H2 Forex Outlook

Heading into 2023, it looked like major central banks across the developed world were nearing the end of their rate hike cycles.

The situation with the Bank of Canada provides an indicative example: BOC Governor Tiff Macklem and company announced a “conditional pause” to interest rate increases in January, suggesting that they were likely done raising interest rates as long as “the economy develops as we think it will and inflation continues to fall.”

As it turns out, that pause lasted less than five months, and the Bank of Canada was forced to start raising interest rates again in June after the economy grew at a 3.1% annualized rate in Q1 and inflation started rising again in April. As of writing in mid-June, traders are now pricing in yet another rate hike from the BOC in Q3 and interest rates to remain at that new peak near 5.00% for more than a year.

Of course, most central banks didn’t even reach the “pause” stage in H1, but it’s clear that the global economy (and by extension, the labour market and inflation) outperformed expectations, forcing central banks to keep the proverbial “pedal to the metal” with interest rate increases beyond what they had expected.

As it often is, the performance of different currencies in the first half of the year was driven by these central bank interest rates, or more accurately, changing expectations for central bank interest rates, with currencies like the British pound, Canadian dollar, and Euro seeing the largest upward revisions to interest rate expectations, while the Japanese yen continues to struggle as the Bank of Japan remains stuck at 0% interest rates:

Source: FinViz. Chart created June 22, 2023.

Below, we take a high-level look at the outlook for the three most-traded currency pairs and their respective central banks, but remember to check our News and Analysis pages for the latest developments and levels to watch as we move through the second half of the year and beyond.

