December 16, 2021 3:06 PM

*This article is part of our 2022 Global Market Outlook collection, where we highlight the key themes, trends, and levels to watch on our most traded products. We’ll be publishing these reports to our pages from December 13-20, so please visit the official 2022 Outlook hub page to see the whole collection!

2021 in Review

2021 started positively as the Chinese economy built on the momentum that saw a return to its pre-Covid path in 4Q 2020. After a bumper +18.3% rise in Q1, expectations were for GDP growth of around 10% in 2021 before falling into the 5.5%-6% range in 2022.

In March, a new five-year plan (FYP) for 2021 - 2025 was unveiled at the National People's Congress (NPC) meeting. The plan was broad and addressed all three pillars of development – economic, social, and environmental.

Key action points, the withdrawal of countercyclical fiscal stimulus and initiatives across Manufacturing Upgrading, Urbanization, Reducing Income Equality, and Decarbonization, including the ambitious goal to reach "peak emissions by 2030 and carbon neutrality by 2060."

By May, the Chinese economy was straining under the weight of soaring commodity prices, and the first regulatory reset commenced. A crackdown on anti-trust and fintech companies sparked memories of three previous regulatory crackdowns, the Anticorruption Campaign in 2013-15, Investigation on Conglomerates in 2016-3Q17, and broad Regulatory Tightening in 2018.

In early July, signs that growth and aggregate credit demand had deteriorated prompted the PBoC to deliver a universal 50bps cut to the Reserve Requirement Ratio (RRR). The cut was thought to be enough to put a floor under growth.

In late July, Chinese authorities rolled out another regulatory change, this time in the education sector, turning tutoring companies into not-for-profit organizations. Amid rising market concern, authorities attempted to provide more clarity stating their aim was to strike a balance between social fairness and growth.

The month of August brought regulatory changes restricting foreign investment and a resurgence of the Delta variant across numerous cities and provinces that prompted swift lockdowns under China's Covid-zero policy. Analysts wasted no time revising lower growth forecasts again into year-end.

In September, fears of default by Chinese property developer Evergrande escalated. Evergrande’s woes directly result from Beijing's regulatory crackdown on property developers in late 2020 and efforts to contain house prices.

Further compounding a slide into the final quarter of the year, a "power crunch" as soaring coal prices and efforts to reduce carbon emissions prompted authorities to implement power restrictions. Power outages meant products could not be manufactured or delivered on time.

The effects of multiple regulatory and police crackdowns have weighed on economic growth and caused billions of dollars to be wiped off the market value of public companies in 2021.

A trio of easing initiatives (outlined below) were announced in early December at a Politburo meeting that prioritized stabilizing growth.

- Chinas Central Bank, the PBoC, announced a 50bps broad-based RRR effective on December 15.

- Beijing initiated a managed debt restructuring of developer Evergrande.

- The CBIRC (China Banking and Insurance Regulatory Commission) stated its intention to support both first-home demand and demand for second homes - the first time since 2015 that Beijing offered support for second-home demand.

Outlook for 2022 - The Year of the Tiger

Growth

After leading the world economy out of the Covid Pandemic, the Chinese economy underperformed in the 2nd half of 2021 due to a series of regulatory resets and tight fiscal policy.

The easing measures outlined above should ensure growth returns to between 5-6% in 2022, a target likely to be confirmed at the National People’s Congress in March.

Inflation

PPI surged to 13.5% in October, its highest level since 1995. The rise was fueled by higher raw material costs and factory production cuts, as government restrictions on carbon emissions and soaring coal prices led to power rationing.

The power crunch has since eased, as have commodity prices. And with minimal pass-through evident from PPI into consumer prices, CPI is expected to remain below Beijing’s 3% target and may ease back below 2% should food prices continue to reverse lower.

Geopolitics

The goodwill from the recent virtual summit between the two Presidents, Xi and Biden, set the scene for the coordinated release of Strategic Petroleum Reserves in November by oil consuming nations and prompted speculation that tariffs might be removed.

Highlighting the complex nature of the relationship, President Biden's diplomatic boycott of the Beijing Winter Olympics means that a wind-back of tariffs is unlikely until after the games conclude in mid-February.

