Banks, which comprise a large part of the Official Sector, are building higher gold reserves: “Our 2023 survey revealed that 24% of central banks intend to increase their holding reserves in the next 12 months, according to survey by the World Gold Council (WGC) in May this year. Central banks’ US dollar holdings were forecast to decline, in the same survey: “Half of central banks surveyed believe the percentage of reserves in USD in five years will be between 40-50%, while just over a quarter believe it will remain unchanged.” According to the IMF, the percentage was 60% at the start of the year that, down from 71% at the start of the century.

This move from Dollars to gold holdings implies a weakening US dollar and stronger gold price. The move is also due in part to recent geopolitical tensions, and is supportive, in a subtle but important way, for the gold price. Gold is now trading at $1,964 per ounce, having traded around $2,000 for the past several weeks.

We estimate that the proportion of gold in Official Sector foreign exchange reserves, combining gold and FX reserves, was around 15% at the end of 2022 (using a $2,000/ounce gold price). Arguably this is skewed towards high gold holdings by a few nations as legacy of the gold standard, and because the US can’t hold US dollars in its forex reserves. If we strip out legacy gold holdings, average central bank holdings are around 7%. This happens to be in the middle of the range recommended for portfolio holdings by quants.

The WGC estimates that net central bank buying globally amounted to 1,079 tonnes last year, sentiment which is pretty much unchanged this year. Data for the first quarter of 2023 show net central bank purchases of 228 tonnes, so if this rate were to be maintained then net purchases would exceed 900 tonnes this year. First quarter purchases were 34% higher than the previous first-quarter record, in 2013, but lower than the latter two quarters of 2022.

Activity in April looks at first sight to show a shift in sentiment with net selling of 71 tonnes by the Official Sector, but a more detailed analysis shows that this is not the case. In fact, Turkey was a net seller of 81 tonnes, feeding domestic gold demand to the tune of one to one and a half tonnes daily during the period when gold imports were partially suspended and domestic buying was extremely strong. Other, smaller sellers were central banks in gold producing countries: Kazakhstan, Uzbekistan and the Kyrgyz Republic.

Also in April, the People’s Bank of China were reported buyers, according to IMF data, at 15 tonnes for the month, lifting the past six months to 128 tonnes for a reported total of 2,076 tonnes. Priced at $2,000 per ounce, this is 4% of the total People’s Bank of China combined gold and foreign exchange reserves, just over half the average among those central banks that do not historically have large gold holdings.

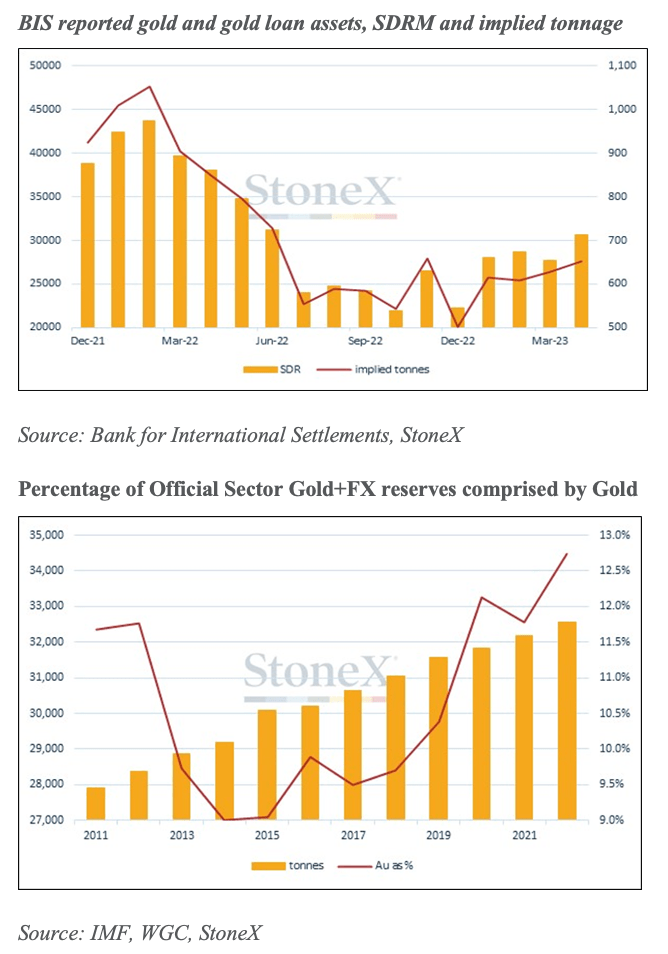

Against this trend, the Bank for International Settlements (BIS) reported gold holdings dropped from 510 tonnes to 102 tonnes over the past year. The BIS has commented, in its site, relating to the Annual Report for 2022, that “the gold balance included 102 tonnes in the Bank's own investment portfolio”. BIS is an international financial institution and is the bank for member central banks and can hold assets on their behalf.

We can deduce a net intra-year fall of 421 tonnes, very close to the 408 tonnes drop implied by IMF figures. This suggests that BIS gold holdings, separate from its own portfolio, stood at 400 tonnes, and the difference with the residual figure at end-2022 is notional, suggesting that third party material with the BIS was more or less unchanged over the year. We cannot immediately be certain where the balance of gold went.

Analysis by Rhona O'Connell, Stone X Head of Market Analysis.

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest US articles

January 5, 2024 03:09 PM

January 4, 2024 06:55 PM

January 3, 2024 07:55 PM

January 2, 2024 08:00 PM