When:

October 7thExpectations:

• EPS 7.5p, a 17.2% YoY rise on revenue of £31.7 billion.

• Pre- tax profits are due to be in the region of £944 million.

Covid revenues vs costs

Sales across all supermarkets, Tesco included are expected to be strong owing to lockdown and surging demand. Online sales are expected to be particularly strong. However, rising revenues have been offset by rising costs associated with the pandemic. Tesco recently hired 16,000 more staff for its online business.

Expectations are for those additional cost headwinds to be abating now. Meanwhile second quarter like for like sales are expected to be +6.3`% higher, excluding fuel and the Bookers wholesale arm.

Competition heating up

Competition feels like it is starting to heat up. Firstly, Marks and Spencer have teamed up with Ocado giving them an online presence and making them a force to be reckoned with. Secondly, and probably more concerning for Tesco is the development of the digital offering at Aldi, which now offers click and collect. Whilst Tesco was taking market share away from Aldi earlier in the year, this is looking like it won’t be trend that continues, particularly when economic conditions become more challenging and consumers could look more to to budget supermarkets such as Aldo and Lidl

New CEO new strategy?

These will be the first results under new boss Ken Murphy, who walked into the job just days ago. Here the key for the market will be outlook. Whilst it is clearly far too early for a strategic unveiling, any hints of changes to strategy will be lapped up.

Then there is Brexit – how could we forget? The Brexit issue continues to linger. It would appear that the broad consensus in the market currently is that the UK and the EU might have a bare bones trade agreement in place by early November. But that’s most certainly not in the bag. The disruption of a no deal Brexit would be considerable, whilst a drop sterling could push up the price of imported goods. Investors remain cautious.

Special Dividend

Finally, any update on the sales of the Asian business will be listened for carefully. Whilst the £5 billion proceeds were initially being ear marked for a special dividend, given the climate maybe Tesco would prefer to re-invest the funds?

What analysts say?

Of the 21 analysts covering the stock:

• Buy 14

• Hold 6

• Sell 1

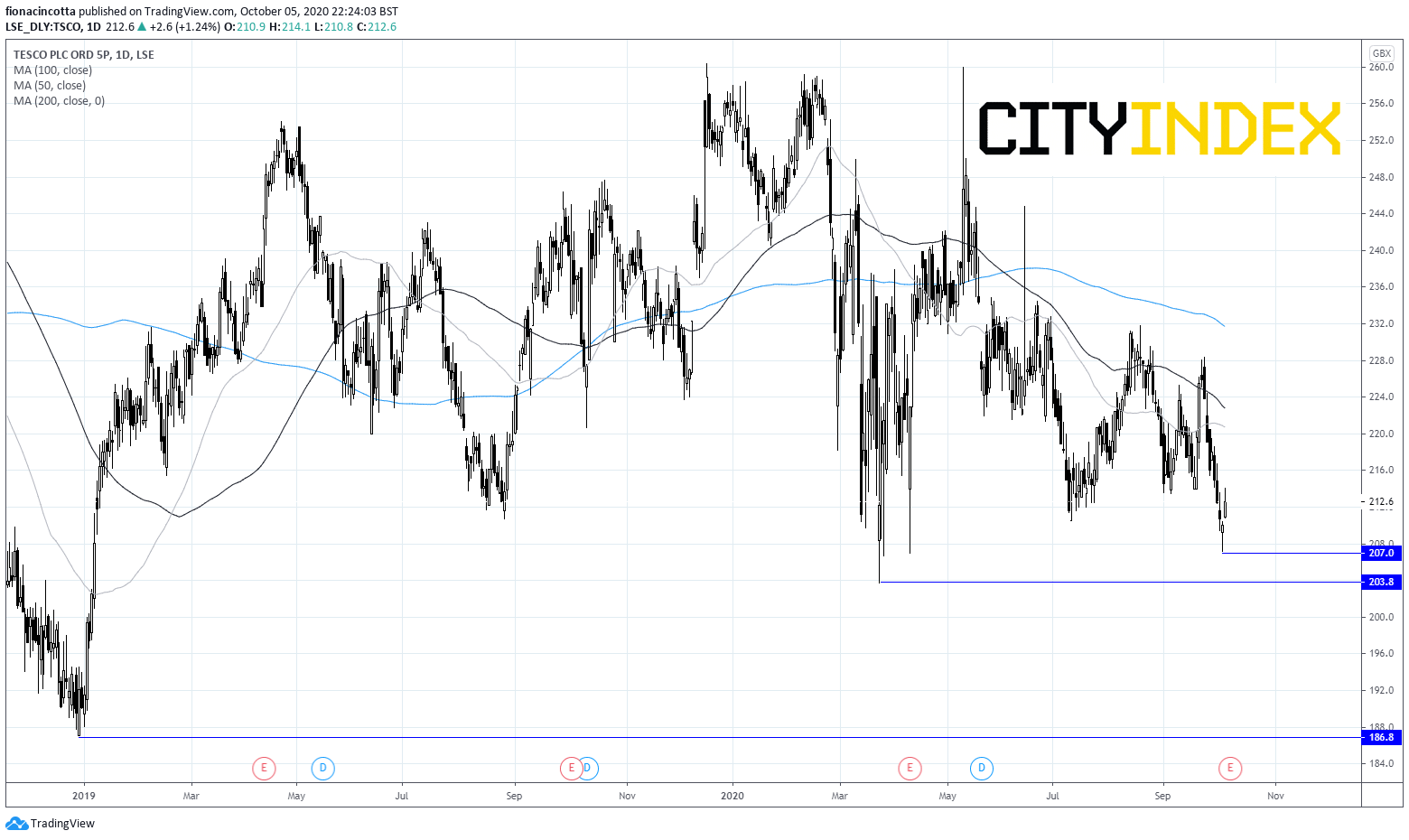

Tesco share price

Tesco’s share price saw spectacular, if short lived recovery from its mid-March low of 203p to a 250p peak. However, the surge lacked follow through, and the stocks has been in a downtrend since mid-April.

Tesco trades firmly below its 50, 100 and 200 DMA and below its descending trendline suggesting that there could be more weakness to come.

Support can be seen at Friday’s low of 207p , prior to the mid-March 203p low A break below here could see the stock look towards Dec 2018 lows of 185p . On the upside resistance can be seen at 220/2p 50 & 100 DMA, prior to 230p 200 DMA & horizontal support.

Tesco Chart

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Equities articles

June 8, 2024 02:00 AM

June 3, 2024 05:56 AM

June 3, 2024 03:34 AM