PCE inflation, NFP and ISM manufacturing in focus: The Week Ahead – 25/08/2023

It's the last trading week of August, and it's fair to say that market conditions were more volatile and eventful than this time of year tends to provide. At the time of writing, we're yet to hear what Fed Chair Jerome Powell has to say, but it could certainly set the tone for next week's trade. And there is no shortage of data to kick off September, including US PCE inflation, GDP, and the ISM manufacturing survey. Final PMIs are also published for the US, UK, Europe, Japan, and Australia. And incoming RBA Governor Bullock speaks, and a host of Australian data includes CPI, retail sales, home loans, and capex.

The week that was:

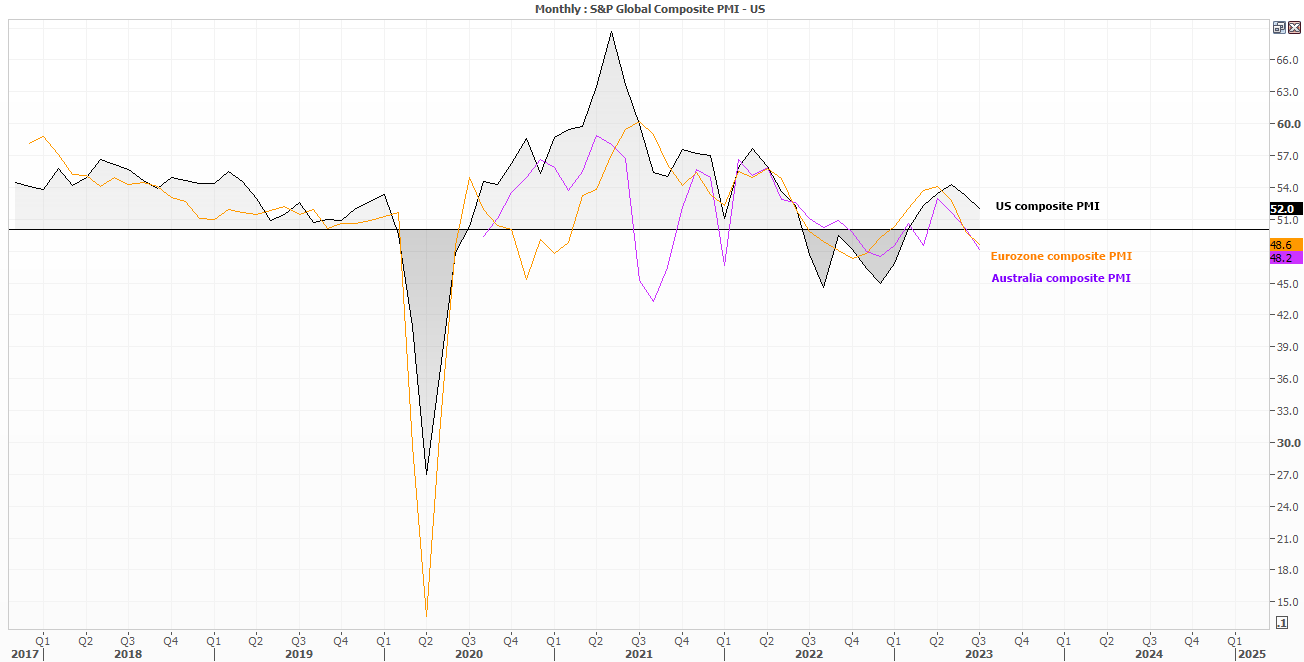

- Flash PMIs mostly disappointed to the downside for both manufacturing and survey reports, dragging composites lower for US, Europe, UK and Australia

- Whilst the weaker PMIs played into the hands of those calling for a peak RBA rate at 4.1%, it also saw bets for another 25bp hike or 50bp BOE hike scaled back

- It also weakened the US dollar and yields ahead of the Jerome Powell’s Jackson Hole speech, as it took the sting out of anticipations of his ‘higher for longer’ narrative

-

Nvidia delivered a blowout earnings report to send shares 10% higher to a new ATH during after hours trade (although those gains were promptly returned during risk-off trade on Thursday)

-

Rising yields and a higher dollar weighed on Wall Street on Thursday, sending the Nasdaq over -2% lower and forming a bearish engulfing day to erase the week’s gains

The week ahead (calendar):

Please note that it is a public holiday in the UK on Monday 28th August 2023

This content will only appear on City Index websites!

