When will Netflix release Q4 earnings?

Netflix is scheduled to release fourth quarter earnings after the markets close on Thursday January 19. The company will release a video interview with management at 1500 PT on the same day.

Netflix Q4 earnings consensus

Wall Street forecasts that Netflix will report a 1.6% year-on-year rise in revenue in the fourth quarter to $7.83 billion, ahead of the guidance provided by the company for sales of $7.78 billion.

Operating income, its headline earnings measure, is expected to plunge 43% from last year to $362.4 million while diluted EPS is set to suffer a sharper fall of almost 70% to $0.41. Still, the market consensus is ahead of Netflix’s guidance for quarterly operating profit of $330 million and EPS of $0.36.

Netflix Q4 earnings preview

Netflix had one of its toughest years ever in 2022. Subscriber growth has been uneven and volatile in recent years. The spike in popularity seen during the pandemic as people searched for entertainment whilst stuck at home during lockdown unwound and led to growth stalling before declining for the first time in the streaming company’s history. This caused it to lose its crown to rival Disney, severely dented confidence and resulted in its share price more than halving in 2022.

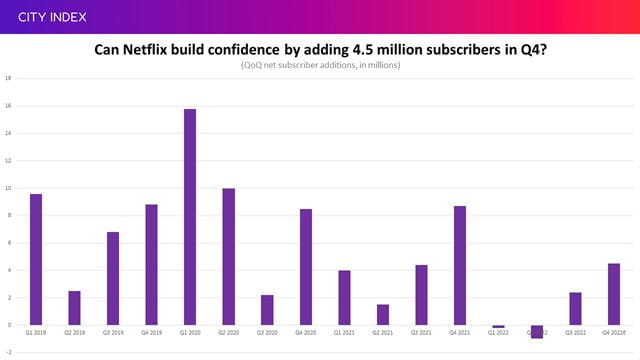

Netflix started to grow its subscriber base once again in the third quarter when it added 2.4 million users and it has said it expects this to accelerate to 4.5 million additions in the fourth, giving it the opportunity to show it is back on a steadier path of growth. Subscriber numbers will hit a record 230.25 million if it achieves that goal.

(Source: Bloomberg consensus)

The number of additions will prove highly influential on how markets react. An acceleration from the previous quarter would help install confidence that growth is reaccelerating while a slowdown would fuel fears that this is just a temporary rebound.

Some analysts have very different views on whether Netflix can achieve its goal to add 4.5 million subscribers this quarter. Bloomberg Intelligence analysts said a strong content slate driven by the likes of Wednesday and Glass Onion (the latter of which is one of its most watched releases upon release ever, according to CNET) could ‘help it easily meet or possibly exceed guidance’. Meanwhile, Barclays analyst Kannan Venkateshwar said he believes the company will fall far short of its goal and is ‘on a path’ to add just 2.7 million subscribers, citing a fall in app downloads and lower viewership figures as it comes up against tough comparatives from this time last year when it reaped rewards from the hugely popular Squid Game (which is its most successful TV series of all time).

It will be more difficult for investors to gauge which direction subscriber numbers are headed going forward. Netflix will no longer be providing guidance for paid net additions. Instead, the company is focusing on the financials such as revenue, operating margins and income, net income and earnings per share. It said the shift is a result of the introduction of new pricing tiers.

The slump in subscriber growth last year forced it to seek new ways to reinvigorate growth, underpinned by the launch of a cheaper ad-supported tier supported by Microsoft and a crackdown on the estimated 100 million people enjoying Netflix without paying and using someone else’s password by offering new paid sharing options.

Investors will be eager to hear news on how the new ad-supported tier is performing, but don’t expect too much considering it has said it won’t make a ‘material contribution’ to its results this quarter and is likely to be a slow and steady build over the coming quarters. There have been media reports that Netflix issued refunds to some advertisers after failing to provide enough viewers, suggesting a lacklustre start. However, analysts have largely shrugged-off the reports and said it is too early to judge the service, which they believe can still provide a new catalyst to revive growth in 2023 – but once again we do have some differing views on how successful this could be.

‘The advertising-based video on demand will be slow to kick in, but when it does (paired with password sharing changes), it should drive topline outperformance,’ said Jefferies analyst Andrew Uerkwitz.

