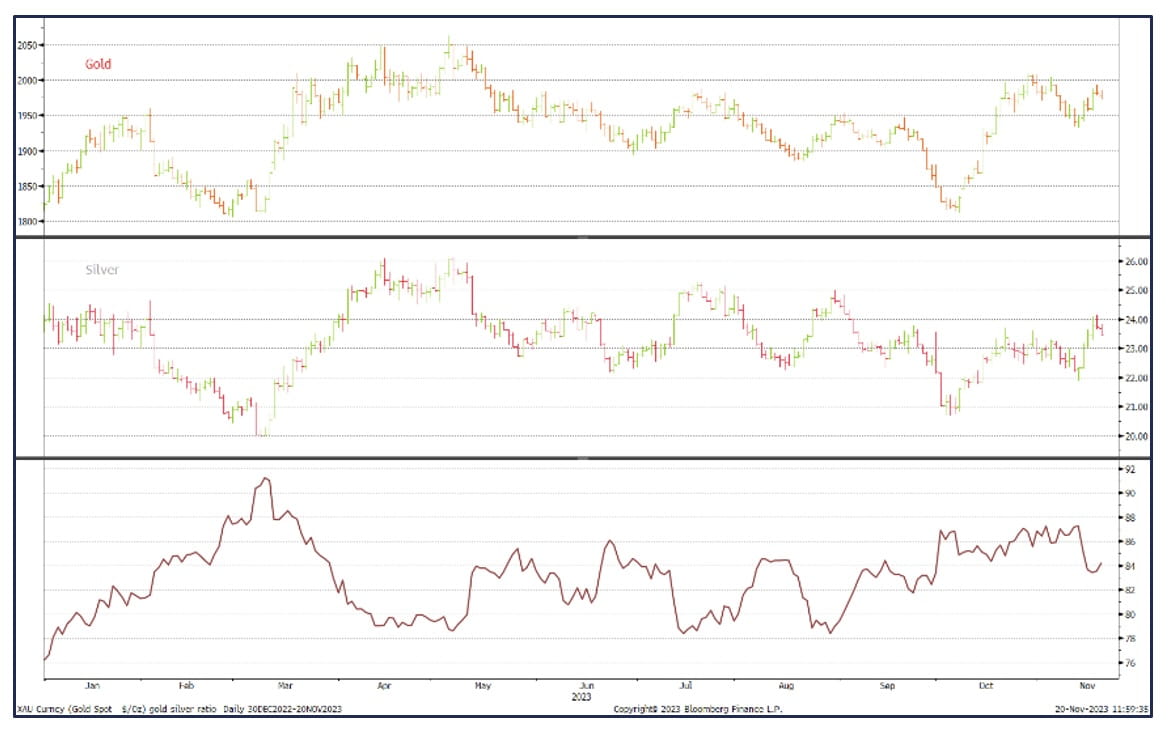

Gold has traded in a $61 range over the past fortnight and now holds around $1,970. Silver has been more positive; after dropping towards $22, it rallied hard to more than $24 before easing. While gold’s range was 3.2% (as a percentage of the low) over the week, silver’s was 10.3%, more significant than the average 2.0-2.5 beta, and much of the silver move looks like short covering.

There still needs to be an overriding force to move precious metals out of their prevailing ranges. Attention should now turn to the Middle Eastern envoys going to China and other Southeast Asian nations to try and broker peace in the Israel/Hamas conflict; if stalemate persists, then gold should continue to find some support, but progress could take prices lower.

Immediate outlook

The past fortnight can be divided into two more or less equal parts, with gold and silver prices declining in the first half and rallying in the second. In the first week, the markets were pressured as several Fed officials took a cautious stance over the prospect of interest rate cuts. Most notably, towards the end of the week, Fed Chair Powell said that the Fed would not compunction about additional policy tightening if necessary. This helped to keep Gold on the defensive, even though he was saying nothing different from previously, noting that the Fed would proceed with care (as they don’t want to derail the recovery).