Earnings This Week

Look at the corporate calendar and find out what stocks will be reporting results in Earnings This Week.

The week ahead (key events and themes):

- US PCE inflation

- Nonfarm payroll

- ISM manufacturing PMI

- Final PMIs

- US GDP

- Australian data (CPI, retail sales, home loans capex and bullock speech)

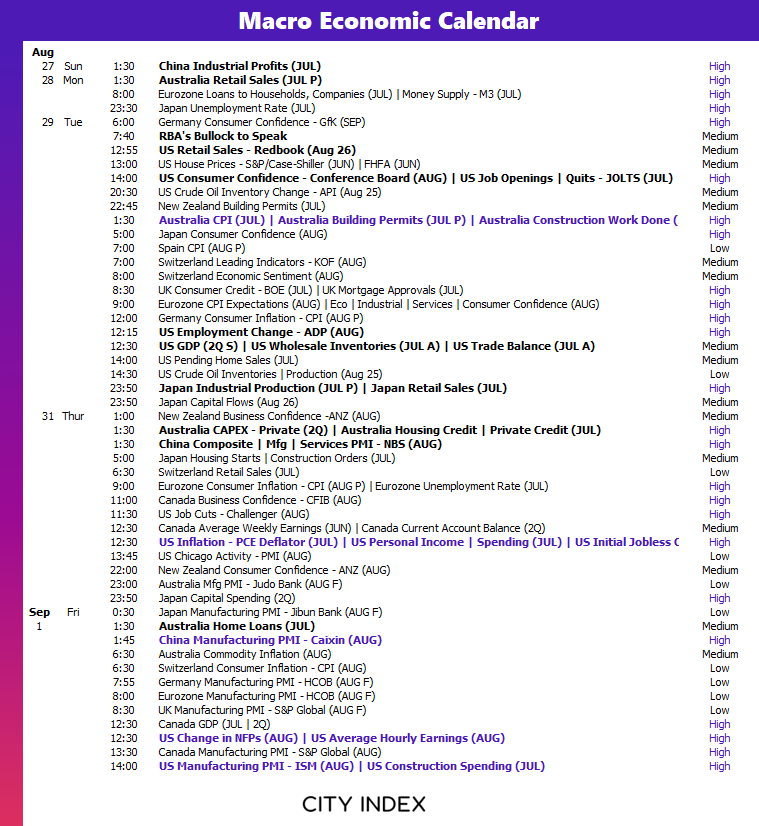

US PCE inflation

Inflation data continues to be the key metric that drives expectations for monetary policies, and therefore drives sentiment for global markets. US inflation data is at the top of the pile of significance, and PCE data is ‘top of the top’ given it is generally the Federal Reserve’s preferred measure.

The significance of this particular PCE inflation report may hinge upon how hawkish Jerome Powell is at his Jackson Hole speech. But in a nutshell, the quicker inflation decelerates, the less hawkish the Fed needs to be and the US dollar could falter.

Last month we saw the annual rate of core PCE fall to a 21-month low of 4.1%, which was its fastest decline since the pandemic. But it remains debatable as to whether we’d see another drop of a similar magnitude next week (as nice as that would be). Looking through the data, services PCE has risen 0.3% m/m three in the last four months. Therefore, a print of 0.2% or lower would be a welcome development.

