What is uranium?

Uranium is a dense radioactive metal that is predominantly used to power nuclear reactors used to generate electricity. However, it is also used to create nuclear weapons and isotopes used in medical and industrial applications.

The metal is abundant in the Earth’s crust and is more common than other well-known metals including tin, tungsten, molybdenum, silver, gold and platinum. Uraninite is the most common primary uranium mineral, but coffinite and brannerite are others that yield some economic interest.

A short history of uranium and nuclear markets

Nuclear energy has come a long way since it was first used to generate power back in 1951, when it powered just four lightbulbs. Today, it is used to create over 10% of the world’s electricity.

The industry has had major ups and downs. The world’s electricity use doubled between 1990 and 2011 and nuclear power formed a large part of that, rising over 25% over those 21 years. However, the disastrous meltdown at the Fukushima nuclear power plant in Japan in 2011, caused by the site being hit by a tsunami, soured sentiment, knocked confidence and resulted in a number of countries reducing their nuclear energy output or even banning it altogether. That built on the existing negative image of nuclear power associated with other meltdowns, such as Chernobyl in 1986, or its use when catastrophic bombs were dropped on Hiroshima and Nagasaki during World War II.

In fact, it took at least seven years for the industry to recover, with nuclear reactors generating more of the world’s electricity in 2018 than it did before the meltdown in 2011. Japan, arguably the country with the most strained relationship with nuclear power, halted all its reactors following Fukushima but has been gradually bringing its plants back online over the years.

The steady improvement means the total amount of nuclear capacity generating electricity hit all-time highs in 2020, as countries start re-evaluating its advantages as a way of adding large swathes of power capacity without having to rely on dirtier fossil fuels. Although nuclear has long been regarded as a clean energy source that sits closer to renewables than fossil fuels, the risks associated with reactors has dampened its appeal – until now. With countries racing to decarbonise their economies and meet climate change pledges, nuclear is now starting to be embraced once again all around the world as a clean energy source, particularly as forecasts suggest we will need considerably more electricity over the coming decades as populations grow and we adopt more tech – from electric vehicles to IoT devices.

Read more: The complete guide to buying and selling ESG company stocks

Where is uranium produced?

Although abundant in the Earth’s crust, uranium production is highly concentrated. For example, Kazakhstan produces over 40% of the world’s uranium each year, with Africa accounting for around 16%, Canada 13%, and Australia 12%.

Its not just concentrated in terms of geography either, with 94% of global uranium output coming from just 14 companies, according to the World Nuclear Association:

|

Company |

2019 Production (tU) |

% of World Total |

|

Kazatomprom |

13,291 |

25% |

|

Orano |

5,809 |

11% |

|

Cameco |

4,754 |

9% |

|

Uranium One |

4,624 |

9% |

|

CNNC |

3,961 |

7% |

|

CGN |

3,871 |

7% |

|

BHP Group |

3,364 |

6% |

|

ARMZ Uranium |

2,904 |

5% |

|

Navoi Mining |

2,404 |

4% |

|

Energy Asia |

2,122 |

4% |

|

General Atomics/Quasar Res |

1,764 |

3% |

|

Sopamin |

1,032 |

2% |

|

Rio Tinto |

1,016 |

2% |

|

VostGok |

801 |

1% |

|

Other |

3,001 |

6% |

And, taking one step further, over half (56%) of global uranium production comes from just 10 mines:

|

Mine |

Country |

Main Owner |

2019 Production (tU) |

% of World Output |

|

Cigar Lake |

Canada |

Cameco/Orano |

6924 |

13% |

|

Husab |

Namibia |

Swakop Uranium (CGN) |

3400 |

6% |

|

Olympic Dam |

Australia |

BHP Group |

3364 |

6% |

|

Muyunkum & Tortkuduk |

Kazakhstan |

Orano/Kazatomprom |

3252 |

6% |

|

Inkai (Sites 1-3) |

Kazakhstan |

Kazatomprom/Cameco |

3209 |

6% |

|

Budenovskoye |

Kazakhstan |

Uranium One/Kazatomprom |

2600 |

5% |

|

Rossing |

Namibia |

Rio Tinto |

2076 |

4% |

|

Somair |

Niger |

Orano/Kazatomprom |

1912 |

4% |

|

Central Mynkudbuk |

Kazakhstan |

Kazatomprom/Cameco |

1694 |

3% |

|

South Inkai (Block 4) |

Kazakhstan |

Uranium One/Kazatomprom |

1601 |

3% |

What countries use nuclear power?

