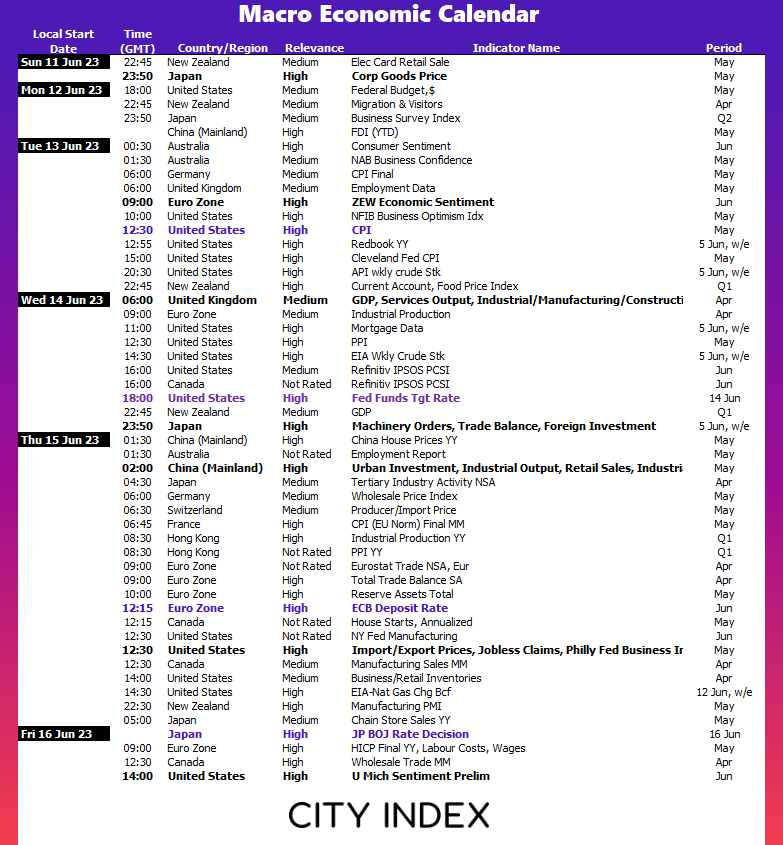

Three mighty central banks release their monetary policy decisions next week, starting with the FOMC meeting on Wednesday. But Tuesday’s inflation report could also carry some clout as it has the potential to move the needle between an anticipated pause to an undesired hike if it surprises too much to the upside. Whilst the ECB meeting on Thursday is the most likely ‘live’ meeting of the three, we’re curious to see how they tackle weak growth, disinflation and what impact (if any) this can have on staff forecasts. And whilst the BOJ are unlikely to change policy, yen traders will be quick to remind you that’s exactly what they want you to think – before they come out with a surprise. So always be on your guard when the BOJ is concerned.

The week that was:

- The RBA hiked their cash rate by 25bp to 4.1%, warning they ‘some further tightening may be required’ –

- It was the second consecutive meeting where they surprised the consensus for a hold

- Citing stubbornly high inflation, the BOC also surprised markets with a 25bp hike to 4.75% (but this may be one and done)

- The combination of RBA and BOC hike saw traders reconsider the potential for the Fed to hike at their July FOMC meeting

- China’s imports and exports continued to slide as demand for goods in general fell, which complemented weak official PMI data form the previous week and further fan concerns for the global growth outlook

- Asian equity markets felt the strain with even the Nikkei 225 forming a bearish engulfing day at its 32-year high, whilst the yuan continued to slide and send USD/CNH to a fresh 7-month high

- The Turkish lira hit a new record low against the US dollar as central authorities loosed their grip of state control and veer towards a free market

- The World Bank increased its growth forecast for 2023, yet lowered it for 2024

The week ahead (calendar):

Earnings This Week

Look at the corporate calendar and find out what stocks will be reporting results in Earnings This Week.

The week ahead (key events and themes):

FOMC meeting

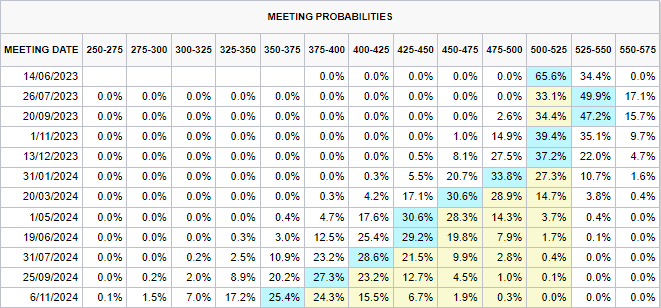

Over the past couple of weeks we have seen market expectations do full circle from pricing in a pause, to pricing in a hike and back again. Whilst some data points could easily warrant a hike (and back up hawkish comments from some Fed members) – others point to a pause. But what tips the scales in favour of another hold next week is that Vice Chair Jefferson backed up comments which alluded to a pause from Powell ahead of the blackout period.

As things stand at the time of writing, Fed fund futures imply a 65.6% chance of a pause next week, or a 34.4% probability of a 25bp hike. Take note that there’s currently a 49.9% chance of a 25bp hike in July or 47.2% chance of one in September.

