Top UK Stocks and Shares | BP Shares | Standard Chartered Shares | Greggs Shares | Domino's Shares | Travis Perkins Shares

Top News: BP beats expectations and vows to increase investor returns

BP said it has increased its dividend and launching a new share buyback after beating expectations in the second quarter, as it vowed to keep growing shareholder distributions going forward.

Revenue rose to $37.6 billion in the second quarter from just $20.77 billion the year before thanks to the improvement in prices as the global economy reopens.

The underlying replacement cost profit – BP’s headline figure – came in at $2.79 billion compared to the $6.68 billion loss booked the year before when the pandemic hit. That came in well ahead of the $2.05 billion expected by analysts. The reported replacement cost profit of $2.38 billion turned from an almighty $17.65 billion loss last year.

The strong performance prompted BP to raise its quarterly dividend by 4% to 5.46 cents from 5.25 cents previously, and that will be complimented by a new $1.4 billion share buyback following the $500 million buyback launched earlier this year.

‘On average at around

Brent currently trades at over $70 a barrel and has remained well above that $60 threshold since early February.

BP made around $700 million in surplus cashflow during the second quarter, which was welcome news considering it warned it could post a deficit in the period. Combined with the prior quarter, BP generated $2.4 billion in surplus cash in the first six months of 2021. BP is returning 60% of surplus cash to investors via dividends and buybacks.

The new buyback will begin before it announces its third quarter results, when it will also reveal its buyback plans for the fourth quarter.

Shareholder distributions were introduced earlier this year after BP hit its $35 billion net debt target around a year early. BP has continued to cut its debt pile and ended June with $32.7 billion in net debt, down from $33.3 billion three months earlier.

BP remains confident going forward, believing that demand for oil can return to pre-pandemic levels before the end of 2022.

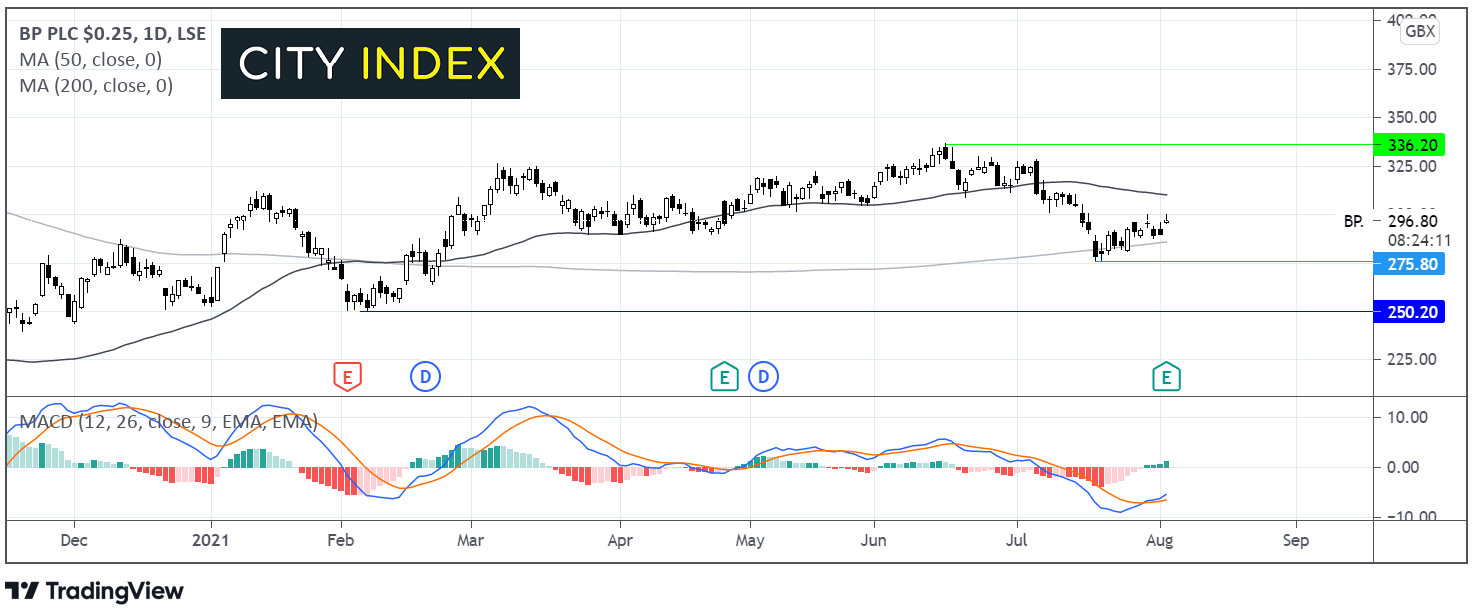

Where next for the BP share price?

