The macro, micro and technical outlook for base metals has been pretty bearish, and it is not surprising that the base metals price index has fallen to six months lows. Market sentiment towards the outlook for a rebound in economic growth within China weakened this year with the release of disappointing economic data.

Nevertheless, we are starting to see signs of a pickup in physical demand in China, a major swing economy for metals. There are emerging signs that demand weakness could be bottoming out in the world’s largest producer and consumer of base metals. Let’s focus on copper: we have started to see signs of a pickup in the physical import premium for the first time in six weeks, record levels of domestic production, and reducing on-warrant inventory.

While we remain cautious of a recovery in Chinese demand, a marathon not a sprint, the worst might be over. Nickel, Zinc and Lead were the worst performers this year, down by almost 30%, 20% and 10%, respectively.

Macro headwinds

- Chinese economic readings indicate recovery will take time

- Weakening sentiment for ex-China growth in the second half of the year

- A strengthening US dollar putting downward pressure on prices

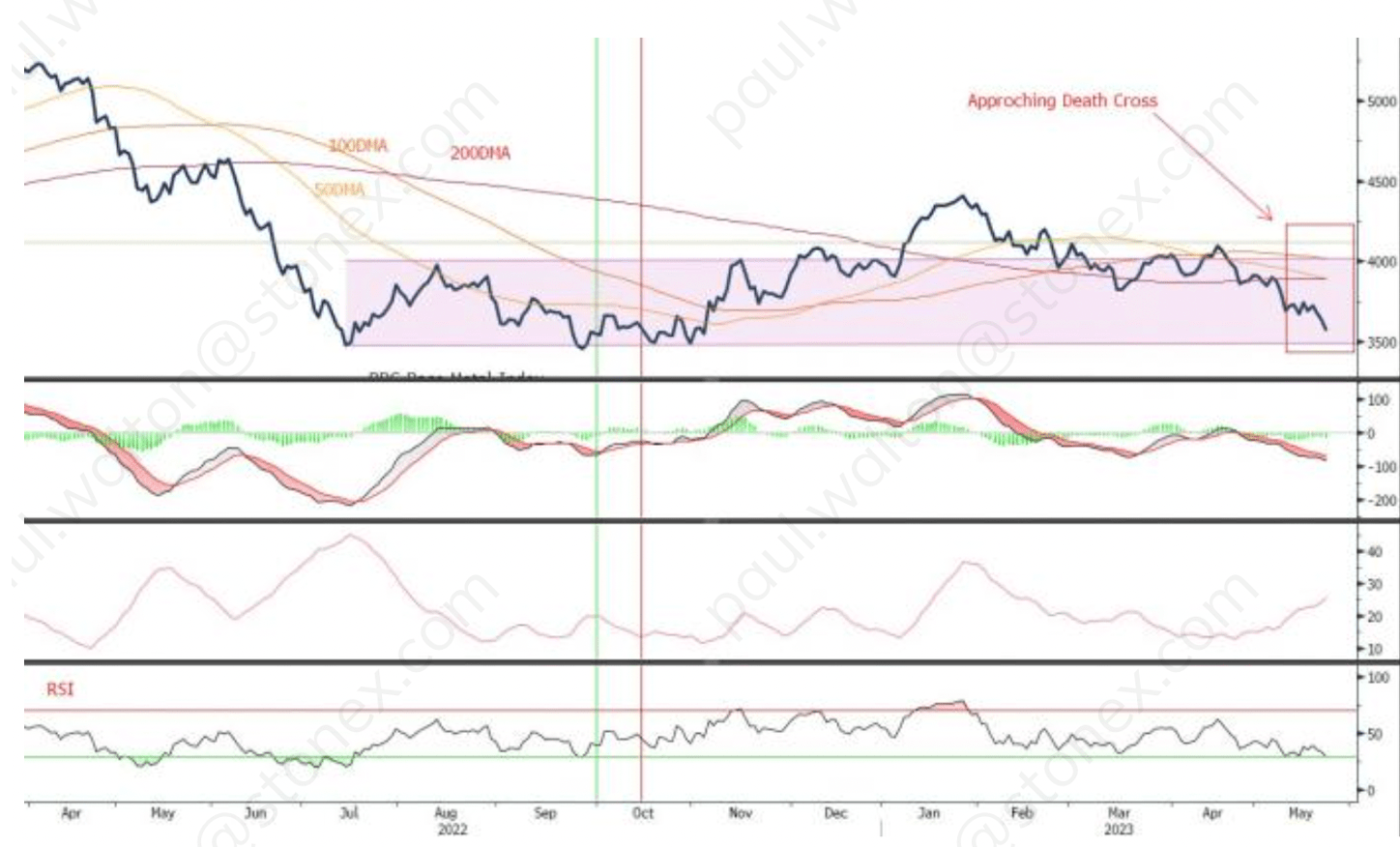

Technical Picture

- The base metal index’s technical view has grown increasingly bearish since mid-April, with the 50-day moving average (DMA) moving below the 100-DMA

- If the 50-DMA moving moves below the 200-DMA, it will indicate a so called ‘death cross’, which is a very bearish technical signal.

LME Base Metal Index – Technical Analysis

Source: Bloomberg, StoneX.

Micro factors

- A sharp inflow of base metal stocks into LME warehouses caused concerns over global demand

- Large copper inflows started in Asian warehouses, more recently spreading to US-based warehouses.

- Copper inventories at the London Metal Exchange (LME) rose 180% in just over a month (reversing a 55% decline in stocks prior to this period since the start of the year)

- The LME Cash – 3 month spread as a result, rose to its largest contango on record, at $66/tonne.

An end in sight to weak demand?

Collectively, these factors indicate that demand on a global basis is weak, especially within China, in which the Q2 period traditionally signifies peak demand for construction. However, if we continue to see a drawdown in domestic Chinese stocks and an increased appetite for imports into the country, then perhaps we have past the worst point in the cycle. Meanwhile, if raw material stocks continue to build in LME warehouses, the LME prices will underperform those of SHFE prices, opening up arbitrage opportunities.

Natalie Scott-Gray, Senior Metals Analyst

natalie.scott-gray@stonex.com

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest US articles

January 5, 2024 03:09 PM

January 4, 2024 06:55 PM

January 3, 2024 07:55 PM

January 2, 2024 08:00 PM