EUR/USD

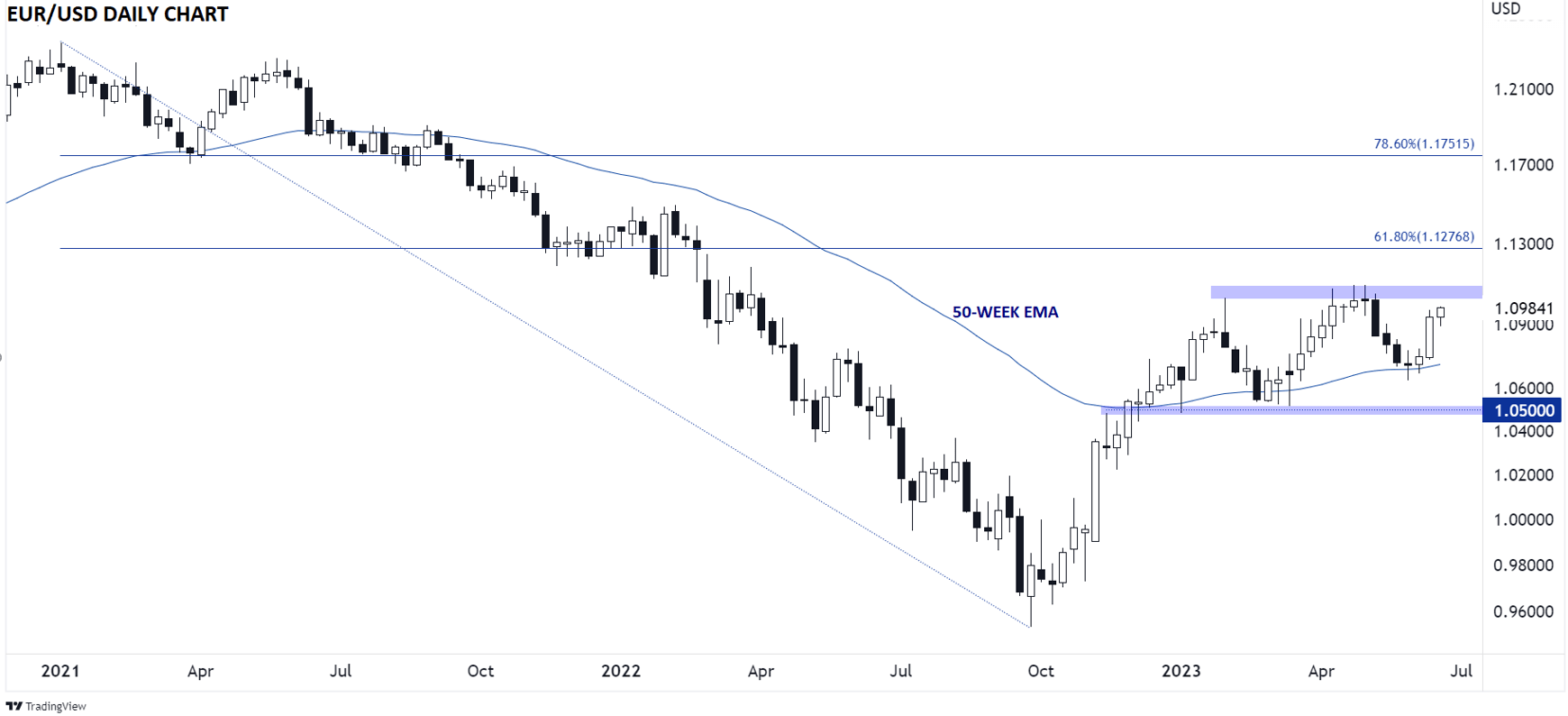

As we noted in our Macroeconomic Outlook, inflation remains higher in the Eurozone than in the US, so it’s not surprising that traders expect the ECB to raise interest rates more aggressively from here than the Federal Reserve, and that has certainly helped support the euro at the expense of the greenback.

However, with many concerning economic indicators on both sides of the Atlantic (contracting money supply, falling leading economic indicators, inverted yield curves galore, etc), one overarching theme to watch in the second half of the year will be whether a central bank rate hike in the hand is worth two in the bush, to mix metaphors. In other words, if the global economy finally starts to slow, expectations for future interest rate increases are likely to be cut faster and more easily than current interest rates.

In that scenario, EUR/USD could be vulnerable to a pullback, especially with rates approaching their highest levels since March 2022 in the 1.1100 area. On the other hand, continued strength in the global and Eurozone economy would allow the ECB to “catch up” toward the Fed’s interest rate, with a EUR/USD breakout above 1.1100 opening the door for a continuation toward the longer-term 61.8% Fibonacci retracement near 1.1275 next.