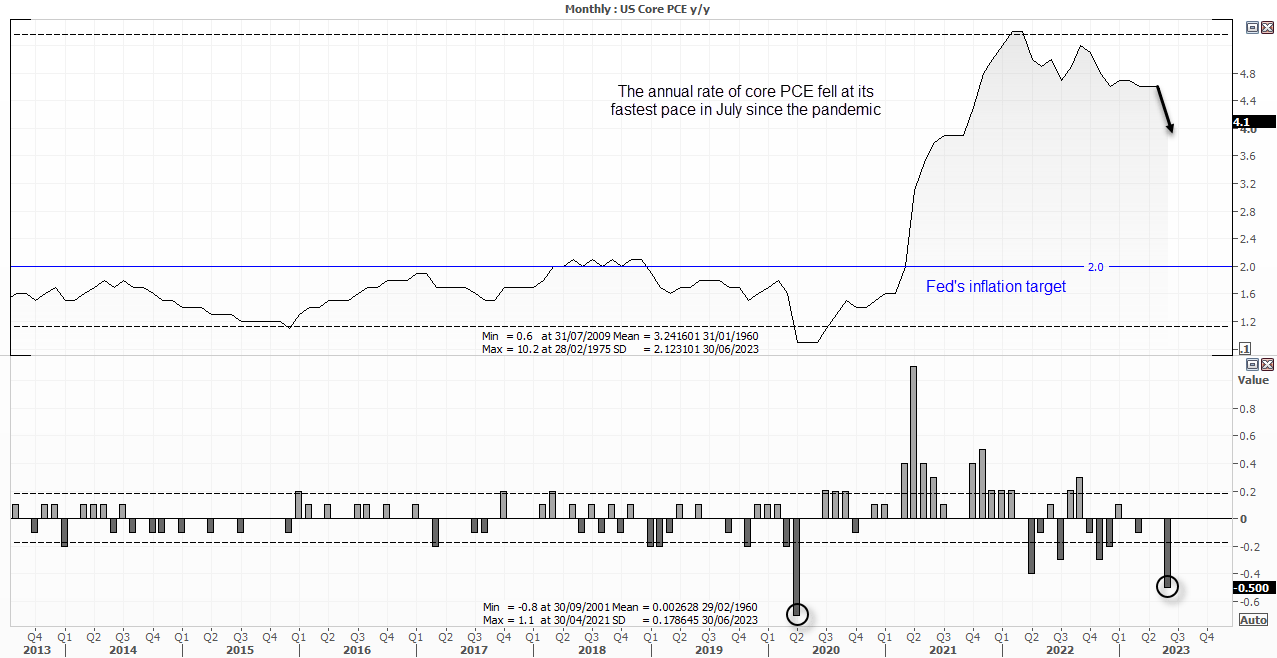

US employment data (Nonfarm payroll, ADP payrolls, jobless claims)

PMIs aside, we’re just not seeing enough weakness in headline employment data to get too excited about the Fed cutting rates any time soon. Whilst there has been plenty of speculation of weakness using other employment metrics, they do not carry as much weight as they perhaps should as the Fed seem to make decisions on lagging indicators such as the unemployment rate. And an unemployment rate of 3.5% hardly screams recession to the Fed, which is a key reason why rate cuts any time soon remain unrealistic.

Still, the monthly nonfarm payroll report is released on Friday and still warrants attention. But we also have other employment metrics which can help shape the tone, because if they come in stronger than expected traders may try to front-run a hotter NFP report (and visa versa). Job openings is released on Tuesday, ADP payroll on Wednesday and jobless claims are on Thursday.

Market to watch: USD/JPY, EUR/USD, S&P 500, Nasdaq 100, Dow Jones, WTI crude oil, gold