On the other hand, Goldman Sachs has raised concerns that new pricing tiers could cause a ‘spin down’ into the lowest priced plans, especially if the economy falls into a recession and prompts people to tighten their belts. The jury is out in 2023.

Let’s turn to the financials. The recent pullback in the dollar should prove beneficial for the likes of Netflix, which earns around 60% of its sales from outside the US and books virtually all its costs in the greenback. The DXY US Dollar Index is down around 8.8% since early November, having risen to its strongest levels since early 2022 last year. This should lead to a milder impact from foreign exchange headwinds. Still, this will not be enough to stop Netflix reporting the most tepid rise in quarterly revenue on record this quarter, although this is expected to reaccelerate throughout 2023.

Meanwhile, costs are set to rise at a faster pace, and this will squeeze margins. Its operating margin is forecast to come in at just 4.3% in the fourth quarter – which would be the tightest margin reported since the start of 2016 and represent a significant contraction from the plus-19% reported in the first three quarters of 2022. That would also be at the bottom of its 4% to 8% guidance range for the quarter, which is usually its least profitable period as it tends to ramp-up spending on marketing and content for the new year. However, this too is expected to rebound to over 21% in the first quarter of 2023, in-line with its long-term goal of 19% to 20%.

The fourth quarter will also be poor in terms of cash generation, with analysts predicting a $266.7 million free cash outflow in the period. Still, the company is on course to deliver over $1.0 billion of free cashflow over the full year in 2022 and this is forecast to more than double in 2023.

What do markets expect from Netflix in 2023?

Currently, Wall Street believes Netflix will add 14 million paid subscribers in 2023. That would mark an acceleration from the 5.8 million additions pencilled-in for 2022, but still be one of the slowest rates of growth seen over the last decade.

Average revenue per user – which will become a more important metric to watch to evaluate the impact of its new pricing tiers – is forecast to continue rising to new record highs this year, driven by the addition of advertising dollars and price increases. Revenue is forecast to grow over 7% in 2023 thanks to faster subscriber growth. Netflix has said it is aiming to deliver double-digit revenue growth over the long-term, but markets don’t believe this will happen until 2024.

Earnings are set to decline in 2022 for the first time in seven years but is forecast to return to growth in 2023, with operating profit forecast to jump over 11% and contribute to a more tepid 2.9% rise in EPS.

Where next for NFLX stock?

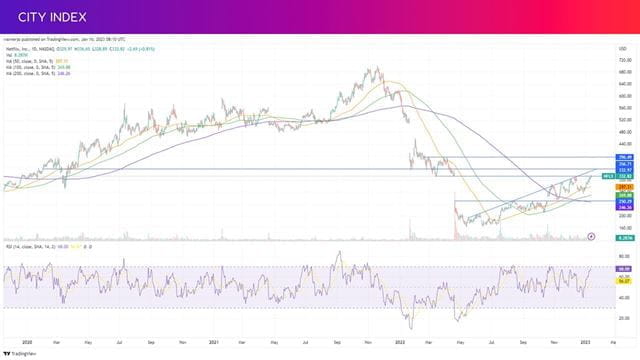

Netflix shares have risen over 90% since hitting their lowest level in almost five years back in May and the stock now trades at a nine-month high.

The stock continues to rise in the uptrend that can be traced back to those lows we saw in 2022, although it is yet to close the gap created in April 2022 when shares plummeted after it lost users for the first time on record. It needs to close above $333.22 to close it. We could see it climb toward $356.80, marking the level of support seen in early 2020, before eyeing a potentially larger move up to $396.50.

On the downside, we are seeing the RSI approach overbought territory to suggest that it may be more difficult to find higher ground going forward. The 50-day moving average has been providing a very loose form of support since last July but the 100-day moving average has proven more reliable. Notably, the 200-day moving average is currently aligned with the $250.30 level of resistance-turned-support seen throughout most of last year.

How to trade Netflix stock

You can trade Netflix shares as CFDs with City Index in just four easy steps.

- Open a City Index account, or log-in if you’re already a customer.

- Search for ‘Netflix’ in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Or you can practice trading risk-free by signing up for our Demo Trading Account.

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Equities articles

June 8, 2024 02:00 AM

June 3, 2024 05:56 AM

June 3, 2024 03:34 AM