US futures

Dow futures -0.34% at 38860

S&P futures -0.18% at 5111

Nasdaq futures -0.64% at 18120

In Europe

FTSE +0.03% at 7640

Dax 0.08% at 17703

- Stocks look to extend yesterday’s losses

- Atlanta Fed President Bostic sees no urgency to cut rates

- Tesla slumps on weak China EV deliveries

- Oil falls after China fails to impress

Sentiment softens ahead of key events

U.S. stocks are heading for a lower open, extending losses from the previous session, amid uncertainty over the future path for interest rates, which has seen stocks move away from record highs.

The leading indices closed lower on Monday despite the S&P 500 briefly touching an intraday record high thanks to the rally in chip stocks and AI hype, although the momentum faded by the end of the session.

Sentiment has soured after Atlanta Fed president Raphael Bostic said there is no urgency to cut interest rates given the US economy's strength. He believes that a rate cut could be appropriate in the third quarter but could be followed by a pause to assess how the policy shift is affecting the economy.

Attention is now on ISM services PMI data, which is expected to ease slightly to 53 from 53.7. Given that services inflation is proving to be sticky, the data and the subcomponents will be closely watched. The prices subcomponent rose sharply in January.

The figures come ahead of Federal Reserve chair Powell's testimony before Congress on Wednesday and Thursday, where he could maintain a hawkish tilt and reiterate his stance that the central bank needs more convincing that inflation will ease to the 2% target.

Even so, the market remains convinced that the Federal Reserve will begin cutting interest rates in June.

Following Powell's testimony, the focus will be on Friday's nonfarm payroll report for further clues on the resilience of the US labor market.

Corporate news

Tesla is set to open lower after the EV maker said shipments of its China-made cars had dropped to a 14-month low. Deliveries of EVs made in Tesla's Shanghai plant declined by 19% yearly to 60,365.

Target is rising after posting earnings that beat expectations. The retailer posted EPS of $2.98 versus $2.42 expected on revenue of $31.92 billion versus $31.93 expected. However, the retailer warned that it expects another year of weak sales.

Crypto stocks remain in focus as bitcoin's insatiable rally continues and the price clears $68,000 just shy of the record hit in the peak bull run of 2021.