The BP share price has trade relatively range bound across the year to date capped on the lower side by 275p and on the upper side by 325p. More recently the share price has been trading at the lower end of the range.

The share price has picked up off 275p retaking the 200 day moving average. The bullish crossover on the MACD is keeping buyers hopeful of more upside.

The recovery in the BP share price needs to over resistance at 309p the 50 dma in order to attack 336p the year to date high.

On the flipside, sellers will be looking for a break below 285p the 200 dma in order to test 275p the monthly low. This could open the door to a steeper selloff to 250p the yearly low.

Standard Chartered reinstates dividend and boosts buyback

Standard Chartered said it is resuming dividend payments and launching an additional share buyback programme after delivering strong growth in the first half of 2021, driven by the improving economic outlook as the world recovers from the pandemic.

The bank reported a 37% jump in underlying pretax profit in the first half to $2.68 billion from $1.95 billion the year before. That was supported by a $47 million release of reserves that had been set aside for potentially bad loans spawning from the pandemic, whereas results were weighed down by a hefty $1.56 billion charge last year. On a reported basis, pretax profit jumped 57% to $2.55 billion from $1.62 billion.

‘I am encouraged by our positive performance in the first half of 2021 despite an uneven recovery from Covid-19. We grew profit before tax 37% year on year, helped by improved loan impairments, strong underlying business momentum and good progress across our strategic priorities. We are more confident in achieving our return on tangible equity targets and we are pleased to announce today an additional share buy-back programme together with the resumption of our interim dividend payment,’ said chief executive Bill Winters.

Standard Chartered said it is resuming payouts with an interim dividend worth 3.0 cents per share, or $94 million in total. The share buyback will return another $250 million to investors and will be launched ‘imminently’. That decision has been made after ending June with a CET1 ratio – which measures the financial strength of a bank – of 14.1%, above the 13% to 14% target range.

‘We intend to operate dynamically within the full CET1 13-14% target range with an eye to the opportunities for growth, as well as credit and economic conditions and the strength of our earnings, as we continue our focus on safely improving our overall return on capital,’ said the bank.

Standard Chartered shares were trading 2% higher in early trade this morning at 445.2p.

Standard Chartered said a record performance for its Wealth Management division, with income up 26% year-on-year, and the strongest performance from its Transaction Banking Trade unit since 2018, with income up 16%, were both offset by the lower interest rate environment and a ‘return to more neutral market sentiment’.

Greggs ups expectations and restores dividend as sales recover

Greggs has reintroduced its dividend after delivering a strong recovery in the first half of 2021, with like-for-like sales having surpassed pre-pandemic levels since non-essential retailers were allowed to reopen back in mid-April, giving it the confidence to raise expectations for the full year.

Greggs shares were up 2% in early trade this morning at 2853.0p, marking a fresh all-time high for the stock.

The baker said total sales in the first six months of the year rose to £546.2 million from just £300.6 million the year before, when it started to be severely disrupted by the introduction of lockdown. More importantly, that was in-line with the £546.3 million revenue booked in the first half of 2019 before the coronavirus crisis erupted.

Greggs reported an underlying pretax profit of £55.5 million compared to the £64.5 million loss reported last year, and that too was ahead of the $40.7 million delivered two years earlier before the pandemic hit.

Like-for-like sales in the first half were down 9.2% compared to pre-pandemic levels but have returned to growth since non-essential retailer reopened on April 12, with Greggs able to benefit from increased footfall around town centres and other sites. It said like-for-likes in the four weeks to the end of July were 0.4% higher than two years before.

It also opened 48 new stores in the first half and closed 11, expanding its store network to 2,115. It expects to open 100 new shops on a net basis in 2021. It has also expanded the number of outlets offering delivery services, which account for around 8.5% of total sales at present.

‘Greggs once again showed its resilience in a challenging first half, emerging from the lockdown months in a strong position and rebuilding sales as social restrictions were progressively relaxed,’ said chief executive Roger Whiteside.

‘We continue to make good progress with our strategic priorities, growing the shop estate and investing in our digital capabilities to compete in all channels and dayparts of our market,’ he added. ‘Whilst there continue to be general uncertainties in the market, given our recent performance we now expect full year profit to be slightly ahead of our previous expectation.’

The improving picture has prompted Greggs to reintroduce its dividend with an interim payout of 15.0 pence per share, marking the first dividend to be paid since October 2019 when they were suspended amid the pandemic. Greggs said it is targeting an annual dividend that can be twice covered by underlying earnings, and has hinted further cash could be returned to shareholders going forward.

