US futures

Dow futures +0.06% at 32946

S&P futures +0.06% at 4173

Nasdaq futures +0.05% at 14342

In Europe

FTSE +0.17% at 7350

Dax +0.70% at 14800

- Stocks steady after gains yesterday

- Federal Reserve begins its two-day meeting

- Tesla extends losses on demand worries

- Middle East worries offset weak China data

Stocks steady after yesterday’s gains

U.S. stocks are set to inch quietly higher after gains from the previous session as investors’ attention turns to the start of the Federal Reserve's two-day monetary policy meeting and as US earnings continue to roll in.

Despite gains at the start of this week, US equities are on track to book their third straight monthly loss, with the S&P500 and Nasdaq set for their worst October since 2018. Rising U.S. Treasury yields and concerns over the Federal Reserve keeping interest rates high for longer hit demand for equities over recent months.

Today, treasury yields have slipped further from last week’s 16-year high. The 10-year treasury yield fell to 4.82% after the Treasury Department said it will borrow less this quarter than expected. When yields full equities often rise.

The Federal Reserve begins its two-day monetary policy meeting, where it's expected to leave interest rates unchanged. The focus will be on commentary at the end of the meeting, which will help the market assess the future path for interest rates and could provide further clues as to whether the Fed intends to hike again, given recent signs of resilience in the US economy.

US consumer confidence data is also set to be released and is forecast to ease to 100 from 103, a four month low as high interest rates and petrol prices hurt sentiment.

Earning season has provided some reason for investors to remain buoyant, with 77.7% of the 250 companies that have reported so far beating analysts’ estimates.

Corporate news

Pinterest is set to rise 16% on the open after the platform posted better-than-expected Q3 results thanks to improved monetization of its international users on its platform.

Tesla is set to fall a further 1% on the open, extending yesterday's 5% losses after the EV maker's key supplier Panasonic announced that it cut automotive battery production, fueling worries of a global slowdown in EV sales.

BP ideas are falling 3% ahead of the open after the oil major missed profit expectations due to weak gas results.

Pfizer will be in focus after the drugmaker posted its first quarterly loss since 2019, mainly owing to charges relating to its covert products.

