Bullish factors

- Uncertainty about the viability of budget targets in 2024 may increase risk premium requirements by investors for Brazilian assets and diminish foreign investments, weakening the real.

- Argentine elections can increase the perception of risks for other countries in the region and temporarily decrease managed money for Brazil, weakening the real.

Bearish factors

- Disclosure of the minutes of the FOMC decision can reinforce the perception that American interest rates have already peaked and contributed to weakening the dollar..

Our Brazil team provides regular weekly coverage of the Brazilian economy and the outlook for the Real, accessible by clicking the link in the banner above.

The week in review

The week was marked by the release of milder-than-expected data for the American economy, reinforcing the perception that the Federal Reserve will no longer raise the country's interest rates and promoting a global weakening of the American currency. The strengthening of the real was constrained by the prolongation of fiscal fears amid uncertainty about the possibility of changing the budget target for 2024.

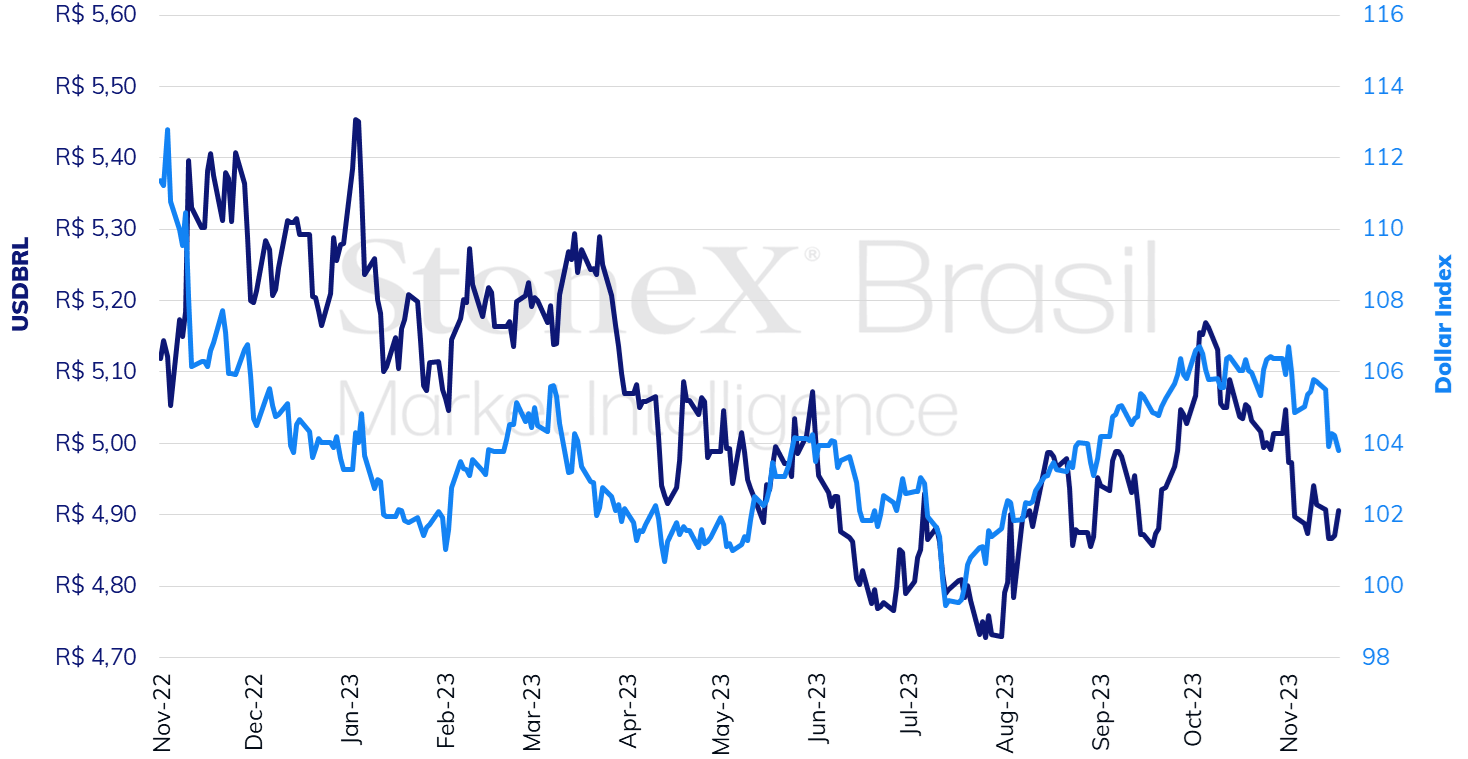

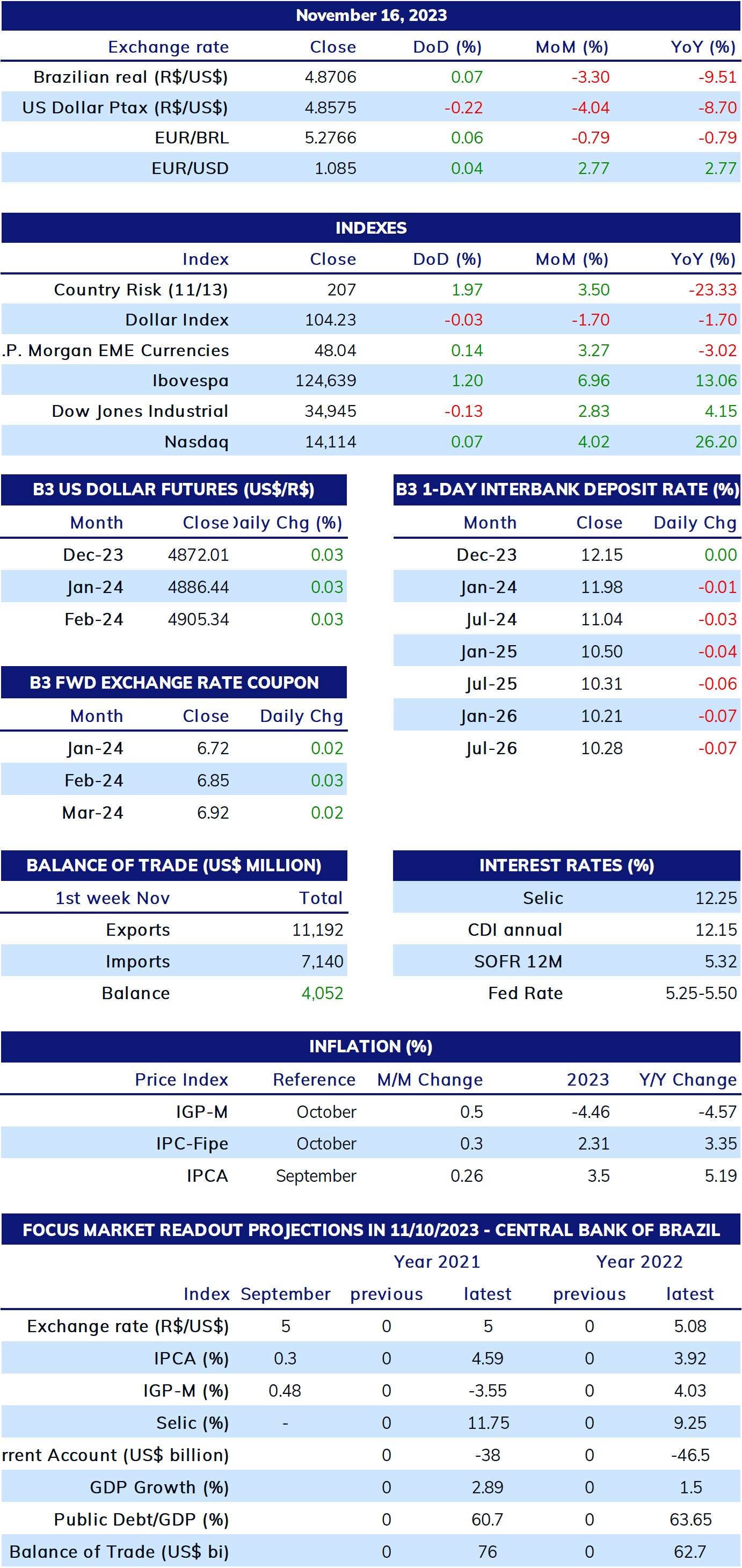

The USDBRL ended the week lower, closing Friday's session (17) at BRL 4.906, a weekly decrease of 0.2%, a monthly decrease of 2.8%, and an annual decrease of 7.1%. The dollar index closed Friday's session at 103.8 points, a change of -1.8% for the week, -2.0% for the month, and +0.5% for the year.