‘The board acknowledges that the business will be carrying a higher-than-normal cash balance in the short term but believes this is a prudent position to adopt given the backdrop, and intends to return any surplus cash to shareholders in due course, in line with its longstanding policy,’ Greggs clarified.

Domino’s Pizza Group boosts buybacks as sales soar

Domino’s Pizza Group said it is boosting the amount to be returned through share buybacks as its pizzas remain as popular as ever, and said it remains confident even as it starts to come up against tougher comparatives and people start to eat out more as lockdown eases.

The company said it was boosting the size of its current buyback programme to £75 million from £45 million previously and paying an interim dividend for the first half of 3.0 pence. No interim payout was made last year as it hoarded cash when the pandemic hit but it does represent one-third of the 9.1p final payout made in 2020.

Domino’s Pizza shares were up 5.4% in early trade this morning at 442.0p, marking a new lal-time high for the stock.

The boost announced today means Domino’s has announced it is returning £136 million of surplus capital to shareholders since the start of 2021.

That came as Domino’s reported 19.6% year-on-year growth in systemwide sales during the first half to June 28 to £752.3 million, with like-for-like growth accelerating to 19.3% from 4.8% the year before.

That translated to higher earnings. Underlying pretax profit jumped 27.7% to £60.8 million while reported profit after tax more than doubled to £41.3 million from just £19.0 million the year before. EPS followed higher to 8.9p from 4.4p.

Domino’s said its new TV marketing campaign and the boost provided from the Euros 2020 football tournament helped boost sales. It also flagged that digital sales have continued to build momentum and now account for 93% of all UK system sales.

Domino’s said it is still working toward a goal of delivering systemwide sales of between £1.6 billion to £1.9 billion per year over the medium-term.

‘As the second half develops, we will operate within a shifting and uncertain landscape as the nation is released from the restrictions imposed by the Covid-19 pandemic, and the country returns to a level of normality. We believe this will benefit our Collection business, which we expect to gradually recover toward order count levels more in line with 2019. Our delivery business will face more competition as the hospitality trade reopens but we believe the strength of our brand and our continued investment in developing our offer will enable the delivery business to maintain its performance,’ said Domino’s.

Travis Perkins shareholders set for windfall as it raises guidance

Travis Perkins reinstated its dividend and raised its profit guidance this morning after like-for-like revenue returned to pre-pandemic levels in the first half of the year, and said it will return more cash to investors once it has completed the sale of its plumbing and heating business.

The building supplies merchant said it has reintroduced the dividend with a 12.0 pence interim payout and said a special return will be made once the £325 million sale of its plumbing and heating business to HIG Capital is completed. An investor update will be held on September 29 to provide more information on how it will ‘deliver long term sustainable value to shareholders’.

That asset sale follows on from Travis Perkins spinning-out Wickes and listing the unit in London earlier this year.

The news came as Travis Perkins said it now expects to report an annual adjusted operating profit of ‘at least’ £310 million, up from £280 million beforehand. The £30 million boost is coming from higher profits than originally expected from its property restructuring programme. That would be up from the £227 million profit delivered in 2020 but still below the £442 million delivered in 2019 before the pandemic hit.

Travis Perkins shares were trading 2.6% lower in early trade this morning at 1680.0p.

Revenue in the first half rose over 37% year-on-year to £2.29 billion and like-for-like growth was strong at 44.1%. Adjusted operating profit of £164 million improved from just £17 million the year before, with adjusted EPS following to 46.2p from 1.0p.

On a reported basis, Travis Perkins swung to an operating profit of £168 million from a £79 million loss, with EPS of 41.5p turning from a 34.5p loss the year before.

‘The long term fundamentals of the group's end markets remain robust with ongoing demand for new housing and historic underinvestment in the repair, maintenance and improvement (RMI) of the existing UK housing stock needing to be addressed. This is further underpinned by the UK Government's commitment to decarbonise the UK economy, providing stimulus packages across a number of sectors, and to invest in infrastructure,’ said Travis Perkins.

‘Whilst some uncertainty remains due to the ongoing pandemic, coupled with inflationary pressures and product availability issues, the group expects the RMI market to remain strong for some time to come and for new housing to continue on its recovery path,’ the company added.

How to trade top UK stocks

You can trade a wide variety of UK stocks with City Index in just four easy steps:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Equities articles

June 8, 2024 02:00 AM

June 3, 2024 05:56 AM

June 3, 2024 03:34 AM