Of course, another hot NFP print of 283k jobs serves as a reminder that the job market remains tight – even if unemployment rose to a (historically low) level of 3.7%. But perhaps the best proxy for that the Fed decide to do on Wednesday is what happens with Tuesday’s inflation report.

Keep in mind we also have the quarterly staff forecasts, updated dot plot and press conference to look forward too which can sway market opinion after the decision. A typical pattern in recent history is to see markets construe the decision as dovish before the press conference reverses the initial move.

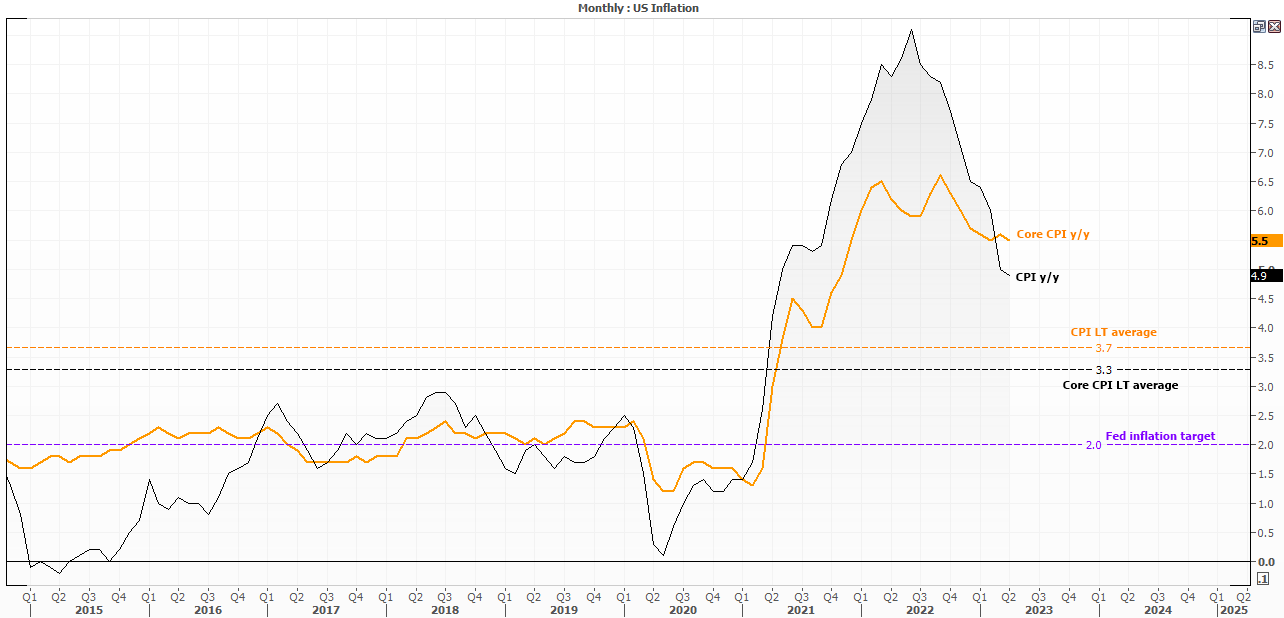

US inflation report

It probably goes without saying that an uncomfortably hot inflation report on Wednesday could tip the scales in favour of another hike, sending the US dollar soaring with yields and weighing on Wall Street, gold and commodity FX. But a more realistic outcome is that inflation will come in or around expectations and show a slight softening whilst remaining elevated by historical standard. The degree (and which side) of expectations it lands upon would then likely see a shift in expectations further our and retain a pause for Wednesday. Of course, what we would all like to see is a healthy drop in inflation which would likely cement a pause, bring forward expectations of the Fed’s cut (slightly) and weigh on the US dollar and yields accordingly.