Gold still consolidating

Source: Bloomberg, StoneX

Since then, the atmosphere has changed slightly with a series of numbers suggesting that the recovery is slowing (retail sales undershooting, a 0.5% fall in the monthly Producer Price Index, a fall in manufacturing production capacity utilization to 74.7%, and falls in both import and export prices, although the latter could be a function of dollar strength). This helped give gold some renewed strength, although ranges have been narrow, as noted above.

Gold, silver, and the ratio: year-to-date

Source: Bloomberg, StoneX

Silver’s move in the second half of the period might be surprising given that 60% of silver demand is industrial and that gold wasn’t moving by much. Still, there were two days when the rally was short and sharp, suggesting short covering and technically driven activity.

Fundamentals

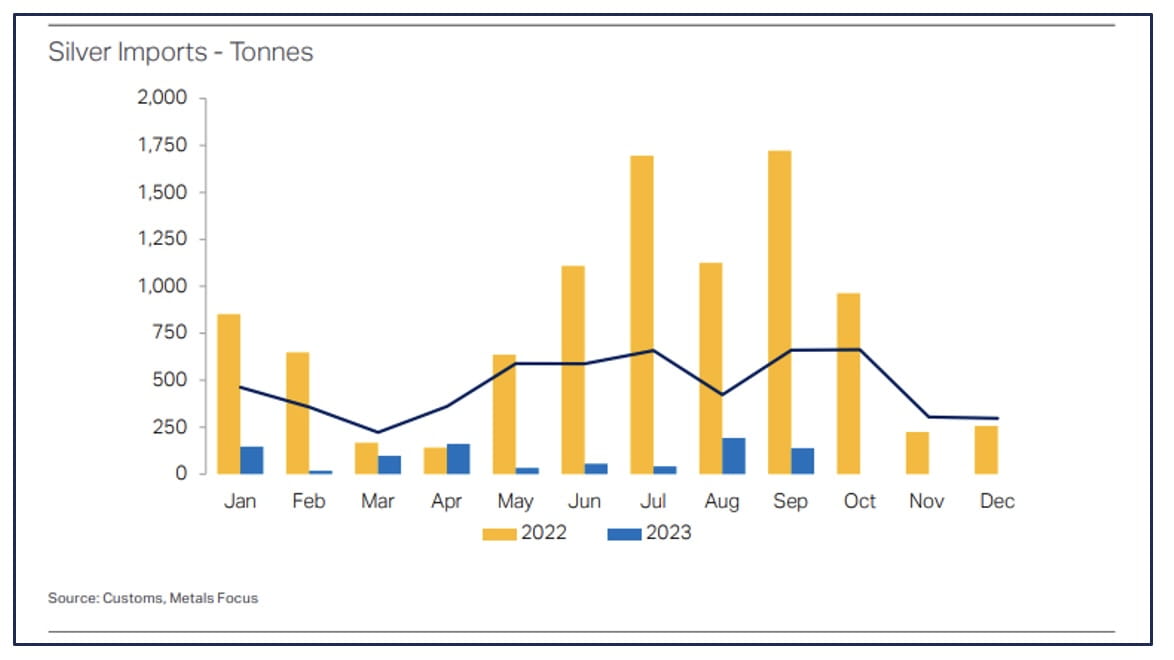

At the fundamental end of the market, Dhanteras and Diwali were celebrated last week; traditionally, the most auspicious days of the Hindu calendar for giving and receiving gifts, notably gold. This year was lively as post-COVID pent-up demand coursed through the Indian populace. In dollar terms, gold imports into India in October were reportedly up 95% to $7.2 billion, and silver imports were up 125% to $1.3 billion. Demand was robust despite high prices, particularly for silver.

