Asian Indices:

- Australia's ASX 200 index fell by -49.3 points (-0.73%) to close at 6,745.90

- Japan's Nikkei 225 index has risen by 305.16 points (1.02%) and currently trades at 30,192.83

- Hong Kong's Hang Seng index has risen by 406.76 points (1.4%) and currently trades at 29,440.88

UK and Europe:

- UK's FTSE 100 futures are currently up 26 points (0.38%), the cash market is currently estimated to open at 6,788.67

- Euro STOXX 50 futures are currently up 18 points (0.47%), the cash market is currently estimated to open at 3,867.74

- Germany's DAX futures are currently up 102 points (0.7%), the cash market is currently estimated to open at 14,698.61

Wednesday US Close:

- The Dow Jones Industrial fell -127.51 points (-0.39%) to close at 32,825.95

- The S&P 500 index rose 11.41 points (0.29%) to close at 3,974.12

- The Nasdaq 100 index rose 50.1 points (0.38%) to close at 13,202.38

It was a solid finish for the Dow Jones which closed at 33k to a new record. The S&P500 posted a modest 0.3% gain and etched out a new high, the Russell 2000 pared Tuesday’s losses whilst the Nasdaq 100 closed at a 2-week high.

The bullish potential the FTSE 100 showed on Tuesday (with a close above 6800) was short-lived. Now back beneath that key level and forming a bearish ‘dark cloud cover’ pattern, it serves as a reminder this is not an index to expect two or three consecutive closes in the same direction. And therefore, not an index to outstay ones’ welcome (on the daily timeframe, at least) until a trend actually develops.

Index futures are mostly in the black across Asia, with Japan’s TOPIX index (+1.3%) and Singapore’s STI (+1.1%) leading the way higher, although Australia’s SPI 200 futures are slightly lower by -16 points (-0.24%) following Australia’s stellar jobs report.

Huge employment boost for Australia

The Australian economy added 88.7k jobs in February, nearly triple the 29.1k forecast. But, more to the point, 89.1k full-time jobs were added and the unemployment rate fell from 6.4% to 5.8%. That is no small feat, even if the government JobKeeper aid is to finish at the end of March.

These numbers flying the face of RBA’s expectations of a slow recovery. But then I guess we’ll have to see if momentum is even slightly sustained before expecting the ‘really, really reserved’ central bank of Australia to get ahead of any perceived curve.

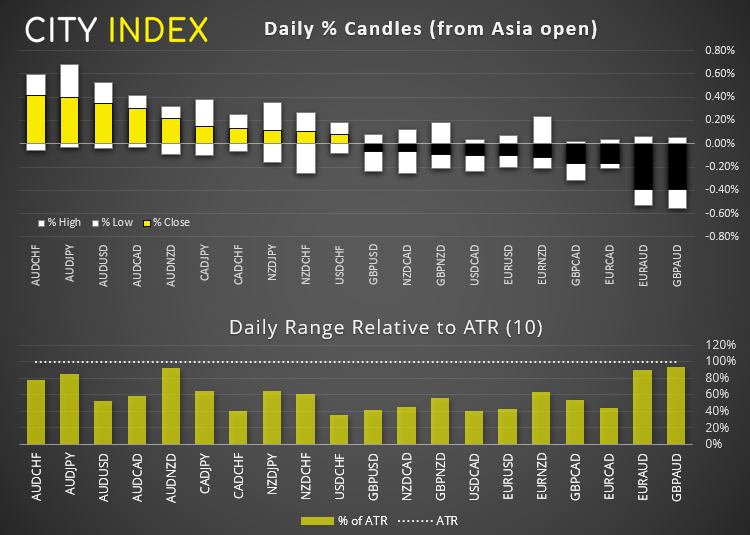

- AUD/JPY broke above 85.00 outlined in today’s Asian Open report, hence the bias remains bullish in line with the daily trend.

- AUD/USD is probing 0.7837 resistance, a break above of which clears the skies for a run towards 80c.

Elsewhere in the land of forex:

Clearly, AUD is the strongest (and most volatile) major overnight. Minor ranges elsewhere, but EUR is the weakest major.

- USD/CHF: Prices have finally drifted near our original counter-trend target, just above 0.9207 support. Yesterday’s bearish outside day suggests it could move lower still but we’d prefer to see how it reacts around current levels before committing.

- EUR/GBP: The 0.8538 support level remains unbroken, and yesterday’s wide ranging bullish outside candle is a concern for bears over the near-term. Still, whilst we could see prices drift higher the daily trend remains structurally bearish beneath the 0.8640 pinbar high.

- EUR/AUD: A bearish breakout occurred on Australia’s strong employment report. The bigger question for bears now is whether they can break beneath the February low and take the cross to its lowest level in three years.