Source: TradingView, StoneX

GBP/USD

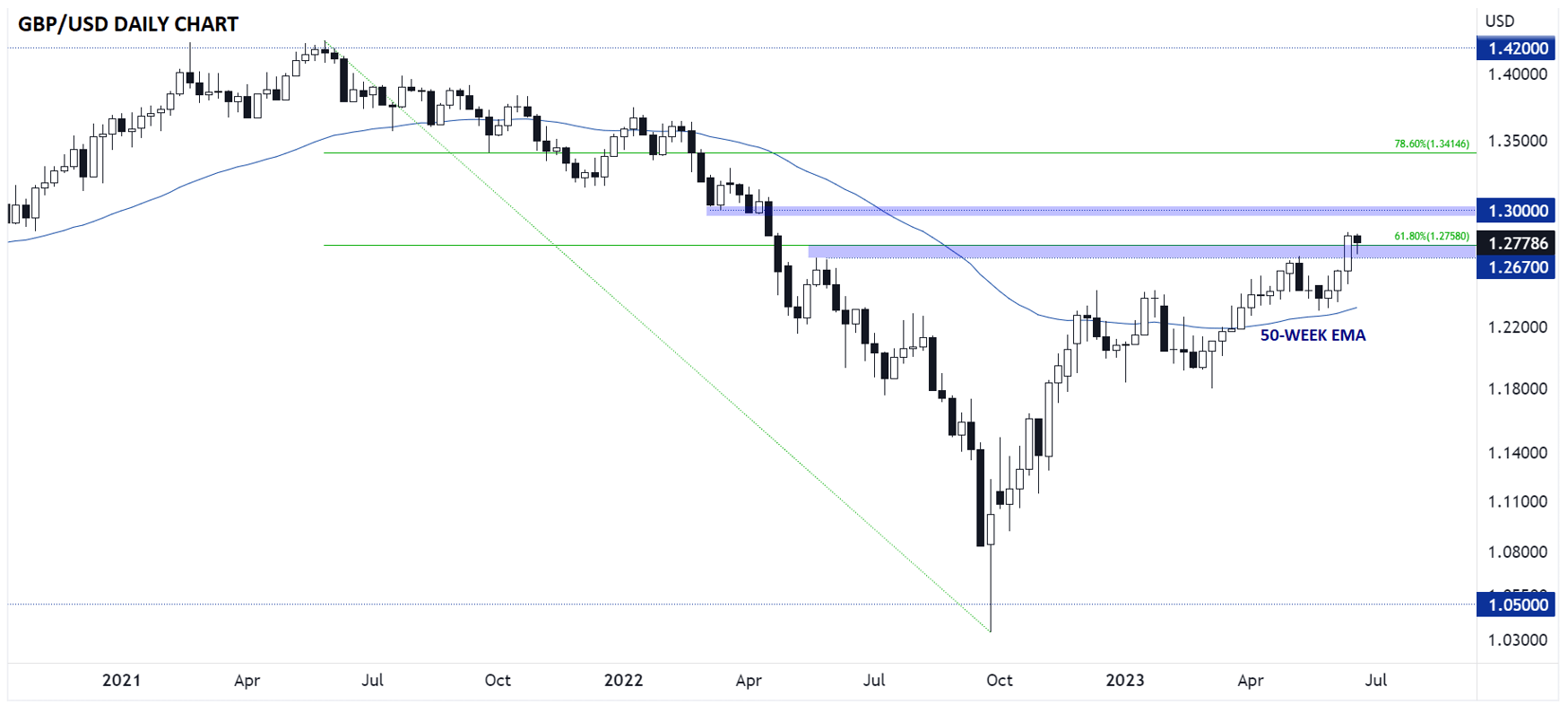

In the above section, we introduced the idea that expectations for future interest rate increases are the first and easiest change that the market can make if growth slows, but that perspective is even more relevant to the pound, where traders are pricing in nearly 100bps of interest rate increases from the BOE in the second half of the year, with rates projected to top out above 6.00% early next year.

The economic situation in the UK is arguably more tenuous than in Europe, given the UK’s tighter labour market and more entrenched inflation, so the BOE may nonetheless be forced to raise interest rates to a higher peak regardless, and that expectation has made sterling the strongest major currency through the first half of the year.

Looking at the chart below, continued strength in GBP/USD could take the pair toward the confluence of previous-support-turned-resistance and the key psychological level at 1.3000, with a break above that area potentially opening the door for a continuation into the mid-1.30s. Meanwhile, a bearish reversal here (likely as a result of falling expectations for future interest rate hikes) could expose the 50-week EMA under 1.2400 next.