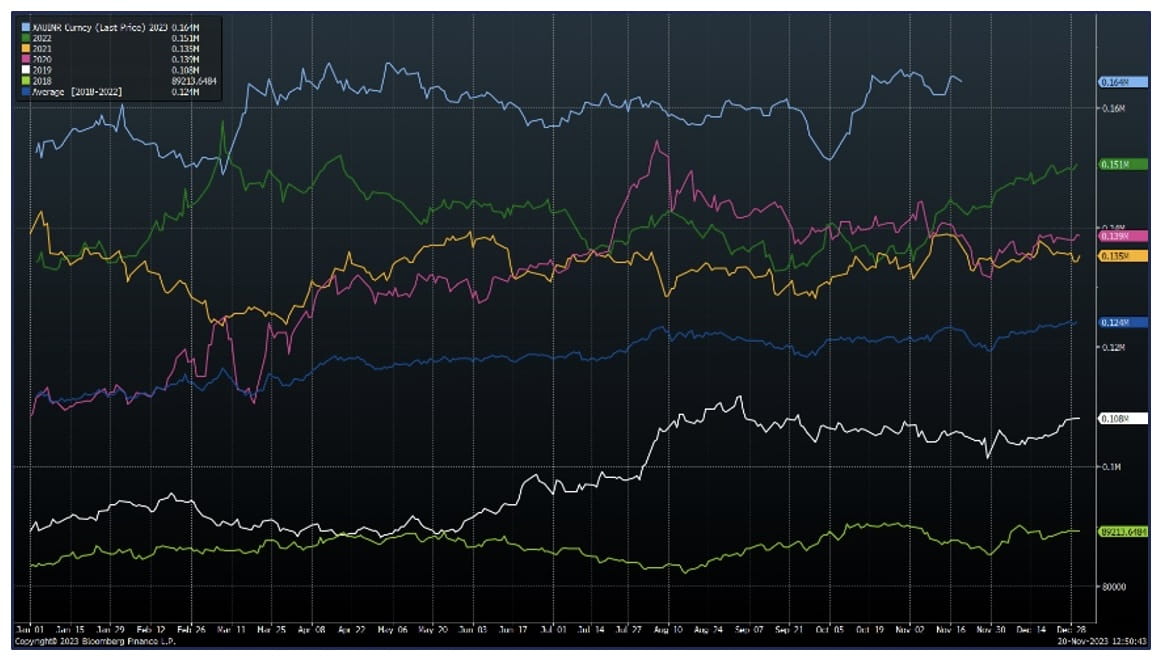

Gold in rupees: seasonality chart

Source: Bloomberg, StoneX

It is also interesting to note that there was a substantial outflow of silver from the LBMA vaults in October, with some 1,192 tonnes (4%), which could have been destined for India. Metals Focus regularly monitors Indian flows, and the most recent publication says that preliminary figures show Indian silver imports of 1,180 tonnes; this is a 23% year-on-year jump and 757% month-on-month.

The chart suggests cumulative imports over January-September were only around 970 tonnes (and compare that with a typical 4,000-6,000 tonnes per annum, historically). 2000-2001 were much lower, while 2022 was sky-high, with about 10,000 tonnes feeding the pent-up post-COVID interest. It looks like they were on fire in October, and there had been a reasonable dip in the rupee price during the month. India is unlikely to be the answer to the LBMA drawdown, but it must have had an influence.

Silver Imports

Source: Metals Focus

Futures positioning

Gold dropped from $2,007 on 30th Oct to a low of $1,932 on the 13th of November, from which the rally started, and the spot closed at $1,964 on the 14th of November.