Nuclear power has traditionally involved major, long-term investment by both the private and public sectors. For example, over the last four decades, the average time it has taken to build a new nuclear power plant has ranged from 58 to 120 months – or, in other words, up to a decade. This is a long-term commitment, meaning that many countries simply idled capacity rather than tear it down even when the industry suffered image issues following Fukushima. Much of that idled capacity has been brought back online over the years and more electricity was generated by nuclear power in 2020 than ever before. There were 441 operable plants spread out across 30 countries at the end of 2020, as demonstrated by the table below.

|

Country |

Nuclear Capacity (MWe) |

Share of Electricity Generation in 2019 |

|

US |

96,772 |

20% |

|

France |

62,250 |

71% |

|

China |

45,498 |

5% |

|

Japan |

31,679 |

8% |

|

Russia |

29,203 |

20% |

|

South Korea |

23,231 |

26% |

|

Canada |

13,553 |

15% |

|

Ukraine |

13,107 |

54% |

|

Germany |

8,052 |

12% |

|

UK |

8,883 |

16% |

|

Sweden |

7,738 |

34% |

|

Spain |

7,121 |

21% |

|

India |

6,255 |

3% |

|

Belgium |

5,930 |

48% |

|

Czech Republic |

3,932 |

35% |

|

Switzerland |

2,960 |

24% |

|

Finland |

2,764 |

35% |

|

Bulgaria |

1,926 |

38% |

|

Brazil |

1,884 |

3% |

|

Hungary |

1,902 |

49% |

|

South Africa |

1,830 |

7% |

|

Slovakia |

1,816 |

54% |

|

Argentina |

1,641 |

6% |

|

Mexico |

1,600 |

5% |

|

Pakistan |

1,355 |

7% |

|

Romania |

1,310 |

19% |

|

Iran |

915 |

2% |

|

Slovenia |

696 |

37% |

|

Netherlands |

485 |

3% |

|

Armenia |

375 |

28% |

|

Total |

390,382 |

10.2% |

What is the uranium price?

Uranium, as a highly controlled substance, is one of only a handful of commodities that does not trade on an open market. Instead, transactions are conducted privately. There are two uranium prices – the spot price, representing how much it would cost to purchase right now, and a long-term price that represents the price paid for delivery over a longer period of time in the future.

Understanding the relationship between these two prices is key. For example, when spot prices are on the rise, companies tend to opt for the long-term in order to try to lock-in prices over a prolonged period of time to shield themselves from being hit by increasing spot prices. But, when the opposite occurs, they are more willing to gamble on falling spot prices. This also means that dramatic movements in the spot price can take time to feed through to the long-term price.

It is also important to note that the nuclear industry has been seen as more and more expensive as other alternatives have fallen in price, partly thanks to heavy government subsidies. With nuclear plants typically working with fixed costs over long periods of time, the dramatic falls in renewable energy and floods of cheap natural gas has made nuclear energy uncompetitive in recent years – although the surge in energy costs in 2021 means this is changing and actually highlighting the benefits nuclear can offer by having more stable energy prices over the long-term.

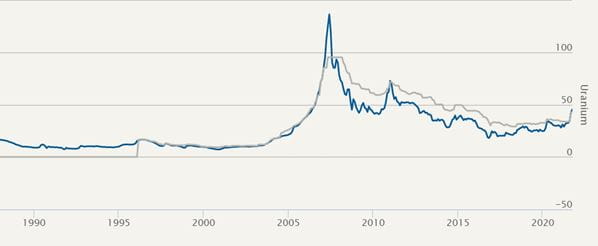

Below is a chart outlining the spot uranium price (blue) and the long-term price (grey) in US dollars per pound between the start of 1988 to the end of October 2021. We can see that prices spiked to all-time highs in 2007 before starting to taper off, and then suffering a lengthier decline following Fukushima in 2011, partly because Kazakhstan started to flood the market with supply even as demand became depressed. More recently, we have seen prices rise since the start of 2021 to their highest level since 2012.