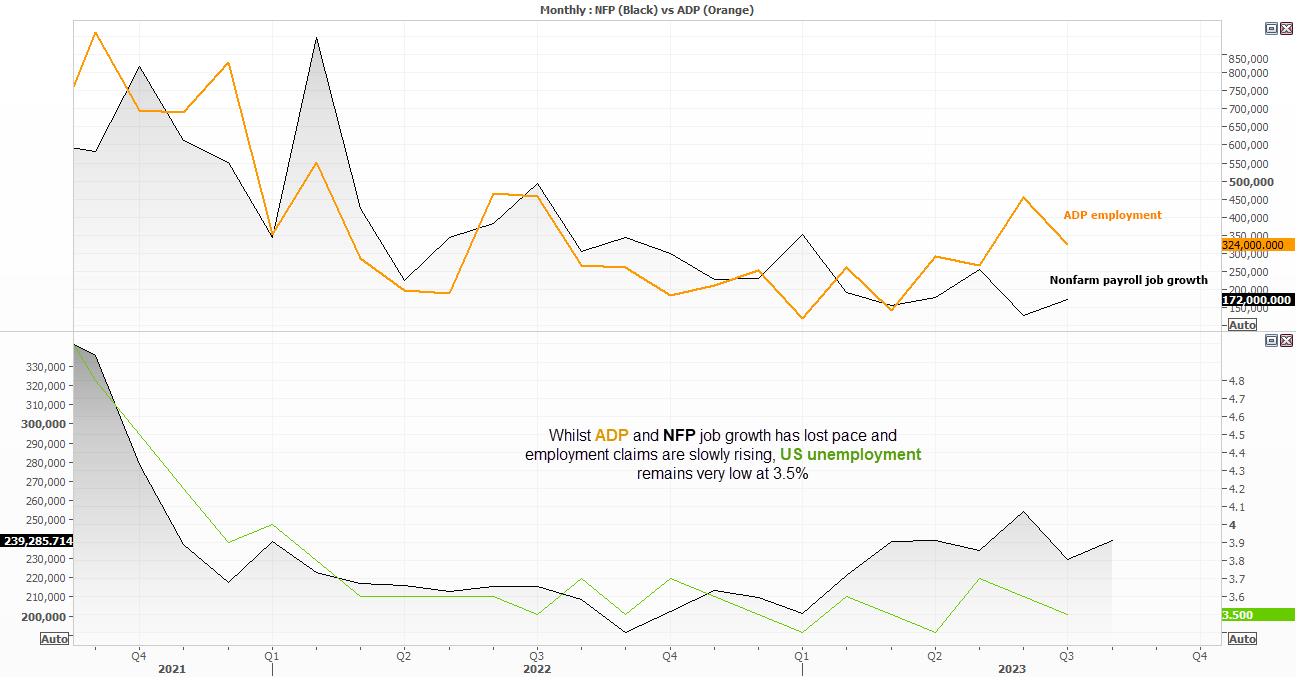

ISM manufacturing PMI

The US manufacturing sector topped out in early 2021 according to the ISM (Institute for Supply Management) and been contracting for nine months. Another weak print may not change much, unless it falls at a much faster pace and backs up the weak data seen on the S&P Global PMI survey. However, new orders are contracting at a much slower pace, so if there is any hope to be gleaned it would be to see new orders move closer to 50 (or above it to denote expansion for the future).

Market to watch: EUR/USD, GBP/USD, USD/JPY, S&P 500, Nasdaq 100, Down Jones, WTI crude oil, gold

Final PMIs

Given that flash PMIs generally include around 80-90% of all survey respondents, final PMIs are easily forgotten as they tend not to deviate too far from the flash estimates. Yet with the general theme of deterioration for manufacturing and services PMIs for the UK, Europe and US this week, traders may take a bit more notice of these final report. Perhaps the original reports were too gloomy, and that leaves some hopes that they may be revised slightly higher. Otherwise, that just leaves the scenario where final PMIs confirm just how bad the flash reports were, or even worse they decline at a faster rate.

Market to watch: EUR/USD, GBP/USD, EUR/GBP, USD/JPY, S&P 500, Nasdaq 100, WTI crude oil

US GDP (2nd revision)

Whilst it seems unlikely to be a major event, GDP should at least be mentioned as the preliminary release far exceeded expectations. On one hand it alleviated concerns of a hard landing, on the other it pushed out expectations of Fed cuts further into 2024. SO we at least get to find out whether GDP really did rise 2.4% in Q2, or if it needs to be downgraded and fan more fears of a hard(er) landing for the US economy.