- GBP/AUD tested trendline support on the daily chart, and interest to note that its overnight range is near its 10-day ATR. So, there’s some potential for bullish mean reversion from current levels if BOE is less dovish / slightly more hawkish than expected.

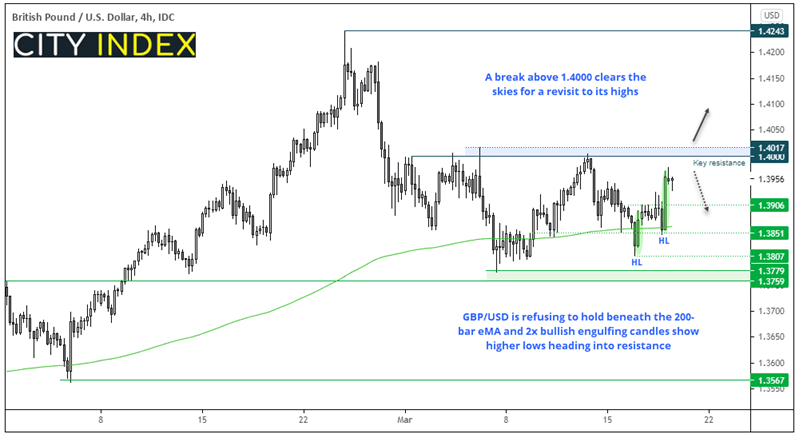

GBP/USD: Could a break of 1.4000 be on the cards? (Should BOE allow)

Yesterday’s bullish close formed the final candle of a 3-bar bullish reversal (the morning star reversal pattern). Given Tuesday’s bullish pinbar low forms a higher low and failed didn’t even test the 50-day eMA, we are hopeful that a significant swing low is in place.

We can see on the four-hour chart that prices are refusing to hold beneath the 200-dar eMA and two bullish engulfing candles show higher lows into resistance. The bias is for an eventual break above 1.4000 but we are also on guard for an initial sell-off beneath it.

- 1.4000 remains a pivotal level.

- A convincing break above 1.4000 suggests its bullish trend has resumed, but if traders are seeking to position themselves ahead of the breakout then they could consider bullish setups on lower timeframes, or evidence that support has been found above the 1.3906 pinbar high.

- But if 1.4000 holds as resistance, bears could seek to place stops well above it to fade into the highs of the range and target 1.3900 and 1.3850.

Commodities: Palladium is no ‘soft’ metal according to this rally

Palladium prices have extended their bullish surge, up around 15% over the past seven sessions and having clearly broken out of its multi-month sideways range. We suspect momentum has realigned with its long-term bullish trend and will seek bullish setups above 2,500.

Gold hit a high around 1756 overnight, just short of out 1760 bullish target. We cannot ignore resistance levels around the 1760/64, as we’re quickly approaching an area that may tempt bears to reload. Initially at least.

Brent futures tested $67 yesterday and formed a bullish hammer on the four-hour chart. Yet with prices drifting lower overnight, we could expect an attempt to break yesterday’s low. But, as long as prices hold above the 66.55 low then we could see prices range between 66.50 – 70.00 as the markets decide whether they want a much deeper correction, or trend continuation.

Up Next (Times in GMT)

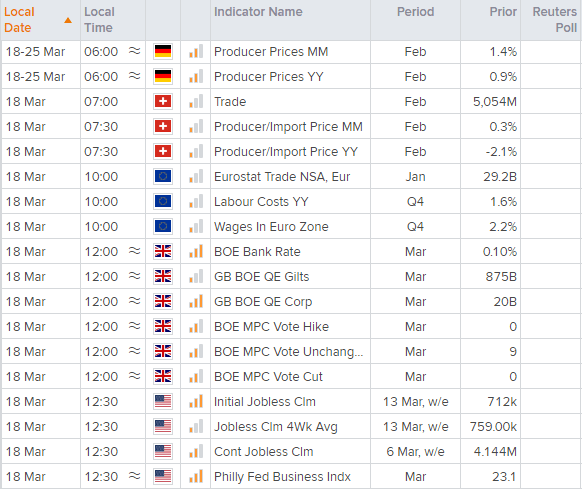

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

- German producer prices are up at 06:00. With yesterday’s stronger ZEW report citing rising inflation expectations, then it would be constructive to see it start in producer prices today, and potential further support an already stronger euro in a weaker dollar environment.

- At 08:00 ECB President Christine Lagarde is to debate the state of the Eurozone economy with lawmakers.

- The BOE (Bank of England) are expected to keep policy unchanged at today’s meeting. But with mixed comments and split views on what threats the economy faces then rising inflation rates and whether inflation remains ‘sticky’ will remain a concern.

- No major economic news is scheduled in the US session.

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Indices articles

July 25, 2024 01:30 PM

July 25, 2024 01:01 AM

July 25, 2024 12:41 AM

July 24, 2024 07:26 PM