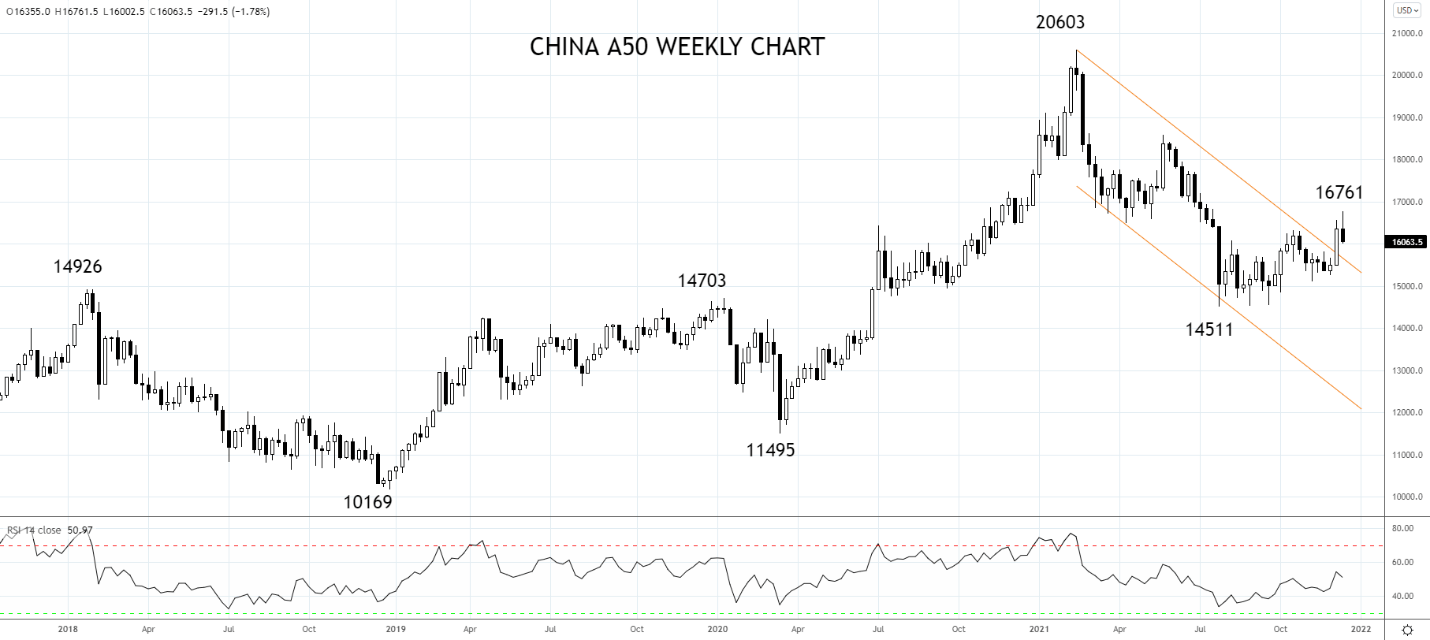

What next for the China A50?

The China A 50 has been among the worst performers in Emerging Markets and in APAC in 2021, falling almost 30% from its peak on February 17 to its low point in July. However, following recent policy easing, the backdrop is improving.

Aided by a rebound in the interest rate-sensitive sectors that account for ~64% of the China A50 index, including Food, Beverage and Alcohol, Banks, Insurance, and Financial Services, the China A50 is set to outperform in 2022.

Technical Analysis

As first observed in an article in October called “China A50 Basing” the correction from the February 20688 high to the late August 14516 low appears complete at the August 14516 low.

“Despite the Evergrande turmoil, the China A50 tested and held the August 14516 low, providing preliminary evidence of basing”.

In early December, the China A50 triggered a bullish break higher from a corrective trend channel before testing medium-term resistance 17,000 area.

Should the China A50 clear resistance at 17,000, the rally would extend towards the May high at 18,575.

Based on this view we favour trading the China A50 from the long side, looking for higher levels in 2022.