Source: TradingView, StoneX

USD/JPY

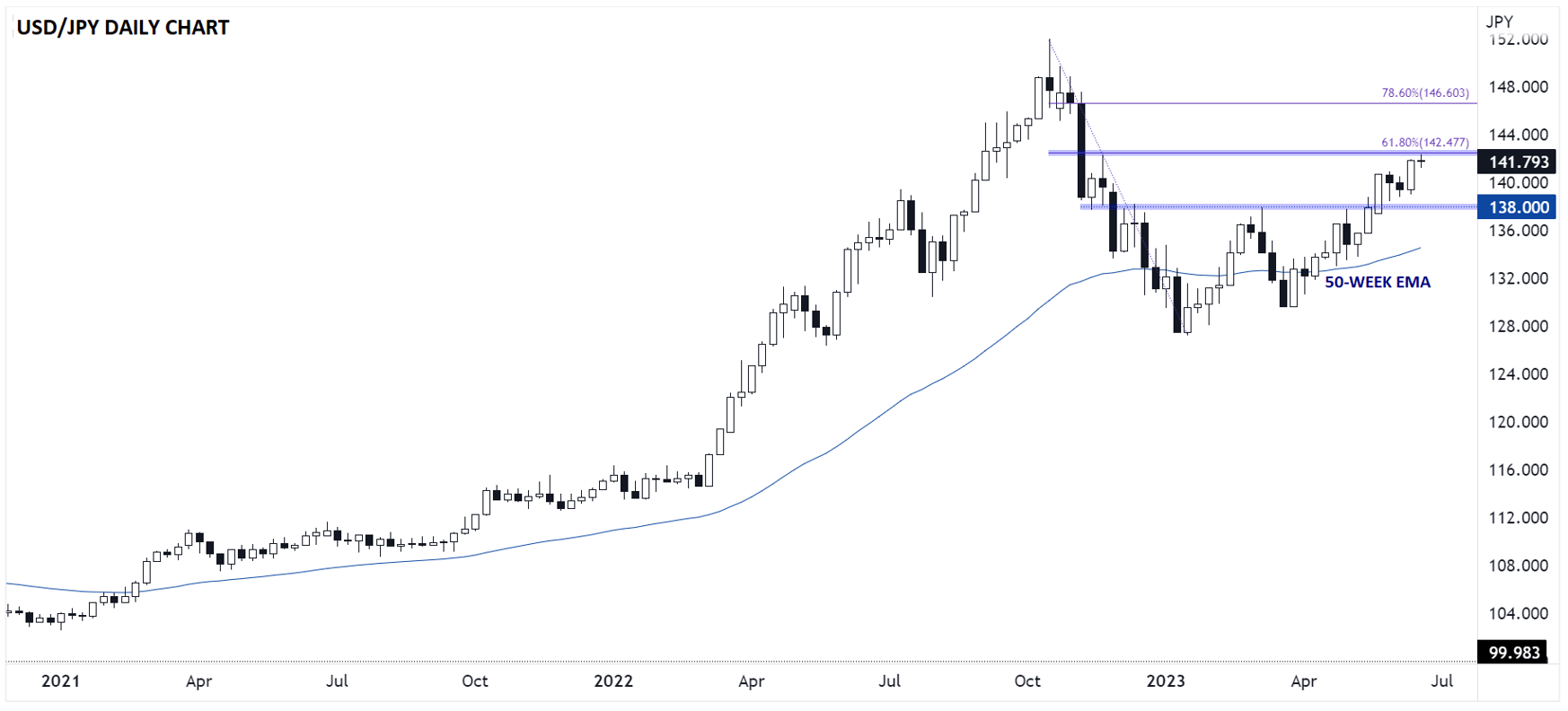

Japan is an island unto itself from a geographic perspective, but it’s also on an island when it comes to monetary policy. Traders were hoping that the installation of a new BOJ Governor would lead to changes in the country’s moribund monetary policy, but so far, Kazuo Ueda has been hesitant to make any tweaks, and indeed endorsed an 18-month review of the central bank’s monetary policy framework, dashing hopes of any imminent shift. While it's likely that the BOJ will look to relax its yield curve control (YCC) program this year, perhaps as soon as July when it’s expected to revise its inflation forecasts, any outright changes to interest rates are likely a while off, potentially into 2024.

For that reason, the yen can be seen as the stable anchor around which other currencies swing as interest rate expectations fluctuate. Therefore, stronger-than-expected global growth in the second half of the year would likely see the yen continue to bring up the rear in terms of relative performance, whereas a global economic slowdown in H2 would likely boost Japan’s currency at the expense of its rivals.

Technically speaking, USD/JPY is testing resistance at the 61.8% Fibonacci retracement of its 2022-2023 pullback at 142.50 as we go to press. A reversal of this barrier would hint at a bearish retracement back to previous-resistance-turned-support at 138.00 later this year, whereas a breakout could open the door for a bullish continuation toward at least the 78.6% Fibonacci retracement at 146.60 next.

Source: TradingView, StoneX

With leading indicators pointing to a slowdown in the global economy as we move through the final six months of the year, the odds favour a potential reversal in the performance of the first half of the year’s “high fliers,” the British Pound and euro, and a potential recovery in the yen after an abysmal start to the year.

That said, traders could have forecast the same thing in the first half of the year, so it will ultimately come down to the performance of the underlying economies in question. Uncertainty abounds, so it's more important than ever to follow the latest economic data and price action to trade successfully in the second half of 2023.

Written by Matt Weller, Global Head of Research

Follow Matt on Twitter @MWellerFX