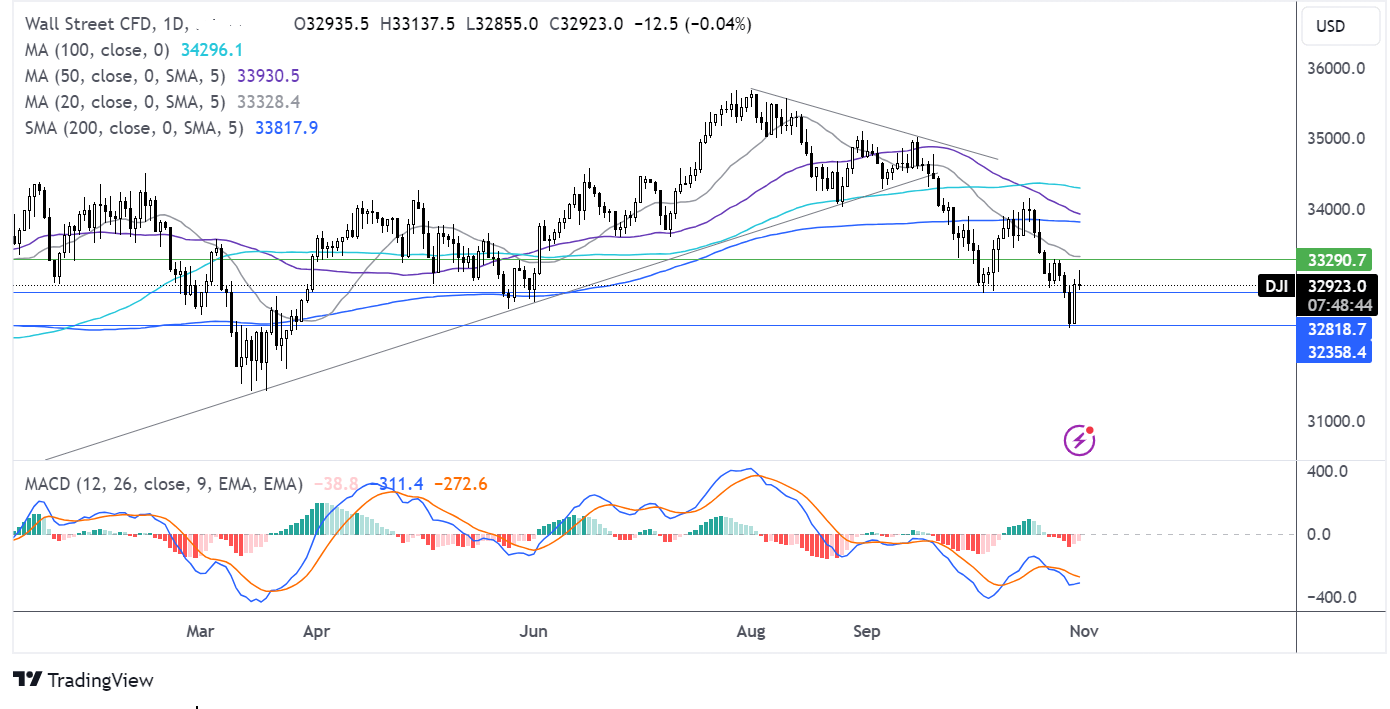

Dow Jones forecast – technical analysis.

The Dow Jones has rebounded from 32320, the October low, retaking resistance at 32800, which, combined with the receding bearish bias in the MACD keeps buyers hopeful of further upside. Buyers will look to rise above 33330 the 20 sma and last week’s high, to negate the near-term downtrend and expose the 200 sma at 33800. Sellers will look to test support at 32800 to bring 32320 back into focus.

FX markets –USD rises, EUR rises

The USD is rising as employment cost data shows that wage growth was ahead of forecasts. The Federal Reserve interest rate decision is tomorrow, where the Fed is widely expected to leave rates on hold.

EUR/USD is rising despite the eurozone economy unexpectedly shrinking in Q3 by 0.1% after growth of 0.2% in Q2. Meanwhile, inflation cooled by more than expected to 2.9% in October, down from 4.3%. The data is helping the euro move higher as concerns of stagflation in the region ease.

GBP/USD is falling after industry data from the British Retail Consortium showed that inflation in British store chains rose at the slowest pace in over a year. Annual shop price inflation cooled to 5.2% from 6.2%, its weakest since August 2022. The data supports the view that the Bank of England could keep interest rates on hold when they meet on Thursday.

EUR/USD +0.41% at 1.0658

GBP/USD -0.07% at 1.2178

Middle East worries offset weak China data

Oil prices are steadying after a 3% fall in the previous session as concerns over supply and an escalation of the conflict in the Middle East are offset by weak Chinese data.

Oil prices are being supported by an escalation of the Israel–Hamas conflict. While Middle East developments have yet to affect oil supply, as the ground invasion intensifies, the risk of involvement from Iran rises.

Meanwhile, oil gains are being capped by disappointing data from China, which showed weaker-than-expected manufacturing and non-manufacturing PMIs, fuelling fears of slowing demand in the world's largest oil importer.

Chinese manufacturing activity contracted while non-manufacturing activity growth slowed substantially. The data suggests that the recent support measures from Chinese authorities have been insufficient.

Attention now turns to API weekly crude stockpile data.

WTI crude trades +0.5% at $82.61

Brent trades +0.5% at $86.87

Looking ahead

14:00 US consumer confidence

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest US Open articles

Yesterday 01:32 PM

July 25, 2024 01:17 PM

July 24, 2024 01:43 PM

July 23, 2024 01:38 PM