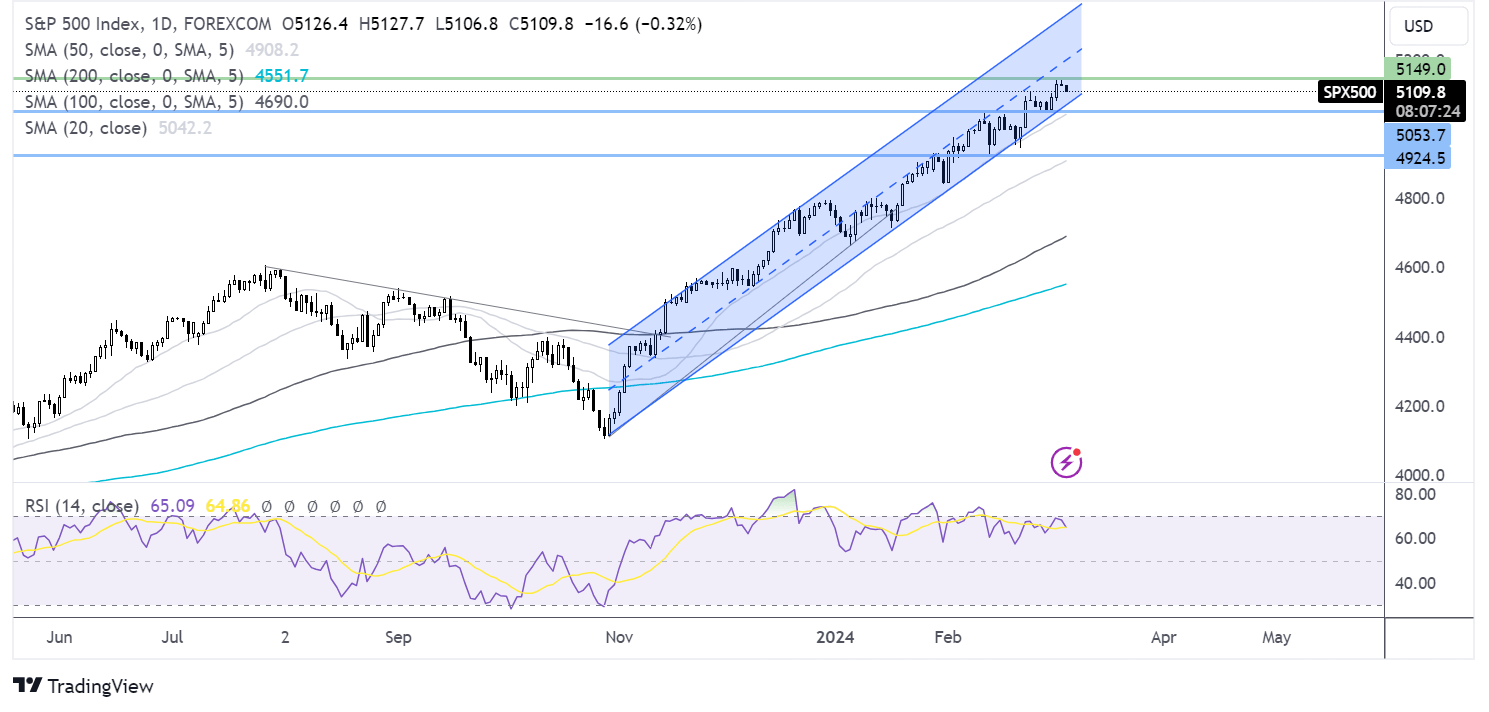

S&P500 forecast – technical analysis.

S&P500 continues to trade in a rising channel, although it appears to be running out of steam after hitting 5149 yesterday. The price has just eased lower toward 5100. Support from the lower band of the rising channel is at 5070, and 5050 marks last week’s low. Meanwhile, buyers will look to take out 5150 to push to fresh all time highs.

FX markets – USD rises, EUR/USD falls

The U.S. dollar is slightly stronger ahead of more U.S. economic data and after a hawkish comment from federal official Bostic, who sees no urgency in cutting interest rates,

EUR/USD is falling despite an upward revision to the eurozone services PMI to 50.2, up from 50, marking a 7-month high. While growth is fractional here, there's also been an uptick in staff recruitment by service providers and stability in incoming new business. Operating costs rose to the highest level in 10 months, pushing up output price inflation. The data comes ahead of the ECB's interest rate decision on Thursday.

GBP/USD is inching lower after the UK services PMI was downwardly revised to 53.8 from 54.3. Adding to the gloomy news, UK sales growth in February slowed as lousy weather kept shoppers at home. According to the BRC, spending increased by 1.1% in February compared to a year earlier, down from 1.2% in January.

Oil falls after China fails to impress

Oil prices are falling for a second straight day. China’s growth forecasts failed to impress the market despite an oil cut extension from OPEC+.

China's annual economic growth target of around 5% is similar to last year's goal and in line with expectations. However, the lack of big stimulus plans to prop up the economy disappointed investors and raised concerns about the oil demand outlook for the world's largest oil importer.

Meanwhile, uncertainties surrounding interest rate cuts and questions over how aggressively central banks will be able to cut rates are also weighing on the demand outlook. Given the economy's resilience, the Federal Reserve appears in no rush to start cutting interest rates.

These factors offset news from the weekend that OPEC+ agreed to extend its voluntary cuts of 2.2 million barrels per day into the second quarter of this year.

Looking ahead, the US inventory report is expected to show that crude stockpiles increased by 2.6 million barrels last week.

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest US Open articles

Yesterday 01:32 PM

July 25, 2024 01:17 PM

July 24, 2024 01:43 PM

July 23, 2024 01:38 PM