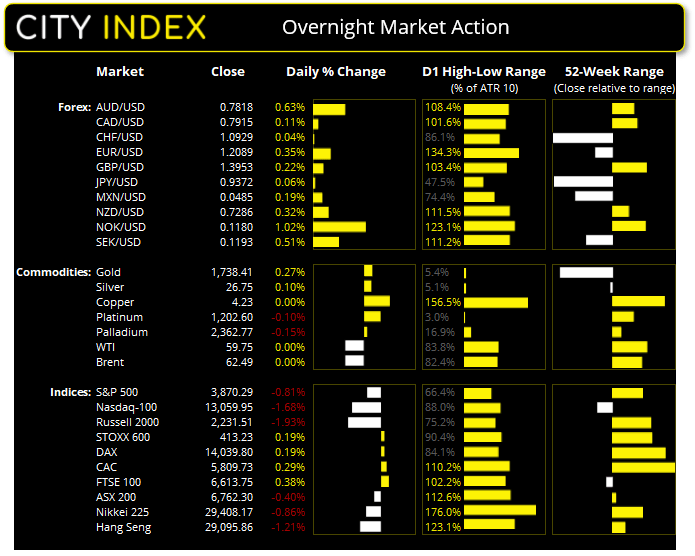

Asian futures:

- Australia’s ASX 200 futures are currently up 60 points (0.888%), the cash market is currently estimated to open at 6,849.6

- Nikkei 225 futures are currently up 270 points (0.91%), the cash market is currently estimated to open at 29,933.5

- Heng Seng futures are currently up 140 points (0.48%), the cash market is currently estimated to open at 29,592.57

FTSE 100:

- FTSE 100 futures are currently up 138.5 points (2.15%)

European futures:

- Euro STOXX 50 futures are currently up 84 points (2.32%)

- Germany’s DAX future are currently up 267 points (1.94%)

- France’s CAC 40 futures are currently up 109 points (1.91%)

Monday US close:

- The Dow Jones index rose 603.14 points (1.95%) to close at 31,535.51

- The S&P 500 index rose 90.67 points (2.379072%) to close at 3901.82

- The Nasdaq 100 index rose 81.84 points (0.63%) to close at 13282.953

China’s manufacturing PMI was the one which bucked the trend with a softer expansion, falling to 50.9 down from 51.5 prior and missing forecasts of it to stay flat at 51.5. Although markets appeared to take this within stride given the report covered Chinese Lunar New Year as many businesses were closed. A ‘back of the envelope’ calculation is to average the January (51.5) and February (50.9) data as it accounts for the rise in business ahead of the holiday. This means the proxy-PMI could sit around 51.2 which, whilst still softer, not as close to the contraction threshold of 49.9. But, if we get a weak print in March (particularly if it contracts below 50) then expect risk-off fireworks to emerge across markets.

Elsewhere, Japan’s manufacturing PMI rose to a 2-year high of 51.40 (up from 50.6), Australian PMI rose to a near 3-yer high of 58.8 (55.3 prior), Germany and the broader Euro Zone PMI’s rose to 60.7 and 57.9 and the UK’s PMI rose to 55.1 (54.9 prior). All the above beat expectations.

And the ISM manufacturing report didn’t disappoint either. At 54.4, the headline index is its highest since May 2004. Prices paid (inflationary proxy) are at their highest level since June 2008, the employment index rose to an 11-month high of 54.4 and new orders rose to 64.8. All in all, not a bad report for Biden’s first full month as President.

Indices broadly higher on improved sentiment

It was a broad rally for equities across all regions. The Russell 2000 led Wall Street higher with a 3.4% rally, the Nasdaq 100 rebounded from 17,755 support to close +2.8% and the S&P 500 is back above 3,900 with a +2.5% gain. All three have produced morning star reversal patterns on the daily chart which are 3-bar bullish reversals. It was a similar story across Europe with the DAX and STOXX indices rebounding back above their 50-day eMAs and the CAC trading back above its 10-day eMA and just below its 2021 high. Structurally the FTSE 100 is less impressive and remains within Friday’s bearish candle with no clear directional bias present on the daily chart. The ASX 200 is set to open higher around 6,849 and take Wall Street’s lead.

Forex: Risk-on - sustained

The classic risk-on pattern seen in Asia yesterday persisted through to the European and US sessions, with commodity FX (AUD, NZD and CAD) being the strongest majors of the overnight session and CHF and JPY the weakest.

