Top UK Stocks | Tullow Oil Shares | Redrow Shares | Keywords Shares | Restaurant Group Shares | Trustpilot Shares

Top News: Tullow Oil returns to profit as CFO stands down

Tullow Oil revealed it returned to profit in the first half of 2021 as it narrowed its production guidance for the full year and announced its chief financial officer is standing down in early 2022.

Tullow shares were up 5.8% in early trade this morning at 47.58p.

The oil and gas company said revenue held broadly steady at $727 million in the first half from $731 million the year before. That was despite working interest production rising to 61,200 barrels of oil equivalent per day from 60,000 barrels. Output dropped in Gabon but this was offset by lifts in Ghana, the Ivory Coast and Equatorial Guinea.

Tullow Oil managed to return to a profit after tax at the bottom-line of $93 million, having booked a large $1.32 billion loss last year. That was driven by a significant reduction in exploration write-offs and impairments that plagued results last year.

Free cashflow improved to an $86 million inflow from an outflow of $213 million last year. Tullow said it is expecting annual free cashflow to come in around $100 million based on oil prices staying around the $60 mark. Notably, that guidance includes an anticipated $75 million payment from its partner Total, but warned this could end up being paid in 2022.

Moving forward, Tullow Oil said production over the full year should average 58,000 to 61,000 barrels per day as it narrowed its target toward the top end of its guidance range. It was previously targeting output of 55,000 to 61,000 barrels per day. It said the revision was down to a deferral of work on the Jubilee field and higher output from Simba in Gabon after work on the project was accelerated.

Tullow is describing 2021 as a transition year after launching a new 10-year plan in late 2020, while securing around $2.3 billion of new funding back in May has firmed up the balance sheet.

‘Overall, from 2021-2025, Tullow's business plan will deliver growth in production, reserves and underlying value, along with material cash flow to support deleveraging which will see the group reduce its gearing to below 1.5x by 2025,’ said Tullow.

‘Over the past few months, Tullow has focused on further refining the plan for the 2021-2025 period with a base case capital expenditure of $1.3 to $1.5 billion during this period. This expenditure is self-funded and requires no additional borrowing. Revenues are protected by Tullow's comprehensive prudent hedging programme and the group has flexibility to reduce expenditure in the event of a sustained oil price fall to $55 per barrel or below,’ said Tullow.

Separately, Tullow announced this morning that CFO Les Wood will stand down at the end of March 2022, by when it hopes to have found his replacement.

