January 14, 2022 4:44 AM

Macro Overview

2021 saw the S&P500 hit fresh record highs on an astonishing 70 separate days. It is noticeable that the first two weeks of 2022 have seen a continuation of the volatility that marked the final months of 2021.

US inflation recently reached an almost 40 year high, hitting an annualised 7% in December. To counter this, the Federal Reserve has become increasingly hawkish.

In response, market expectations have shifted towards faster balance sheet normalization, with "quantitative tightening" to begin in September after Fed lift-off in June or possibly as early as March. A prospect that has rattled tech stocks.

Meanwhile, surging Omicron cases have left hospitals straining under the weight of numbers, disrupting global supply chains and grocery shelves empty. A development that will weigh on Q1 growth, likely to be reflected in some company's forward guidance.

Earnings

Despite the headwinds outlined above, S&P500 companies are expected to deliver strong earnings growth again. According to Factset, "For Q4 2021, the estimated earnings growth rate for the S&P 500 is 21.7%."

Presuming this is the confirmed growth rate for the quarter, it will mark the fourth straight quarter of earnings growth above 20% and lift full years earning growth to more than 40% for the full year.

Guidance

As noted by FactSet in the first week of January, "93 S&P 500 companies have issued EPS guidance for the fourth quarter. This number is slightly below the 5-year average of 100. Of these 93 companies, 56 have issued negative EPS guidance, and 37 have issued positive EPS guidance."

This marks the first time since Q2 2020 that S&P500 companies have issued more negative EPS guidance than positive guidance. Despite this, the estimated (year over year) earnings growth for Q4 2021 is above the expectations from the start of Q4.

Sector Performance

As noted by Factset, the Energy sector led by companies such as Exxon Mobil and Chevron have recorded the largest percentage increase in estimated (dollar-level) earnings of all eleven sectors since the start of the quarter at 40.8% (to $28.1 billion from $20.0 billion).

The Consumer Discretionary sector led by Amazon.com has recorded the largest percentage decrease in estimated (dollar-level) earnings of all eleven sectors since the start of the quarter at -15.1% (to $27.1 billion from $32.0 billion).

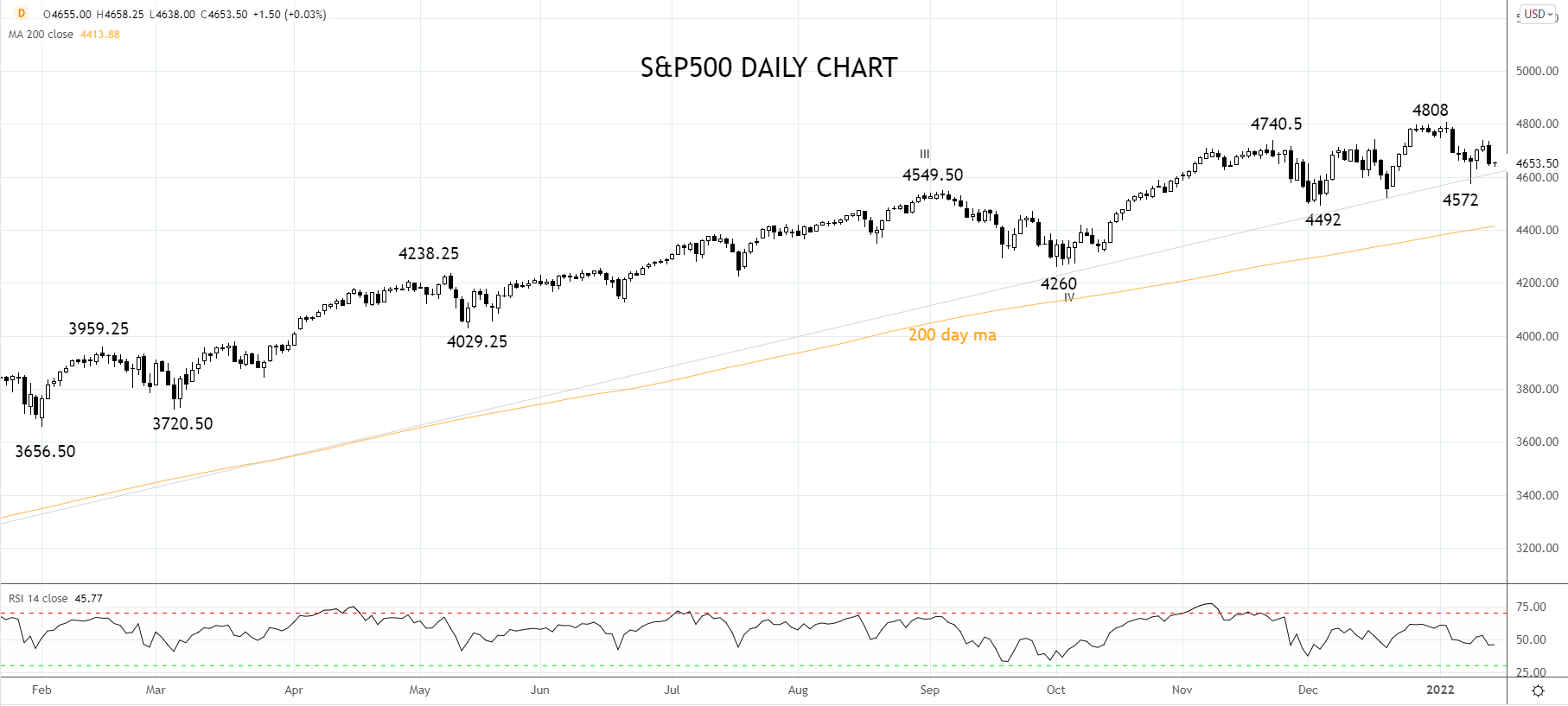

S&P500 Technical Outlook

The overnight decline has the S&P500 eyeing important trendline support at 4620/00ish from the March 2020, 2174 low.

Providing the S&P500 remains above 4620/00 (closing basis), look for a push towards 5000 during the first quarter of 2022.

However, should a sustained break below 4620/00ish occur, the risks are for a deeper pullback towards 4400.

Source Tradingview. The figures stated areas of January 14th, 2022. Past performance is not a reliable indicator of future performance. This report does not contain and is not to be taken as containing any financial product advice or financial product recommendation

How to trade with City Index

You can trade with City Index by following these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Earnings season articles

July 18, 2024 02:46 PM

July 15, 2024 10:33 AM

April 25, 2024 03:09 PM

April 23, 2024 01:15 PM