What to expect from US retail stocks in Q3

We have seen Walmart and Target both issue multiple profit warnings this year as they try to adapt to the effects of persistent inflation, which has squeezed margins and caused dramatic changes in consumer shopping habits that has wreaked havoc on inventories and hurt their bottom line.

Rising inflation is helping bolster revenue through higher prices, but it is also pushing up expenses and the cost of everything continues to rise. We have seen headline inflation start to ease but core but it still remains high. We saw US CPI dropped to 7.7% year-on-year last month from 8.2% in September as it continues to ease following the peak seen in August, and we finally saw core inflation start to drop. Still, the situation is posing a problem for retailers that want to protect profitability but need to stick by their customers and provide them value.

Higher prices and the need to stretch pay packets further in response to the increase in the cost of living has prompted consumers to change the way they shop. They are having to spend more of their wages on essentials like food, wellness and health. Unsurprisingly, both Walmart and Target have seen a rise in demand for their private label products as people trade down from pricier brands.

Still, consumers ultimately have less to spend on discretionary goods and, as a result, we have seen demand for things like clothing, homeware, electronics and other forms of general merchandise collapse. Plus, consumers are deciding to spend whatever money they have left on experiences and services, like restaurants and outings as they make up for lost time during the pandemic, and less on goods after stocking up during lockdown.

The good news is that inflation is encouraging more shoppers through the doors. During normal times, retailers like Walmart and Target appeal to low-and-middle income consumers but in tough times like today everyone is looking for savings. Walmart has said about three-quarters of the market share gains it has made in food has come from customers that have annual incomes of over $100,000.

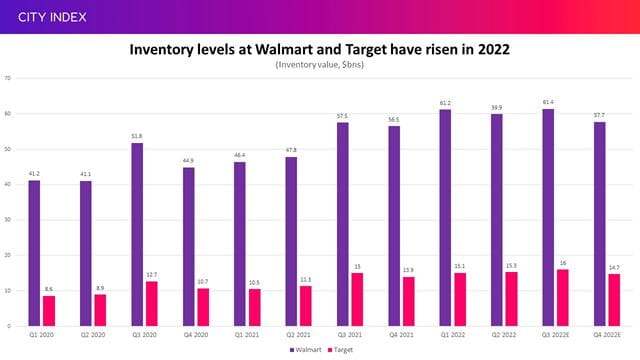

The bad news is that the rapid shift in demand has left retailers with not enough of the products customers want and too much of the stuff that they no longer need. Therefore, the industry has been forced to slash prices and offer deep discounts to shift inventory. This is what has driven the collapse in earnings and profit warnings from both Walmart and Target this year, in addition to the unwinding of demand that exploded during the pandemic.

Both companies have taken action to address their inventory issues. Investors may be spooked by forecasts that suggest inventory levels will have risen further in the third quarter – but the value is being pushed up by cost inflation and retailers are also stocking up early ahead of the holiday shopping season. Ultimately, inventories may be larger, but Walmart and Target have both signalled that it is of better quality and mix after being rebalanced to ensure they have the right products on the shelves.

With this in mind, investors will want to see evidence that retailers have the right mix. Back-to-school should provide a boost in the third quarter and will be treated as an early test for retailers, providing insight into how they are positioned ahead of the festive season. Consumers are keen to celebrate after two years of Covid-19 disruption but there is no doubt that value is the number one thing people are looking for and that consumers are more cost-conscious. The recent warning from ecommerce giant Amazon that sales will grow at their slowest rate on record for any festive season on record suggests general merchandise will remain out of favour, which will heighten attention on food and other essential categories.

The shift in demand and rising costs, which are expected to continue rising as we enter 2023, means earnings will remain under pressure. Still, Walmart and Target have signalled that the second half of 2022 will be better than the first and markets believe that margins will improve going forward and hope the worst is behind them.

Walmart Q3 earnings preview

Walmart will go first when it releases third quarter earnings on Tuesday November 15. Wall Street forecasts Walmart will report a 3.5% rise in US comparable sales, a 5.3% rise in revenue to $147.9 billion and a 9% year-on-year drop in adjusted EPS to $1.32.

Walmart should be past the worst of its inventory problems this quarter based on management’s commentary at the end of the last quarter. Chief financial officer John Rainey said around 40% of the rise in inventory levels during the period was purely down to cost inflation, and that only around $1.5 billion of it was causing a headache. This situation should have continued to improve, and management have promised a ‘strong finish’ to the back-to-school season that will ‘quickly transition to the holidays’.

Walmart has said it expects US comparable sales to be up 3.0% this quarter, and the fact analysts believe this will come in at 3.5% shows there is confidence Walmart is working through its inventory problems.