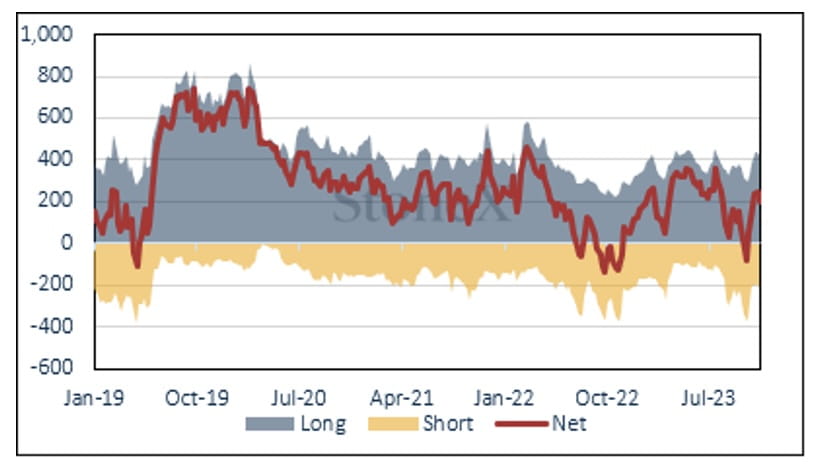

Negative sentiment is returning for the most part, with longs down by 24 tonnes (5.5%) and shorts up 19.4 tonnes or 10%. Net longs were down 18% to 200 tonnes from 243 tonnes and a twelve-month average of 194 tonnes.

Gold COMEX positioning, Money Managers (tonnes)

Source: CFTC, StoneX

Silver dropped from $23.30 on the 3rd of November, bottomed at $21.88 on the 13th of November, and closed at $23.07 on the 14th of November.

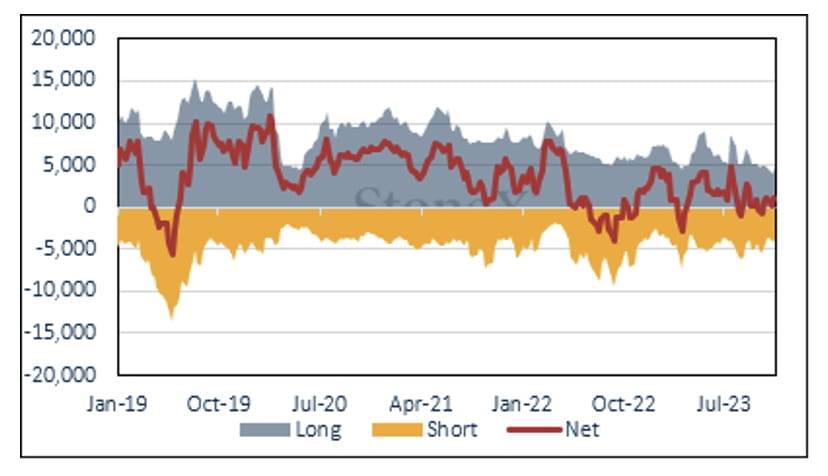

The reverse of gold with a 20% (819 tonnes) increase in longs and a 5.1% (207 tonnes) contraction in shorts; net long increased from 56 tonnes to 1,078 tonnes against a twelve-month average of 1,761 tonnes.

COMEX Managed Money Silver Positioning (tonnes)

Source: CFTC, StoneX

Exchange Traded Products

In the ETP sector, the first half of November has seen the sellers again with the upper hand, with a loss of 16 tonnes in the period to 10th November and an estimated four-tonne contraction in the following week. There has been some scattered buying, generally at the lower prices, and no interest in the rally, but nothing of note, leaving the holdings at the end of last week at 3,234 tonnes, a drop year-to-date of 238 tonnes. For context, world gold mine production is roughly 3,700 tonnes.

Silver has been similar, with sporadic days of net purchase, but sentiment has remained cautious, unlike the slight shift in sentiment among the Money Managers on COMEX. Unlike gold, there was little by way of reaction to falling prices; buying had no actual pattern to it. For November, the funds have shed a net 174 tonnes (less than 1%) to 21,961 tonnes. World silver mine production is in the region of 26,000 tonnes per annum.

Taken from analysis by Rhona O’Connell, Head of Commodity Market Analysis for EMEA & Asia, StoneX Financial Ltd.

Contact: Rhona.Oconnell@stonex.com.

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest US articles

January 5, 2024 03:09 PM

January 4, 2024 06:55 PM

January 3, 2024 07:55 PM

January 2, 2024 08:00 PM