US stocks extend rally but will the Fed spoil the party for bulls

Global equity markets have increased their gains at the start of the week, with European indices closing between 0.3 to 1.6 per cent higher today. […]

Global equity markets have increased their gains at the start of the week, with European indices closing between 0.3 to 1.6 per cent higher today. […]

Global equity markets have increased their gains at the start of the week, with European indices closing between 0.3 to 1.6 per cent higher today. In the US, shares on Wall Street were trading higher at the time of this writing. Sentiment in the stock markets has remained resilient despite a sell-off in the oil market and fresh data showing industrial activity in China slowed down more than expected at the start of the year. Stock market investors seem happy to be picking the dips due to the on-going support from central banks. With interest rates being virtually zero across the developed nations, there are not many asset classes that come with acceptable yields and reasonable degrees of risk.

Indeed, after the initial scepticism over the ECB’s latest stimulus package faded, stocks have rebounded strongly from their Thursday afternoon’s lows. In this regard, it will be interesting to observe how the markets will react to the upcoming policy decisions from the Bank of Japan on Tuesday, the US Federal Reserve on Wednesday and the Bank of England and Swiss National Bank on Thursday. Apart from the SNB, the rest of these central banks are unlikely to make any changes to their policies. But equally important will be the forward guidance from the Fed. If the FOMC hints strongly at the prospects of another rate rise in June then US equities may react negatively. The prospects of marginally higher borrowing costs may discourage investors from buying stocks without a sizeable pullback. In contrast, if the Fed appears to be more dovish than expected then stocks may actually extend their gains. In any event, US markets may soon start to underperform their European peers where the Europe Central Bank has turned even more dovish by the introduction of a beefed-up QE package.

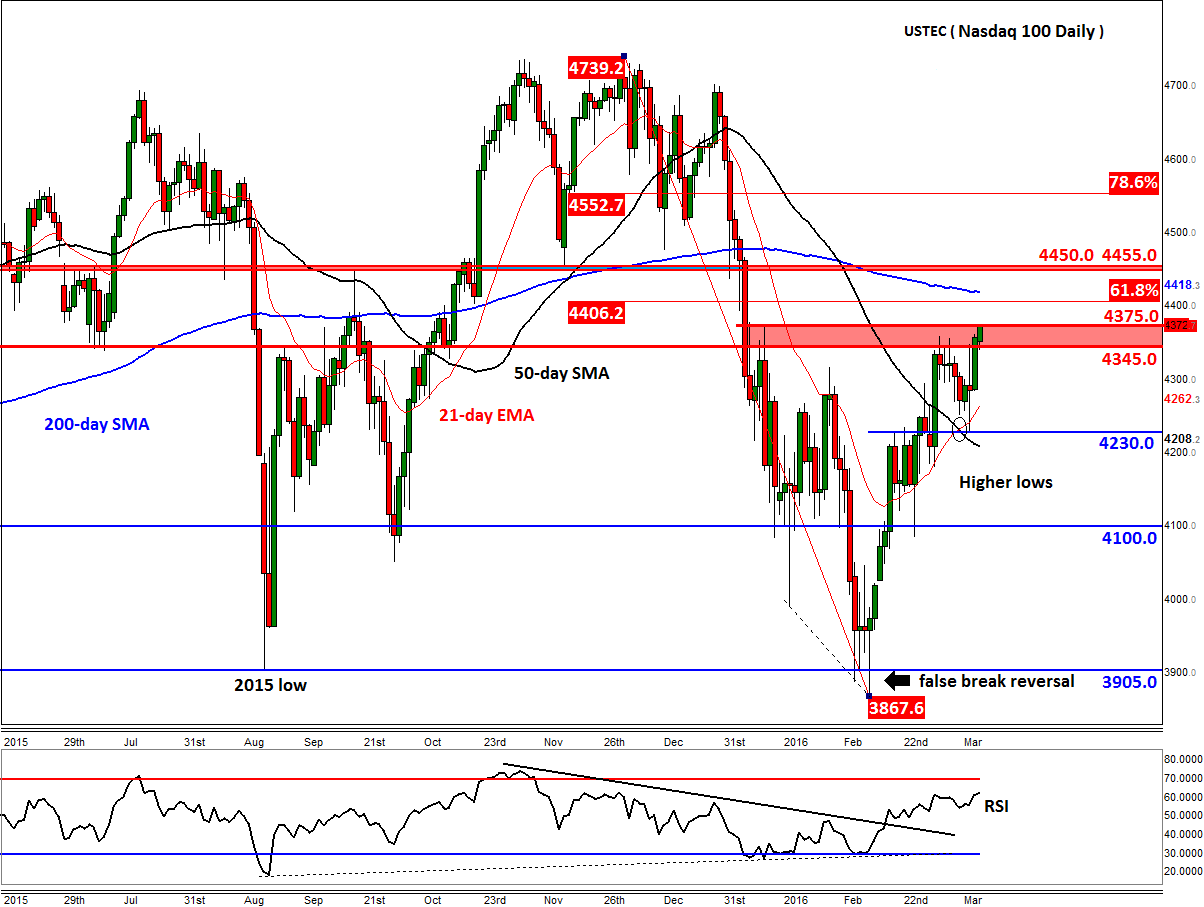

Ahead of the central bank meetings, the technical outlook on US stock indices continues to look constructive, with both the Dow and S&P 500 closing above their respective 200-day moving averages for the first time this year at the end of last week. The Nasdaq 100 however has underperformed somewhat, for it still remains below its own 200 MA. Nevertheless, the underlying price action continues to look constructive for this index too. Ever since it created a false break reversal pattern at 3905 in February, the index has been putting in higher highs and higher lows. Today, the tech-heavy index is trying to climb above the recent range highs of 3445/75 area. So far, it is doing a good job at it but things could change quickly if, for example, oil extends its decline further.

A close above this 4345/75 area, if seen, would strongly point to a continuation of the rally towards the 61.8% Fibonacci retracement at 4406, the 200-day moving average at 4418 or the previous support/resistance level at 4450/55 area. The RSI is still not at the “overbought” threshold of 70, so there may be some juice left in this rally. At this stage, a closing break below 4345 would be deemed a bearish outcome in the short-term outlook. If seen, the Nasdaq 100 could potentially drop back towards Thursday’s lows of around 4230 before deciding on its next move.