Earnings will remain under pressure as costs rise and shoppers buy more food and essentials, which offer lower margins, and a pullback in sales of more lucrative discretionary items. Still, markets are hopeful adjusted EPS at the bottom-line will decline at the milder end of its 9% to 11% target range.

Walmart has said the second half will be better than the first, so it not only needs to show an improvement in the third quarter but also provide a buoyant outlook for the festive period. This needs to at least meet guidance to install confidence over its prospects. Wall Street is expecting Walmart to deliver year-on-year US comparable sales growth of 3.2%, a 1.7% decline in operating income, and a 3.8% fall in adjusted EPS over the festive quarter.

The company’s guidance for the full year is for adjusted EPS to be down 9% to 11% from 2021 and analysts believe the decline will be on the milder side for now.

Where next for WMT stock?

Walmart shares have been on the rise since hitting a two-year low back in June. The rally gained momentum in the second half of October but has stalled after finding a ceiling at around $143, which has been unsuccessfully tested at least five times in the last eight sessions.

The RSI approached overbought territory at this level to suggest it is the first upside target that needs to be captured. A sustained break above here could allow the stock to climb toward the ceiling we saw over the five months to March at $146.50. The 42 brokers that cover Walmart have an average target price of $152.94, implying there is slightly greater upside potential. This is roughly aligned with the peaks we saw in both August and November 2021.

Any renewed pressure could see the stock swiftly fall back toward the rising trendline of support that has been in play since it hit those lows back in June. Investors will hope that the moving averages can provide some support sooner. If the trendline fails to hold, then the stock could slip to $128 before the two-year low comes back into play.

Target Q3 earnings preview

Target will follow with third quarter earnings out on Wednesday November 16. Wall Street forecasts Target will report comparable sales growth of 2.5% and expect revenue to rise 3.2% from last year to $26.1 billion. Adjusted EPS is estimated to drop 28% to $2.19.

Target, which is considerably smaller than its rival, saw earnings plummet almost 90% in the second quarter. That was much steeper than anticipated even though Target had lowered its guidance twice. That was the result of the company deciding to slash prices to shift excess inventory. Management said it was confident, however, that the short-term pain was vital to ensure the business was in a better position for the second half of the year.

Inventory levels remain high, but management has stressed that this is down to cost inflation and said it has a better mix, with more products that are bought frequently such as food and household essentials, as well as seasonal goods, in warehouses and less general merchandise after it cancelled big orders for stock that has seen demand disappear.

Target said in the last quarter that it had not seen as much inflation-induced change in shopping habits although it too has seen an increase in demand for food and beverages and other household essentials. Notably, beauty has also proven to be an area of strength for Target and that comes as it continues to rollout Ulta Beauty outlets in its stores.

It has promised a much better margin in the third quarter compared to the second, when it posted an operating margin of just 1.2%. Analysts are looking for a margin of 5.3% in the third and believe this can recover further to 6.2% in the fourth.

Target has not been providing quarterly guidance, but said it is aiming to deliver low-to-mid single digit revenue growth over the full year and an operating margin of 6% in the second half of the year. Wall Street currently has its doubts considering the consensus points toward annual topline growth of 3.3% and believe its margin in the back end of 2022 will come in just shy at around 5.8% as freight, fuel, shipping, and other fulfilment costs continue to apply pressure.

Where next for TGT stock?

Target shares also hit two-year lows back in June and, while it has since rebounded, it has not experienced as big a rally as Walmart. We saw the stock climb above $168 for brief periods in August and September but this has remerged as a ceiling after providing resistance late last month, following a series of lower-highs in recent months. Notably, this is aligned with the low we saw back in March 2021. A move above here would allow it to target the September peak at $175 and then the August peak of $180, which looks set to soon converge with the 200-day moving average.

The 34 brokers that cover Target have an average target price of $191.89, implying there is 25% potential upside from current levels.

Investors will hope that the brief level of support seen late last month at $147.50 can remerge if Target comes under pressure, although there are signs that this isn’t particularly strong. That leaves the door open to potential for a large decline back toward the two-year low at $139 should bad news send shares tumbling.

How to trade Walmart and Target stock

You can trade Walmart shares and Target stock with City Index in just four easy steps:

- Open a City Index account, or log-in if you’re already a customer.

- Search for ‘Walmart’ or ‘Target’ in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Or you can practice trading risk-free by signing up for our Demo Trading Account.

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Equities articles

June 8, 2024 02:00 AM

June 3, 2024 05:56 AM

June 3, 2024 03:34 AM