AUD/CHF was the strongest cross with a 2% rally and recouped most of Friday’s losses, EUR/AUD was the weakest with a -1.3% decline and all CHF pairs exceeded their 10-day ATR to show. USD/CHF is over halfway to our 0.9200 target outlined in yesterday’s Asian Open report, although prices are now meandering around its 200-day eMA. A break beneath the hourly low of 0.9119 removes it from the watchlist.

The US dollar was slightly higher with DXY (US dollar index) gaining 16 pts (+0.18%) and EUR/USD finding some stability above the 1.2000/23 support zone. GBP/USD moved in line with our bearish bias outlined in yesterday’s European Open report, although the move lacks momentum which leaves the potential for a bounce from current levels.

Commodities: Gold remains unloved

Gold (XAUUSD) remains anchored to Friday’s low and currently trades around 1,722. Bulls failed to hold onto an early rebound and found resistance near Thursday’s low around 1,759 before rolling over. The most positive outcome is it is currently holding above Friday’s low. The next major support level (bearish target) is around 1,700.

Oil prices continue to retrace and fell to a 5-day low ahead of Thursday’s OPEC+ meeting. WTI futures are back below their 10-day eMA and currently trade around 63.39 whilst Brent futures are at 63.40. Still, the retracements appear orderly and of no major concern (yet) given the strength of the bullish moves over recent months.

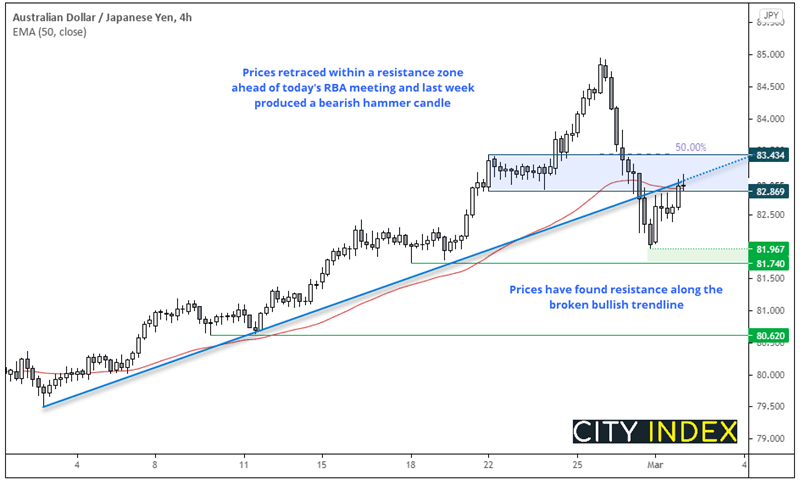

AUD/JPY: Drifts into resistance zone ahead of RBA meeting

It’s no secret the AUD pairs have enjoyed an almighty ride since their March lows. Yet with AUD/USD faltering at 80c last week and AUD/JPY printing a bearish hammer which failed to hold above the December 2018 high, we are on guard for near-term losses as part of a corrective phase. Besides, one must wonder at which point the RBA start discussing their higher currency level with conviction again.

Whilst yesterday produced a risk-on session for AUD/USD, its range remains engulfed by Friday’s bearish candle. And we can see on the four-hour chart that prices have traded in a corrective manner into a resistance zone around the 50-bar eMA and crawling up the broken trendline.

- Bears could seek a candle close (15 in, 30 min, hourly etc) below 82.86 to assume a swing trade short is underway. The more bearish the close the more conviction the potential swing high has.

- Initial target is the lows around 81.74/97

- The bias remains bearish below 83.43, although the broken trendline

Up Next (Times in AEDT)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

The RBA’s (Reserve Bank of Australia) meeting is the main event in today’s Asian session. Although they are expected to hold rates at 0.1% and reiterate caution over a return to policy normalisation. Should they take a firmer stance on the rise of AUD then perhaps we could see the Aussie finally come under pressure. We will also be interested in any commentary surrounding their increased bond purchases this week which saw them double the programme from $2 billion to $4 billion.

South Korean data warrants a look because any weakness here can prelude global growth, particularly if we are to see a surprise contraction with their PMI data. Yet a positive data set could maintain the positive sentiment seen overnight.

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Indices articles

July 25, 2024 01:30 PM

July 25, 2024 01:01 AM

July 25, 2024 12:41 AM

July 24, 2024 07:26 PM