USDBRL and Dollar Index (points)

Source: StoneX cmdtyView. Design: StoneX

HIGHLIGHTS: Fiscal target and LDO

Expected impact on USDBRL: bullish

This week's highlight should be the vote on the Budget Guidelines Law (LDO, in Portuguese) bill in the Joint Budget Committee (CMO, in Portuguese). After weeks of uncertainty and behind-the-scenes discussions about the possibility of changing the target fiscal goal for the 2024 Budget, the federal government has decided not to submit an amendment and to maintain the original objective of a zero primary deficit in the LDO. The rapporteur, Deputy Danilo Forte (União-CE), is expected to present the report for consideration on Monday (20) by the CMO and vote on it this week. Then, the LDO will go to the Plenary of the National Congress, which is expected to vote in the next two weeks, and then the Annual Budget Law (LOA) must be voted on, with the deadline for Plenary voting scheduled for the last week before the recess (December 18-22).

If, on the one hand, maintaining fiscal goals at this moment is a victory for the government's economic team and helps in defending the maintenance of the target, behind the scenes, according to reports from specialized media, it still seems certain that the change in the target will occur in the future, but through a bill, which will require a majority of deputies and senators, probably in March, when the first bimonthly report on revenues and expenses is presented. In this way, in addition to opting for a strategy that may require legislative mobilization, which has been a weak point of this government, it is not possible to recover the credibility of fiscal policy management, which may maintain higher perceptions of fiscal risks to Brazilian assets and increase the requirement of risk premiums by investors, weakening the real.

FOMC Minutes

Expected impact on USDBRL: bearish

This week, the release of the minutes from the last meeting of the Fed's Federal Open Market Committee (FOMC), which took place between October 31 and November 1, should also be highlighted. The decision of the Committee to keep the American basic interest rates stable and a speech considered more balanced indicated that the monetary tightening cycle of the institution may be nearing its end. This perception was reinforced by the release of economic data that were milder than expected for October, boosting a sharp appetite for risks among investors. In this way, the month of November is being marked, so far, by a significant global weakening of the American currency, a significant decline in yields of US Treasury bonds, and an appreciation of risky assets, such as paper, commodities, and currencies of countries that export primary products.

In a certain sense, the minutes will reflect an outdated situation since the discussions at the end of October were centered on concerns of "higher for longer" economic data for September warmer than experts' expectations and continued pressure from Treasury yields. On October 19, for example, yields on 10-year Treasuries had surpassed 5% p.a. for the first time since 2007, compared to 4.42% p.a. this Friday, November 17. Similarly, the speech of Federal Reserve authorities is still cautious and calls for patience, stating that the inflationary reduction so far is welcome but that any price reacceleration can provoke a new interest rate hike. Market agents want to explore the considerations about the interest rate trajectory, as there is almost consensus that a new hike is unlikely and that the Fed should keep rates unchanged for some time before starting a cycle of cuts.