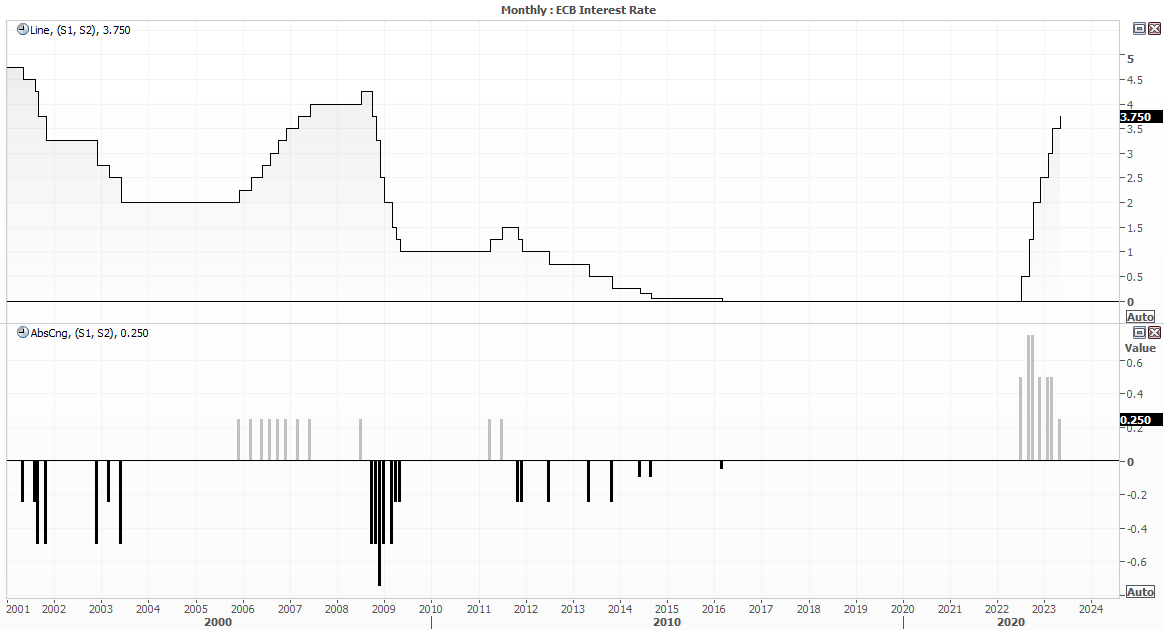

ECB meeting

The consensus is for the ECB to hike their interest rate by 25bp to 4%, which would be its highest level since 2008 and their eighth hike this cycle (followed by another 25bp hike in July). Yet with weaker growth an obvious signs of disinflation, there’s a case that the central bank may not need the multitude of hikes going forward that they have ben touting. Still, that does not mean the ECB will be in any rush to reveal any such viewpoint, especially with the Fed at a 5% interest rate and the likes of the RBA and BOC hiking earlier this week.

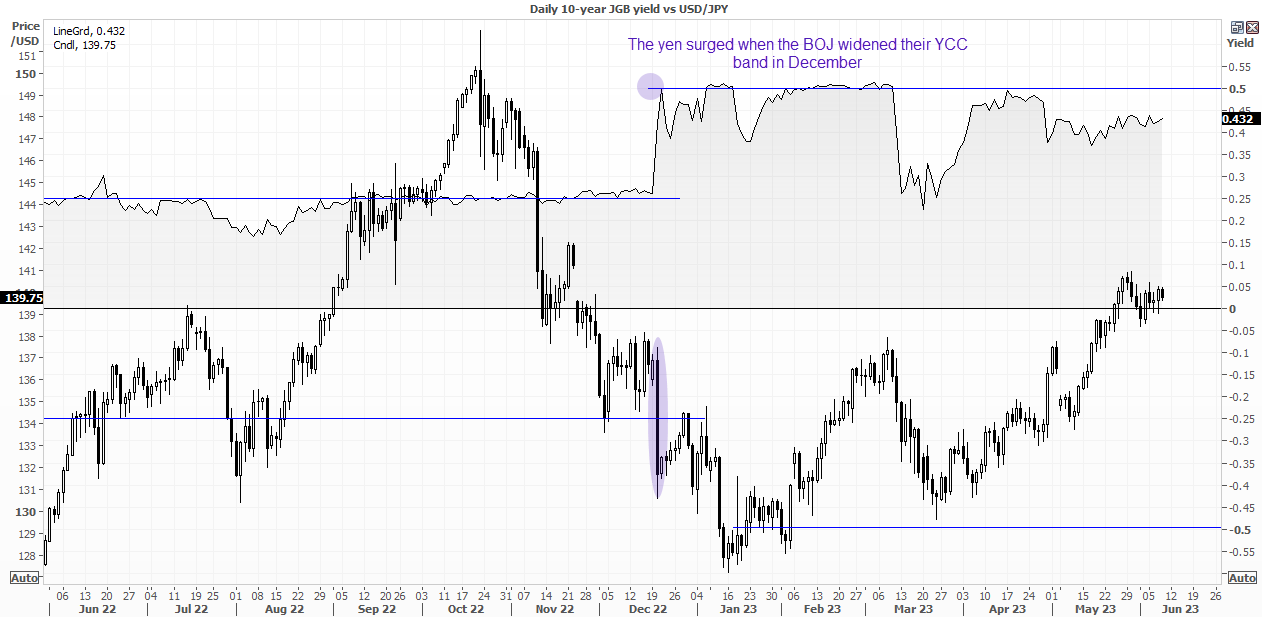

BOJ meeting

In all likelihood, there will be no change to monetary policy form the BOJ at this meeting (or any time soon). But that is not to say we should not ignore the possibility of some action, given their reluctance to provide accurate forward guidance and history of surprising markets every now and then. Commentary he’s remained ultra-dovish from BOJ members, even if inflation has ticked higher.

Interest rates currently remain at -0.1% as they have since 2016, and if they are to change anything it would likely be a wider YCC band, or the abolishment of the policy all together. And that could spur a bout of very strong yen strength (USD/JPY weakness).

-- Written by Matt Simpson

Follow Matt on Twitter @cLeverEdge

How to trade with City Index

You can trade with City Index by following these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the market you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Week ahead articles

Yesterday 04:48 AM

July 19, 2024 06:20 AM

July 12, 2024 01:32 AM

July 12, 2024 01:32 AM