(Source: Cameco)

Is nuclear power set to make a comeback?

So, why are uranium prices finally on the rise after suffering almost a decade of declines? Put simply, it is a combination of rising demand for nuclear power and a deficit in supply of uranium. Falling prices over the years has seen many companies temporarily or even permanently shut uneconomic mines and it takes time for higher prices to build enough confidence for firms to restart operations. The result of all this is that 30% less uranium was produced in 2020 than what the world’s nuclear fleet needed. Although the industry has been able to pull on military and government stockpiles over the years, these are dwindling.

‘Irrespective of the uranium supply scenario, the capacity of all presently-known mining projects will have to at least double by the end of [2040],’ says the World Nuclear Association.

This means that not only do existing mines need to ramp-up output, but there is also a big enough deficit that new mines will need to be created. Considering it can take up to a decade to establish a new large mining project, the lag could create an even tighter supply scenario over the coming years and lead to higher prices.

On the demand side, we are seeing encouraging signs from around the world that it is once again looking to embrace nuclear power as a key weapon in the fight against climate change. For example, the new $1 trillion US infrastructure bill that was recently passed has committed billions toward propping up the country’s existing nuclear fleet.

‘The bottom line is that you’ve got a lot of safe and reliable plants out there that are providing zero-carbon electricity exactly when our nation and the world need it most,’ said the deputy chief of staff at the US Department of Energy, Jeremiah Baumann. ‘We can’t afford to have the setback of losing a lot of carbon-free electricity.’

Meanwhile, the UK government has agreed to pump hundreds of millions of pounds into new mini reactors, with business secretary Kwasi Kwarteng describing it as a ‘once in a lifetime opportunity for the UK to deploy more low-carbon energy than ever before and ensure greater energy independence’.

Elsewhere, we are seeing some countries start work on their first nuclear reactors. Belarus hooked up its first plant in 2020, the United Arab Emirates started generating power from its first nuclear reactor in 2021, Bangladesh is currently constructing its first two sites, and Turkey is set to begin construction on its first plant this year. There are over 50 new plants currently under construction around the world, and over 69% are being built in Asia (particularly in China), where many countries are looking for ways to significantly increase electricity generation capacity and cut their carbon emissions.

Read more: Top renewable energy stocks to watch

Uranium trading: How to trade uranium

Uranium’s radioactive elements means it is not traded on the open market like most other commodities, such as oil, gas, coal or gold. This means traders cannot directly trade uranium and must gain exposure through alternatives, such as uranium miners that produce the commodity, nuclear stocks that use it, or even exchange-traded funds (ETFs). We outline some of the stocks and ETFs to consider below.

Read more: CFD trading for beginnersYou can trade all of the uranium and nuclear stocks mentioned in this article with City Index in just four easy steps:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the stock or ETF you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Top uranium stocks

Uranium miners are responsible for mining the commodity used to keep nuclear power plants in operation. They ultimately derive their value from how much they produce and the reserves they own that can be mined in the future – which in turn is valued based on spot and future uranium prices.

Below is a list of seven of the larger uranium miners on the market, but there are also a number of smaller companies that may be of interest such as Berkeley Energia and Forum Energy.

Kazatomprom

Kazatomprom is by far the largest producer of uranium in the world, operating five of the 10 largest uranium mines. The company is charged with being Kazakhstan’s national operator for the export and import of uranium, nuclear power plant fuel and the specialist equipment the industry needs. The National Wealth Fund Samruk-Kazyna JSC, which was formed by the Kazakhstan government, owns 75% of the business with the other 25% floated on the Astana International Exchange and the London Stock Exchange. The company operates 26 uranium deposits grouped into 14 project clusters spread across the country, but it also enriches it and produces the powders and fuel pellets used by nuclear power plants. It also mines a number of rare metals like tantalum, beryllium and niobium, which are all used to make key equipment used for a wide-range of high-spec applications.

