When will Snap release Q3 earnings?

Snap is scheduled to release third quarter earnings after US markets close on Thursday October 20. A conference call will be held on the same day at 1400 PT, or 1700 ET.

Snap Q3 earnings consensus

Wall Street forecasts Snap will deliver a 6.3% year-on-year rise in revenue to $1.13 billion in the third quarter and that it will report a diluted loss per share of $0.25, wider than the $0.05 loss seen the year before. The adjusted loss per share is estimated to come in at $0.03 and turn from a $0.17 profit last year.

Snap Q3 earnings preview

Snap CEO Evan Spiegel admitted that the company failed to deliver in the last quarter and that its results, which saw revenue growth stall to its slowest rate on record and its profitability eroded, did not ‘reflect our ambition’.

That raises the pressure to impress the markets this week, which did not welcome the last set of earnings and sent shares back toward their pandemic-induced lows we saw back in March 2020. The stock has plunged 35% since its last quarterly results out in July.

Snap has said it had already started to implement change to reaccelerate revenue growth by investing in its direct advertising business and by finding new sources of income to diversify its revenue and pursue new growth opportunities – but investors won’t reward Snap until they see evidence this is working. The fact revenue growth is expected to slow further in both the third and fourth quarters suggests it has a big job on its hands to reassure investors.

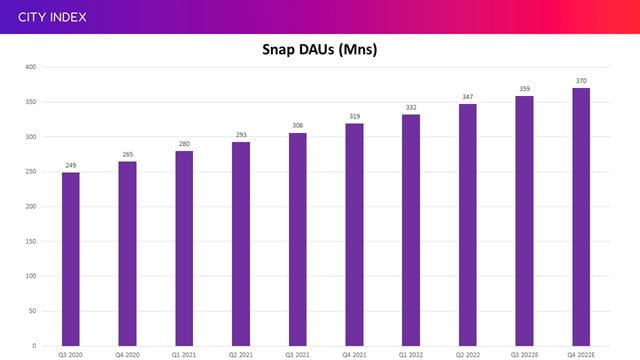

Snap is expected to add 11.6 million Daily Active Users (DAUs) in the third quarter and end the period with 358.6 million of them on its platform. That will be the fewest quarterly additions in two years and markets think it will add even fewer subscribers in the fourth quarter of 2022:

Snap is expected to grow users across all regions, albeit at very different paces. Of the 11.6 million additions, just 900,000 of them are forecast to come from North America, 1.4 million from Europe and the remaining 9.6 million will come from newer markets in the Rest of the World segment.

Revenue growth has stalled because of the slower rate of user additions and because the amount of revenue it earns from each user has also come under pressure, with analysts forecasting average revenue per user (ARPU) of $3.18 this quarter, down 9% from last year. Advertisers have become more cautious and pulled back on spending amid the weaker economic outlook and rampant inflation – which is likely to get worse before it gets better as a recession emerges on the horizon.

‘In certain high-growth sectors, businesses are reassessing investment levels amid the rising cost of capital, which is further reflected in campaign budgets and the level of bids per action,’ Snap said in the last quarter.

Meanwhile, competition for younger users versus the likes of TikTok remains rife, and Apple’s IDFA changes introduced last year – which has made it harder for social media platforms to track online behaviour and target ads – has also shifted marketing dollars elsewhere.

The main weapon being wielded in the fight to revive growth is Snapchat+, a paid subscription service that offers exclusive features and new tools before being released to the wider market. The service was launched in June, and it took less than two months for it to attract its first million subscribers. That was back in mid-August and investors will be keen to see how many more subscribers it has secured since that last update.

Meanwhile, its bottom-line is succumbing to the slower topline growth twinned with rising costs. The amount it is paying for the upkeep of the vital infrastructure that keeps Snapchat going and the figures being returned to content producers through its revenue-sharing mechanism are both rising and overall cost of revenue will be up 4% compared to last year. However, the brunt of rising costs is hitting operating expenses, which are expected to be over 20% higher than last year as the cost of everything from marketing and R&D to everyday G&A expenses continues to rise – enough so that Snap has sunk into the red this year.

Snap has already put the brakes on hiring as part of a broader effort to get a grip on costs. It announced in late August that it was cutting around 6,400 jobs, representing around 20% of its workforce. It has also discontinued its investment in its array other activities beyond the core Snapchat app, from its shows and series created under ‘Snap Originals’ and gaming to its new flying camera drone name Pixy and its social mapping app Zenly. Reports suggest Snap is aiming to cut annualised content and operating costs by $500 million compared to what we saw in the second quarter, so investors will be keen to see early signs that costs are heading in the right trajectory.

It is worth noting that the comparative figures in the third and fourth quarters will be easier compared to what we saw in the first half – although still tough considering revenue jumped 52% and EPS rose 17-fold in the third quarter of 2021.

Where next for SNAP stock?

Snap shares have drifted between a narrow band capped by a ceiling of $12.65 and a floor marked by the 28-month low of $9.40 that was first hit in late July and again in early October. We are waiting for the stock to breakout of this range to signal where it will head next, with $11 currently acting as an intermediary level of resistance that needs to be recaptured before it can target that $12.65 ceiling.

A break above the ceiling will open the door to potentially sharper jumps, first to the $15.50 level of resistance we saw throughout May and June and then to $21 to close the gap created four months ago. We could see the stock target $18, the high of May 2020, on the way up.

That could be a struggle according to the 43 brokers that cover Snap, which have an average target price of $15.39. That implies there is over 40% potential upside from current levels, although this has experienced a dramatic drop from over $26 just three months ago.

The 28-month low has held firm for the last three months and it needs to stay that away to avoid opening the door to the pandemic-induced low of $7.90 seen back in March 2020.

How to trade Snap stock

You can trade Snap shares with City Index in just four easy steps:

- Open a City Index account, or log-in if you’re already a customer.

- Search for ‘Snap’ in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Or you can try out your trading strategy risk-free by signing up for our Demo Trading Account.

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Snap articles

February 1, 2023 01:31 PM

January 26, 2023 01:19 PM

October 18, 2022 03:11 PM

July 22, 2022 01:21 PM