Source: TradingView

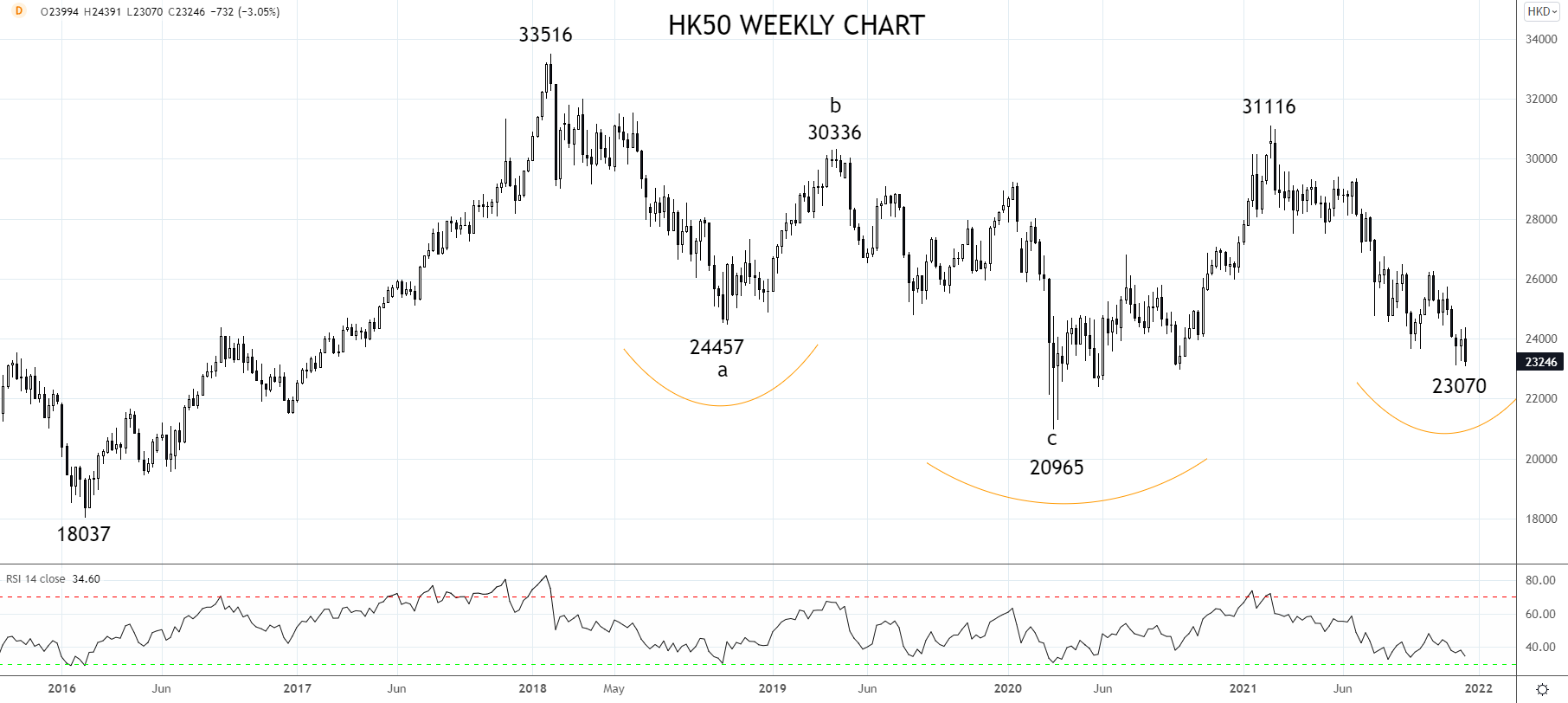

What next for the HK50?

This year, the HK50 is amongst the world's worst performing major stock markets after regulatory resets in China and the Covid-19 pandemic.

Based on the themes already outlined and a border reopening with China, the HK50 is well placed to recover a good portion of its 25% peak to trough fall in 2021.

The HK50 to be bolstered by a rebound in sales from Hong Kong retail names and revenues from Casino operators and high-paying dividend stocks such as AIA Group Ltd and CK Hutchison.

Technical Analysis

The decline from the 2018 33516 high to the 2020 low at 20965 is viewed as a completed three-wave corrective sequence after an impulsive move higher.

More recently, a five-wave decline from the February 2021 31116 high to the 23104 low is noticeable and suggests the HK50 is close to putting in place a bottom.

Providing support at 23000 holds the expectation is for a rebound back towards initial resistance at 26500, with scope for the rally to extend towards the 2021 high at 31116.