Cameco

Cameco is headquartered in Canada but operates across North America, Australia and Kazakhstan. Its licenses allow it to produce around 53 million pounds of uranium each year, supported by proven and probable reserves of over 455 million pounds. It is also a leading provider of uranium refining, conversion and fuel manufacturing services. Notably, many of its North American operations remain suspended because they either prove uneconomical at current prices or because of a shortage of workers due to the pandemic – giving it plenty of firepower to trigger when market conditions improve.

BHP

BHP Group is one of the world’s largest mining companies that is known for producing a variety of commodities spanning copper, iron ore, nickel, and coal. However, it is also a sizeable producer of uranium. BHP operates one of the largest uranium mines in the world through Olympic Dam in South Australia, where it also produces the likes of copper, gold and silver. The main advantage BHP offers over pure-plays is that it is diversified and offers exposure to a number of commodities.

NexGen Energy

NexGen Energy is not yet producing uranium but is developing multiple projects in Canada. The company believes the bear market that has plagued the uranium market for over a decade has resulted in systemic underinvestment in the market at a time when demand is rising. It says 90% of all uranium is consumed by countries that have no production, especially in the US and in emerging markets such as China, India and Saudi Arabia. It says the lack of new supply twinned with growing demand will results in ‘sustainably high uranium prices’. Its key project is the Elite Arrow project in Saskatchewan, which is the largest development-stage uranium deposit in Canada.

Paladin Energy

Paladin Energy is an Australian-listed focused on the Langer Heinrich mine in Namibia, which is complimented by earlier-stage exploration work in Australia and Canada. The mine has historically produced over 40 million pounds of uranium in its lifetime but was idled back in 2018 due to low prices making it uneconomical. However, with prices improving, the firm is now working on restarting the operation under a new plan that could see it produce for at least 17 more years and produce up to 6 million pounds of uranium within the first seven years alone. Its plan suggests the mine can deliver an estimated life of mine cost of production of around $27.40 per pound of uranium, implying it can be highly profitable even at current prices.

Top uranium ETFs

ETFs are an effective and less risky way of gaining exposure to the uranium and nuclear markets as they offer broad exposure to a variety of companies operating within the sector, meaning you can spread the risk and avoid having to place all your eggs in one basket.

Northshore Global Uranium ETF

The Northshore Global Uranium ETF is made up of a basket of companies that are involved with uranium. This includes those exploring or mining for uranium as well as those that earn royalties from the commodity. The ETF’s market price has risen at a slower rate than its net asset value over the last year, meaning it has consistently traded at a slight discount.

Its 10 largest holdings at November 18, 2021 were Kazatomprom (17.2% of portfolio), Cameco (16.7%), Sprott Physical Uranium Trust (7.6%), Energy Fuels (5.8%), Yellow Cake (5.5%), Denison Mines (5%), Uranium Energy (5%), Paladin Energy (4.4%), NexGen Energy (4.3%) and CGN Mining Co (3.4%).

Global X Uranium ETF

The Global X Uranium ETF offers targeted exposure to companies that mine uranium or produce nuclear components, making it slightly different to the Northshore ETF even if they offer exposure to many of the same businesses.

The ETF’s top 10 largest holdings as of November 19, 2021, were Cameco (23.4%), Kazaktomprom (10.7%), NexGen Energy (7.2%), Paladin Energy (6.4%), Denison Mines (5%), Energy Fuels (4.5%), Uranium Energy Corp (3.5%), Yellow Cake (2.7%), Centrus Energy-A (2.5%) and Boss Energy (1.9%).

Top nuclear stocks

The other side of the coin to the uranium industry is the nuclear market that consumes the commodity to provide power from plants. It is a very different market to those mining uranium. Most of them are concentrating on keeping existing plants running while others are actively building new plants to add fresh capacity. It is worth noting that nuclear power plants tend to operate under long-term contracts with fixed prices, while new ones have historically been costly and time-consuming to build and therefore carry a significant element of risk.

