- Significant reduction from oil supply should keep downside limited

- Demand concerns overstated

- We think WTI could reach $85 to $90

WTI crude oil hit a fresh post-OPEC high above $81.80 on Tuesday, before sliding more than $1 from there to find itself weaker on the session at the time of writing on Wednesday. However, the path of least resistance remains to the upside following the big price upsurge on the back of the OPEC’s unexpected decision at the weekend. Our WTI forecast is that it will reach $85 to $90 before any serious signs of weakness emerge.

The official US crude oil inventories data from the EIA is due for release later on Wednesday. But this is unlikely to move prices significantly lower, given the privately conducted survey from the American Petroleum Institute (API) on Tuesday showed a large drawdown.

Where does oil go from here?

In the short-term, oil prices are going to be driven more by supply concerns than demand. On the supply front, the big production cuts have fuelled speculation oil prices will reach 2022 levels and provide fresh inflationary jolt to world economy. I, for one, think that the impact of the production cuts could send WTI to at least $85-$90 from here, before we potentially see some real weakness in oil prices again. Any short-term weakness in oil prices could prove to be short lived.

Weakening US jobs data not impacting WTI forecast much

Obviously, a high oil price will hurt demand at a time when household and business finances are overstretched. The thing about oil demand, though, is that it is very price inelastic. So, unless something like Covid happens again, don’t expect to see a material drop in oil prices due to demand weakness. People will not stop driving or travelling by plane because of high oil prices. Therefore, demand is only likely to get hurt moderately by rising oil prices.

This means that the weakness in US jobs data we have seen over the past couple of days, which has revived fears of a slowdown in the US economy, is unlikely to hold oil prices back. Today we saw the employment component of the ISM PMI fall sharply from the previous month’s 54.0 reading but at 51.3 it still remained in the positive territory. On top of this, the ADP Private Payrolls come in at 145K when 210K was expected. On Tuesday, we saw a big 630K drop in US job openings in February.

These weaker employment indicators only add to recession concerns. But it is worth remembering that the jobs market still remains quite healthy. Just look at the recent non-farm payrolls reports. What’s more, despite that large drop in job openings, there are still some 1.67 jobs available for each unemployed US citizen. To give you an idea how this compares to the pre-pandemic levels, when the labour market was considered strong, there were about 1.2 jobs available for each unemployed person in the US. All eyes will now be on the US nonfarm payrolls report on Friday, with the ISM services PMI to come later on Wednesday’s session.

European data improves further

Meanwhile from Europe we saw some surprisingly strong data this morning. German industrial orders jumped by 4.8% in February, recovering sharply since November when recession concerns were at the highest. What’s more, Spanish business activity in both the services and manufacturing sectors improved further in March, and once again beat expectations. Spain's services PMI rose to 59.4 in March, reaching its highest level since November 2021.

With the Eurozone economy proving to remain more resilient than expected, this should reduce concerns over demand in the short-term

What about the longer-term outlook?

While the OPEC+ cuts are expected to tighten the oil market and may well provide further support to prices in the near-term, the longer-term outlook remains uncertain. After all, a side effect of a sustained period of high oil prices will be inflation. This may mean tighter monetary policy will remain in place longer than expected. Even then, it will probably take a proper hard landing of the global economy to cause a severe dent in global oil demand.

Thus, the only way for oil prices to come under significant pressure again is from the supply side of the equation. Specifically, if non-OPEC supply increases sharply. This is possible but will take some time for producers outside of the OPEC+ to ramp up their production. If they ramp oil production so significantly than OPEC+ starts to lose market share again, then this will start another supply war between the OPEC+ and non-OPEC countries such as the US and Canada.

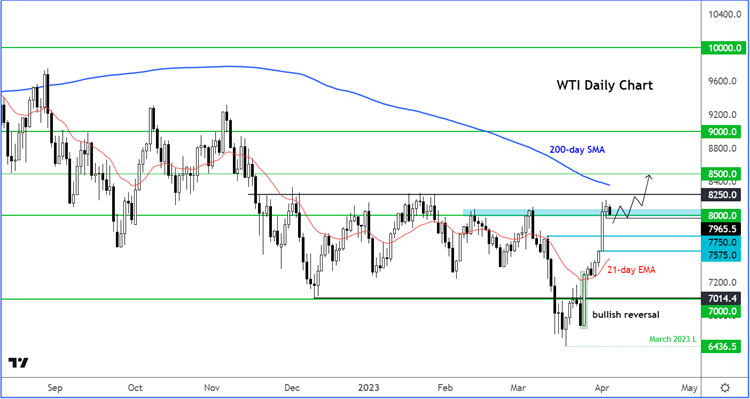

WTI Forecast: Technical Analysis

Bringing the focus back to the short-term, oil traders are now torn between waiting for a proper dip in order to buy oil or chase the market here so that they don’t miss out on further potential gains.

The big gap that was created at the weekend remains largely unfilled. While gaps typically fill, they don’t always. This could be a breakaway gap in oil prices, given the big fundamental impetus that was announced. What oil traders will want to see here is some consolidation around or ideally slightly above the $80 level now. This would give traders the confidence that they need that the market wants to push higher.

Alternatively, if WTI falls to fill most or all of its weekend gap, then, in that case, traders will want to see the formation of a bullish daily candle before looking for fresh long opportunities.

Source: TradingView

ICYMI, here’s what the OPEC agreed on

In case you didn’t read the news, the OPEC+ blindsided the market with a surprise production cut, announced at the weekend. The group agreed to cut nearly 1.7 million barrels of oil per day. The reductions are pledged from next month through year end. Saudi Arabia is again leading the way with 500,000 barrels per day of cuts. Several other Gulf states have joined in with their curbs. Russia, who had already announced a 500k bpd through June, has now extended that through year end.

The OPEC+ decision came totally unexpected. Given that nearly 1.7 million barrels of oil per day will be held back from global supply, this should keep prices supported.

-- Written by Fawad Razaqzada, Market Analyst

Follow Fawad on Twitter @Trader_F_R

How to trade with City Index

You can trade with City Index by following these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest WTI articles

July 25, 2024 05:30 PM

July 18, 2024 12:48 AM

July 10, 2024 03:45 PM

July 9, 2024 05:30 PM