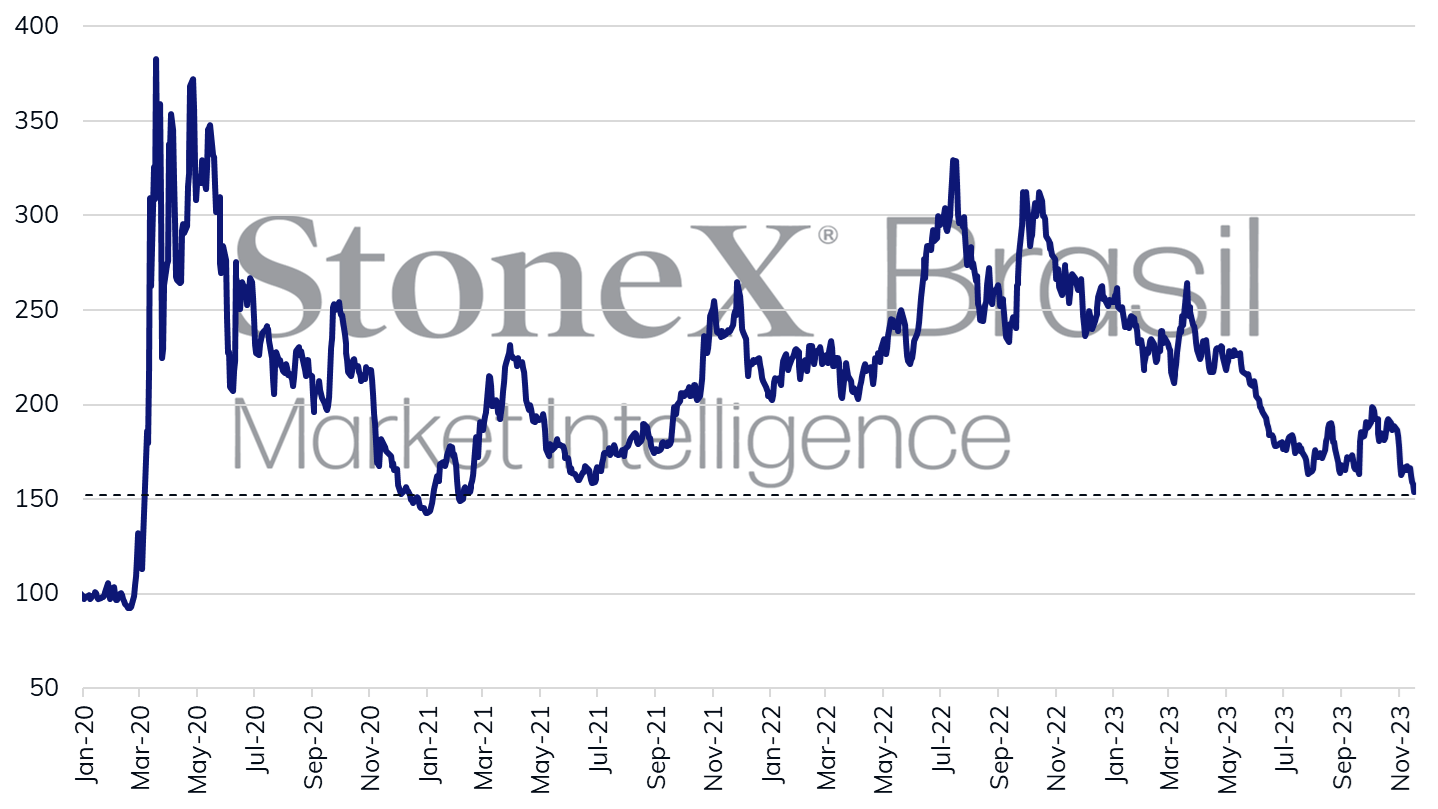

For Brazil and the real, the boost in risk appetite meant a significant fall in the rating of Brazilian bonds, with the spread of Credit Default Swap (CDS) contracts reaching the lowest value since February 2021. Additionally, there was a higher demand for Brazilian assets, contributing to the strengthening of the real, which can be observed, for example, in the balance of foreign capital flow on the B3 during the month.

Spread of Brazil's 5-year Credit Default Swap (CDS) contracts (basis points)

Source: Bloomberg. Design: StoneX.

Foreign capital flow balance on the B3 as of November 14, 2023 (BRL/billion)

Source: B3. Design: StoneX.

Source: B3. Design: StoneX.

Argentina's elections

Expected impact on USDBRL: bullish

This Sunday (19), the second round of presidential elections in Argentina occurs between candidates Javier Milei and Sergio Massa. The voting intention surveys show a balanced race, usually with differences within the margins of error. Any elected candidate will face an economy with very difficult economic challenges, such as high inflation rates and a shortage of international reserves. Suppose the current Minister of Economy Massa represents the continuity of a government with many failures. In that case, the oppositionist and ultraconservative Milei accumulated controversial statements such as abandoning Mercosur if elected and not doing business with Brazil.

Key Indicators

Sources: Central Bank of Brazil; B3; IBGE; Fipe; FGV; MDIC; IPEA and StoneX cmdtyView.

Sources: Central Bank of Brazil; B3; IBGE; Fipe; FGV; MDIC; IPEA and StoneX cmdtyView.

Analysis by: Leonel Oliveira Mattos (leonel.mattos@stonex.com), Alan Lima (alan.lima@stonex.com), and Vitor Andrioli (vitor.andrioli@stonex.com).

Translation by Rodolfo Abachi (rodolfo.abachi@stonex.com).

Financial editor: Paul Walton (paul.walton@stonex.com).

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest US articles

January 5, 2024 03:09 PM

January 4, 2024 06:55 PM

January 3, 2024 07:55 PM

January 2, 2024 08:00 PM