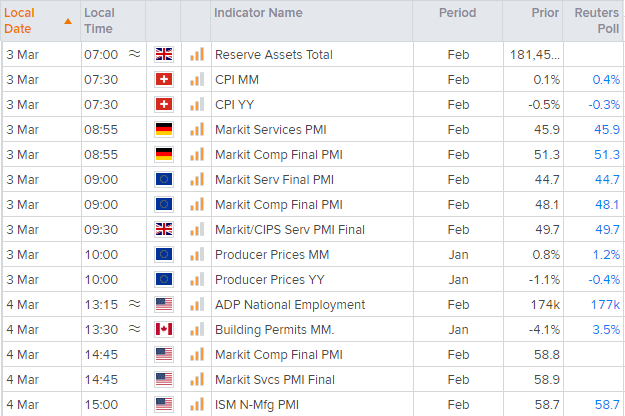

Up Next (Times in GMT)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Markit release their service PMI and composite PMI reports (manufacturing and Services combined) for Germany, the Euro Zone and US later. Given the positive tone set by manufacturing data this week, firmer data from services should further boost sentiment as it paints a picture of a broader recovery. However, with Germany and Euro Zone PMI firmly within contraction territory then this may be an outside chance. Therefore, a more volatile response may be seen if services drag the composite reads down towards (or below) 50.

At 14:00, BOE policymaker Silvana Tenreyo takes part in a discussion on negative interest rates co-hosted by IMF and University of Frankfurt.

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Equities articles

June 8, 2024 02:00 AM

June 3, 2024 05:56 AM

June 3, 2024 03:34 AM