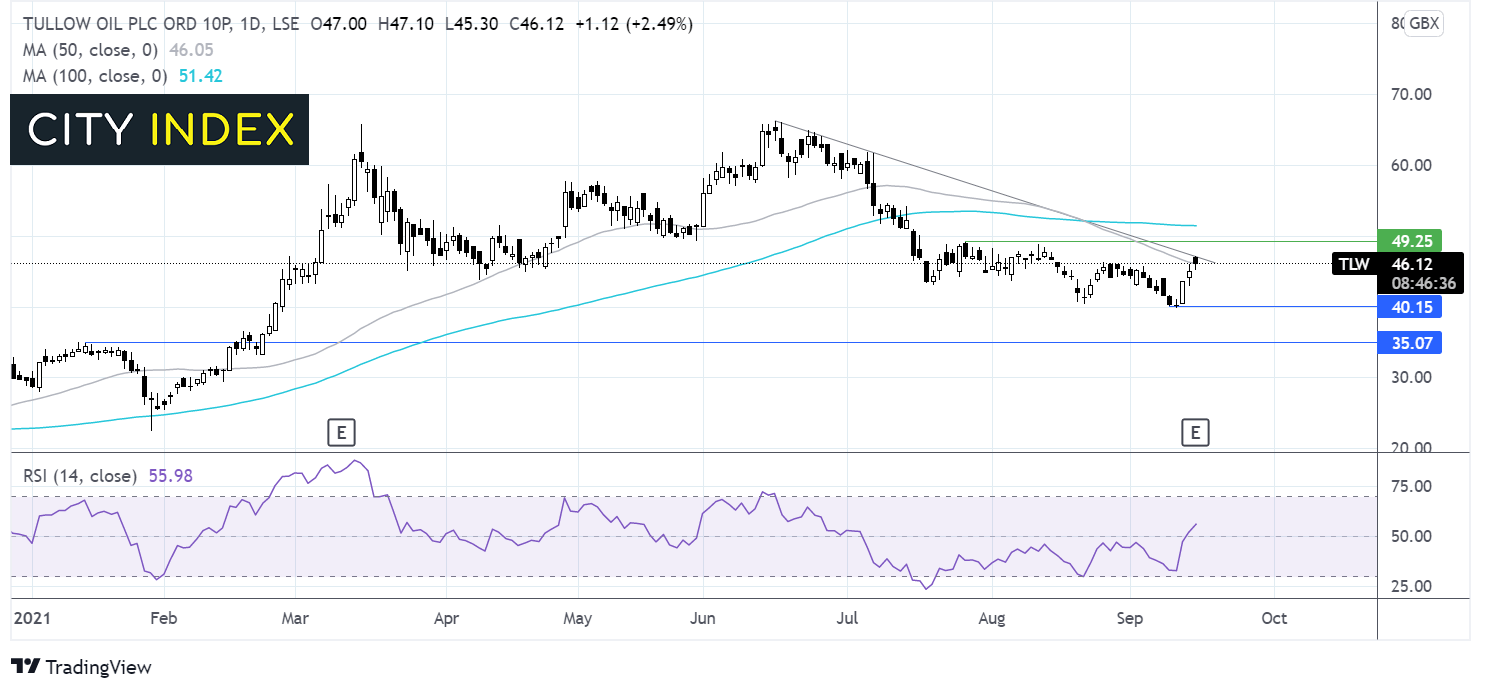

Where next for the Tullow Oil share price?

After trending higher across the year Tullow Oil ran into resistance at 66p. After hitting this year to date high, the price formed a series of lower highs and lower lows finding a floor last week at 40p.

The price has rebounded off this level and traded higher over the past three session. The RSI is supportive of further upside. Any move higher is guarded by the descending trendline resistance at 47p. A move over 49p horizontal resistance could bring the 100 sma at51.4p into play.

Failure to break above the falling trendline resistance could see last week’s low at 40p come into focus. A fall below here could spark a deep selloff to 35p the January high.

Redrow expects sales rate to normalise going forward

Redrow said the buoyant housing market has moderated in recent months and that it expects sales rates to return to more normalised levels after experiencing a spike in demand during the pandemic and the stamp duty holiday.

Revenue rose 45% in the year to June 27 to £1.94 billion from the £1.34 billion booked the year before. That was the result of Redrow building 5,620 homes in the period compared to only 4,032 last year.

Pretax profit more than doubled year-on-year to £314 million from £140 million, coming in ahead of the £301.6 million expected by analysts.

The improvement from last year, when it was disrupted by the pandemic, will be welcome, but results remain below pre-pandemic levels from the £2.11 billion in revenue and £406 million in profit delivered in the 2019 financial year. That comes as Redrow scales back its operations in London to focus on better opportunities outside the capital.

Still, the recovery prompted Redrow to pay a final dividend of 18.5p, having not made a payout last year due to the uncertainty plaguing its outlook. That takes the total payout for the year to 24.5p.

Redrow entered the new financial year with an order book worth £1.43 billion. That is up by a fraction compared to a year ago but well ahead of the £1.01 billion booked two years ago before the pandemic started.

Redrow also said that the rising input costs are continuing to be offset by rising house prices. Average selling prices increased 2% in the year to £338,500.

The company also reinstated its medium-term guidance now it has ‘returned to a more normal market’. Redrow is targeting annual revenue of over £2.2 billion and EPS of over 90p by the 2024 financial year, with an operating margin of 19.5% and a return on capital employed of over 22%. For context, Redrow delivered an operating margin of 21.4% and a ROCE of 18.5% in the recently-ended financial year.

‘The buoyant housing market has moderated in recent months and we anticipate sales rates will return to historically average rates over the course of the current financial year. It is on this basis we have planned for the future and we are confident our timely investment in land, combined with strong demand for our Heritage homes, will support our longer-term growth aspirations,’ said chairman John Tutte.

‘Additionally, our record order book also provides us with an excellent platform for the future with over £1.3 billion of revenue already secured for the current financial year. As a result, the business is well-placed to deliver another set of strong results,’ he added.

Redrow shares were down 1.1% in early trade this morning at 694.1p.

Keywords Studios warns growth will slow after stellar performance

Keywords Studios posted strong double-digit growth in both revenue and earnings during the first half thanks to a buoyant video games market, but warned growth will moderate as it comes up against tougher comparatives in the second.

The company, which supplies technical and creative support to the video game industry, said revenue grew over 37% in the first half of 2021 to EUR238.7 million, coming in just ahead of what analysts had expected. Organic revenue growth accelerated to 22.9% from just 8% last year.

Adjusted Ebitda jumped over 64% to EUR50.7 million, boosted by an improved margin of 21.2% compared to 17.8%.

Adjusted pretax profit improved 83% to EUR39.7 million while reported pretax profit increased over 97% to EUR21.9 million from EUR11.1 million last year.

The company said growth was driven by robust demand from the video game industry, which it said was eagerly churning out new content after suffering production delays and disruption in 2020. It said it is still suffering from some operational disruption but said it ‘continues to operate flexibly across all service lines to deliver market-leading service to clients’.

Keywords said it will pay an interim dividend of 0.7p. It did not make an interim payout last year as the pandemic caused uncertainty, but the payout is above the 0.58p dividend paid out in the first half of 2019.

Looking forward, Keywords said trading has ‘started well’ in the second half, noting strong demand for game development, marketing and art creation services.

‘Our Game Development, Marketing and Art Creation service lines, which work at the earlier stages and throughout the content creation cycle, are particularly expected to benefit from this increased activity throughout H2. Whilst we anticipate that demand for our later stage services, Testing and Localization, will build as content flows into them as we move through the second half and beyond,’ the company said.