Source: TradingView

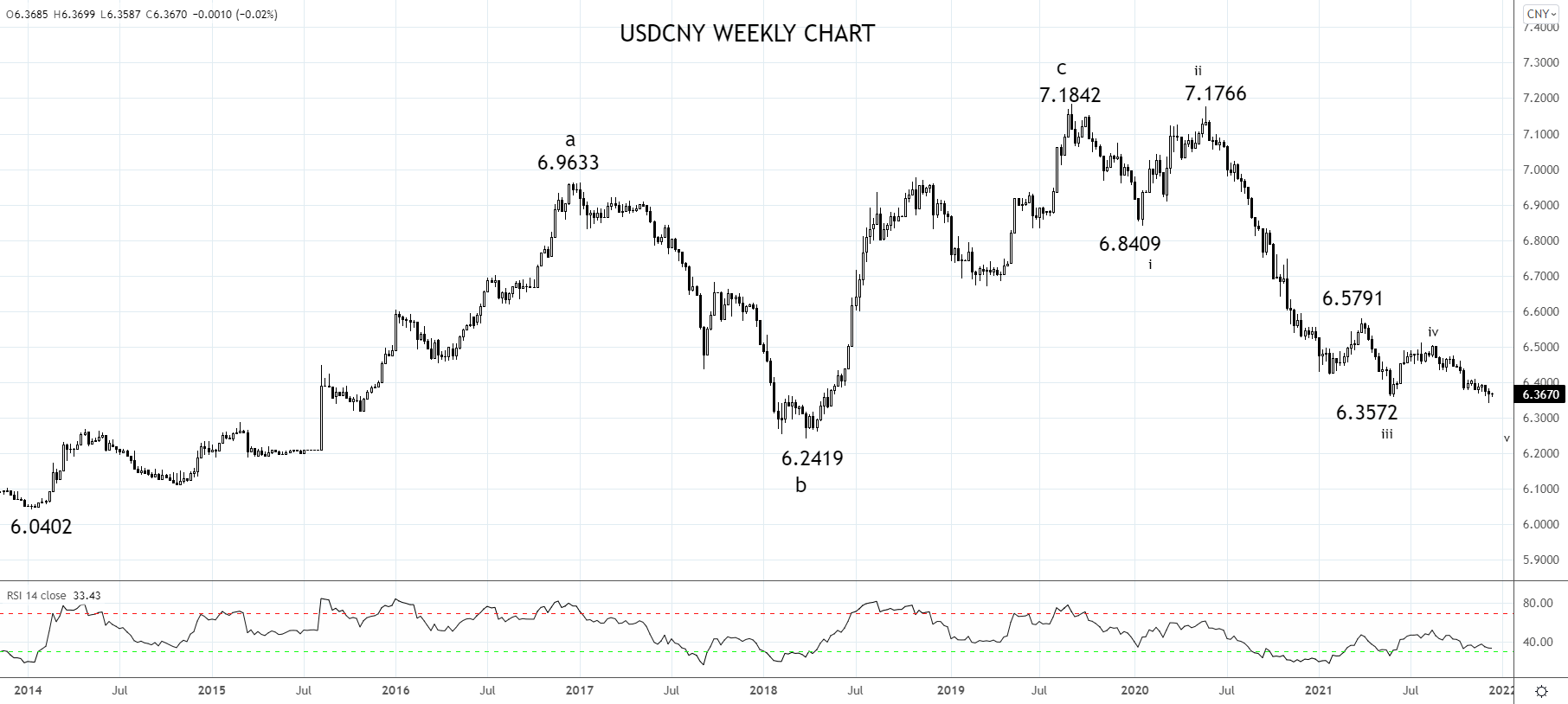

What next for the CNY?

USD/CNY has weathered the volatility of 2021 that included weak data, regulatory resets, and the Evergrande saga while trading in a remarkably tight 3.5% range. Meanwhile, the U.S. dollar index, the DXY, has rallied over 7% year to date.

Supporting the CNY an elevated goods trade surplus, muted services trade deficit, and continued foreign buying of Chinese onshore bonds that offer investors positive real return.

The CNY is expected to continue to outperform in 2022 despite the increasing probability of a faster Fed Taper. Ultimately this means USD/CNY is probably destined for a relatively tight range for the first six months of 2022, between 6.4500 and 6.3000 on the downside.

USDCNY Technical Analysis

USDCNY completed a multi-year three-wave corrective rally from the 2014 6.0402 low at the September 2019 7.1842 high. The high not surprisingly traded during the heights of the U.S. – China trade war.

In May 2020, shortly after the U.S and China signed a trade agreement, an impulsive, almost 10% move lower commenced in USD/CNY before the move lost momentum at the beginning of 2021 as the broader U.S. dollar rally started.

As both the U.S. dollar and the CNY will continue to attract inflows in 2022, further downside is likely to be limited to 6.3000 and, at the lowest, the 6.2419 low from 2018. While bounces are likely to find sellers between 6.4500 and 6.5000.

Source: TradingView

How to trade with City Index

You can trade with City Index by following these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest China A50 articles

June 5, 2024 03:54 AM

June 3, 2024 03:34 AM

May 29, 2024 06:03 AM