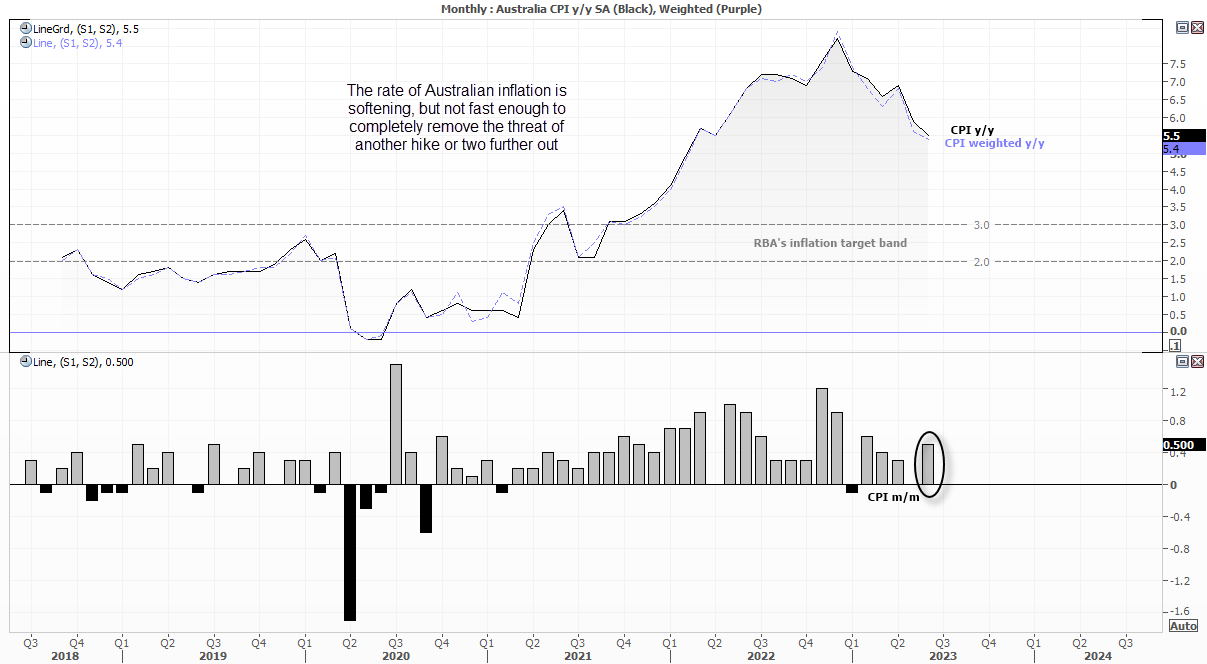

Australian data (CPI, retail sales, home loans capex and bullock speech)

As things stand, many suspect that the RBA have indeed reached their peak rate at 4.1% - although that doesn’t mean the threat of further hikes does not remain. Yet with household spending down around -10% y/y by some measure, cracks forming in Australia’s headline employment figures and China’s data going from bad to worse, the threat of an imminent hike is dead in the water.

However, there is enough data next week to potentially change things if they are one sided enough. The monthly inflation report on Wednesday is the key event, and with a weighted CPI of 5.4% it clearly remains “too high”. With housing up 7.4% y/y and food up 7% y/y, we’re not expecting miracles. But it needs to pull back at a faster pace to truly remove the threat of another hike. But we also have retail sales on Monday, and if household spending is a guide then we may see it contract at a faster pace than last month’s -0.8% fall. It could also take some of the wind out of Wednesday’s CPI sails if it is soft enough.

Building approvals is unlikely to be knocking out strong figures on Thursday, but there is a case that is it around a cycle low looking at a 15-year chart. Capex data also provides a lead on GDP and is released alongside building approvals.

Incoming governor Michelle Bullock speaks on Tuesday at 5:40 AEDT (07:40 GMT). Titled “Climate Change and Central Banks”, it may not be ground breaking in terms of policy. But her words will carry great importance when she takes over the helm in a few weeks from now.

Market to watch: AUD/USD, NZD/USD, AUD/NZD, NZD/JPY, AUD/JPY, ASX 200

-- Written by Matt Simpson

Follow Matt on Twitter @cLeverEdge

How to trade with City Index

You can trade with City Index by following these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the market you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Week ahead articles

Yesterday 04:48 AM

July 19, 2024 06:20 AM

July 12, 2024 01:32 AM

July 12, 2024 01:32 AM