Keywords said it remains on track to deliver its upgraded guidance over the full year, but warned that growth will moderate as it comes up against tougher comparatives in the second half.

Keywords is aiming to deliver annual adjusted pretax profit margin above its 14% to 15% historical range but said this will start to normalise in 2022 as investment rises. The current consensus estimates Keywords will deliver annual revenue of EUR498 million and adjusted pretax profit of EUR79 million. That would compare to the EUR373.5 million in revenue and profit of EUR55 million delivered in the last financial year.

‘We have continued our acquisition strategy which is building the group into the 'go to' service provider globally, with the recent acquisitions of Tantalus Media, Climax Studios and AMC taking us into new geographies and deepening our Game Development and Art Creation capabilities,’ said John Hauck, CFO and joint interim CEO.

‘Looking forward, we expect the strong demand to continue, giving us confidence in delivering a full year performance in line with recently increased market expectations, and our financial strength leaves us well placed to continue to complement organic growth with value-accretive acquisitions,’ he added.

Keywords said it is still searching for a new CEO after Andrew Day retired in June, with Hauck holding the ship steady alongside chief operating officer Sonia Sedler in the meantime.

Keywords shares were down 1.1% in early trade this morning at 3176.0p.

Restaurant Group grows confident since reopening sites

Restaurant Group said it has delivered strong growth and outperformed the wider market since it was able to start welcoming customers back indoors in May, prompting it to raise its earnings guidance for the rest of the year.

Restaurant Group shares were down 4.5% in early trade this morning at 117.3p.

The company, known for its sprawling portfolio of restaurants and bars like Wagamama and Coast to Coast, was one of the worst hit by the pandemic. Although it was able to keep hundreds of sites open for takeaway and delivery, the majority of its portfolio was only able to properly reopen when restrictions on indoor dining were eased on May 17.

Between indoor dining resuming on May 17 and August 29, Wagamama delivered like-for-like sales growth of 21% while the wider market experienced growth of just 8%. Its pubs delivered 12% growth while the wider market continued to struggle and posted a 2% decline, while its leisure sites reported an 18% jump in LfL sales, outpacing the 8% growth seen by its rivals.

Its concessions business continues to struggle with LfL sales down 53% in the period, but that also outperformed the steeper falls experienced by competitors.

‘We have made good progress in the past six months, securing the refinancing and recapitalisation of the group in the first quarter before focusing our attention on the re-opening of the business and welcoming back dine-in customers as government restrictions eased,’ said chief executive Andy Hornby.

‘Whilst there are some well documented sector challenges to navigate in the short-term, particularly around labour availability and supply chain, we believe the group is well positioned for the long- term,’ he added.

Although the performance has improved since indoor dining resumed, its financial results suffered as most of its sites were closed or operating at reduced capacity for most of the first half. As a result, revenue in the 27 weeks to July 4 came in at £216.8 million compared to £227.2 million the year before when the scenario from the pandemic was equally challenging.

Adjusted Ebitda rose to £11.3 million from a loss of £18.3 million the year before, while its reported pretax loss at the bottom-line narrowed to £58.8 million from the vast £234.7 million the year before.

Looking forward, Restaurant Group said it is expecting to continue outperforming the wider market in terms of LfL sales for the rest of the year, and said the trading performance since reopening ‘supports an increase in our FY21 Ebitda expectations’ – although it did not provide firm numbers to back that up.

Trustpilot Group ups growth ambitions as bookings accelerate

Trustpilot Group, the digital review platform, said it has seen a re-acceleration in bookings growth during the first half of 2021, prompting it to raise its growth target for the rest of the year.

Revenue was up 31% in the six months to the end of June to $62 million, rising 22% at constant currency. Annual recurring revenue followed 36% higher to $134 million.

Trustpilot, as a subscription software business, focuses on retaining customers and said its retention rate rose to 97% in the period compared to 91% the year before. The site had hosted over 144 million reviews on its platform at the end of June, up from 100 million a year ago. Similarly, the number of domains reviewed on its site has climbed to 626,000 from just 445,000.

Its adjusted loss for the period widened to $3.7 million from $2.1 million the year before, while its reported loss at the bottom-line ballooned to $17.2 million from $5.8 million.

The company reported a 37% rise in the number of bookings, which provides visibility to future revenue. Trustpilot said it is expecting annual revenue growth this year to match the 22% constant currency growth seen in the first half, up from its previous target to deliver growth in the high-teens.

‘We saw strong growth across all geographic regions in the period, as we continued to demonstrate our ability to scale our business efficiently,’ said Trustpilot.

‘The growth we have achieved also reflects an element of recovery from the impact of the Covid-19 pandemic which affected H1 FY20. The subsequent re-acceleration in our business that we saw in H2 FY20 has continued, as anticipated, into the first half of this financial year,’ it added.

Trustpilot shares were down 5.4% in early trade this morning at 389.6p.

How to trade top UK stocks

You can trade a wide variety of UK stocks with City Index in just four easy steps:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Equities articles

June 8, 2024 02:00 AM

June 3, 2024 05:56 AM

June 3, 2024 03:34 AM