EDF Energy

EDF Energy touts itself as one of the largest and cleanest energy companies across Europe. Over three-quarters of all the electricity it produces comes from nuclear power plants, with the rest predominantly coming from renewables with a small portion generated using coal and gas. It is 83.8%-owned by the government of France, which is more reliant than any other country in the world by generating over 70% of its electricity from nuclear plants. EDF is the ‘world’s leading nuclear operator’ and operates 73 reactors around the world, 58 of which are in France. It is also constructing major new plants in France as well as the UK and China.

Hitachi and General Electric

Two major conglomerates, Japan’s Hitachi and US outfit General Electric, are working together on their nuclear ambitions through a joint venture named GE Hitachi Nuclear Energy that was established in 2007. This is owned 80.01% by Hitachi and 19.99% by GE. The venture is based in the US and combines GE’s ability to design reactors, fuels and services with Hitachi’s construction capabilities and experience in improving performances of reactors. The venture currently offers the BWRX-300 small modular reactor, the sodium cooled PRISM reactor that can turn nuclear waste into low carbon energy, and the Advanced Boiling Water Reactor (ABWR) and Economic Boiling Water Reactor (ESBWR), which are described as the ‘world’s safest reactors’. It also offers a number of fuels and services to customers around the globe. It is important to remember that both Hitachi and GE have sprawling business empires and that nuclear energy forms only one component. This means they offer greater diversity but are not suitable for those seeking a pure nuclear play.

Rolls Royce

Rolls Royce is best known for producing engines and related equipment used in commercial and military airplanes, but it makes over 22% of its revenue from the energy markets, predominantly by supplying reciprocating engines and power generation systems that are used to provide critical backup power for mission critical systems like hospitals, as well as key marine and industrial applications. Although the company has disposed of some of its nuclear interests, it has hit headlines recently with a new technology focused on Small Modular Reactors (SMR). These are new, smaller reactors that can built in a factory rather than on-site, making them cheaper and quicker to construct than a typical large plant. The modular approach also means they can be scaled appropriately as needed. The firm has partnered with BNF Resources and Exelon to invest £195 million over three years into SMRs in the UK, with a further £210 million of investment coming from the UK government. They will require more funding, but the government backing sets a bullish tone for nuclear energy in the country, with the first plants set to be hooked-up to the power grid in the early 2030s. One plant will be the same size as around two football pitches and able to power around one million homes.

Exelon

Exelon is one of the largest power companies in the US (and also operates in Canada) operating nuclear, gas, wind, solar and hydroelectric power projects and distributing it across most of the country. Nuclear accounts for 61% of its energy mix, followed by natural gas (21%), gas and oil (6%), hydroelectric (5%), and wind and solar (3%). With 21 nuclear reactors at 12 facilities across the US, it is the country’s largest nuclear power generator. In total, it supplies energy to over 20 million homes and businesses and Exelon says its fleet is ‘more than four times cleaner than our nearest industry peer’.

Dominion

Dominion Energy supplies power and gas to almost 7 million customers across 16 US states from its offshore wind and solar projects and four nuclear plants named Millstone, North Anna, Surry and VC Summer. It also owns coal and oil facilities as well as a number of natural gas operations. Nuclear currently accounts for around 40% of its electricity generation but this is set to fall to around 34% by 2035 as it expands its renewables portfolio.

Kansai Electric

Japanese outfit Kansai Electric Power Co is another business with a sprawling empire spread across telecoms, real estate, and energy generation, transmission and distribution. Energy is the main business and the company generates around 12% of its power from three nuclear plants in Japan, although multiple units have been closed down in recent years in the wake of the Fukushima accident that prompted stricter rules being introduced for other plants across the country.

Fortum

Fortum is the third largest nuclear generator in Europe. It has nuclear plants in Finland and Sweden that are the second biggest contributors to energy generation, accounting for about 20%, with hydropower touting the biggest capacity. It also has combined heat and power, wind and solar projects on its books. Fortum is also one of the world’s largest companies handling nuclear waste and it also provides whole-of-life services to other companies operating plants. Like Rolls Royce, it too sees the future as small modular reactors but has said it could be 10 to 15 years before its first one is deployed.

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Shares market articles

November 2, 2023 01:41 PM

November 1, 2023 01:33 PM

October 31, 2023 01:15 PM

October 31, 2023 10:24 AM