The focus of OPEC+ members over the last few weeks has shifted from agreeing on cuts to more aggressively enforcing them, and so far Kazakhstan has shown more willingness than some of the other rule-breakers to comply. Although coronavirus is still raging across South America and some US states are going through a fresh spike in cases, the end of the lockdown is fundamentally spelling a recovery in demand that is likely to go on over the weeks ahead. The lower production and the pickup in demand are already being reflected in upticks in WTI and Brent crude prices and the week ahead should support the same trend.

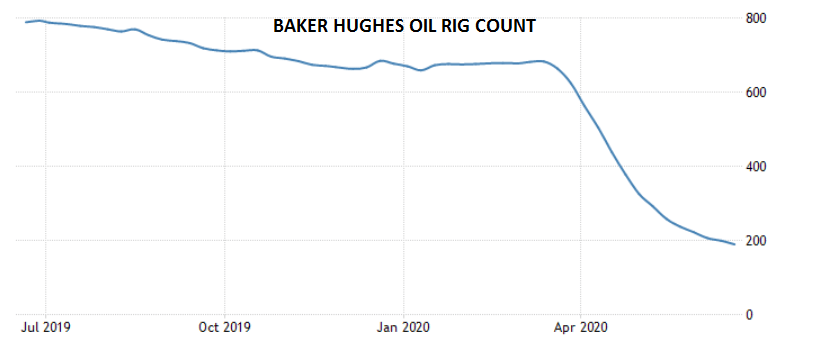

US rig count expected to turn

To say that the erosion of domestic US demand since the outbreak of COVID has been dramatic would be an understatement; it has pushed domestic shale production to breaking point. So many rigs have closed – 690 in the last 12 months – that with only 279 rigs left in operation, there is not much more to close. The rig count onshore has dropped below 200 for the first time last week and there are only 35 active shale oil rigs outside the Permian Basin of West Texas and Southeastern New Mexico.

Oil production is notoriously cyclical and also slightly lags behind price moves, as producers try and shelter their industry from knee-jerk reactions. Now that WTI prices have somewhat stabilised, surviving shale producers are increasingly saying that they have no more plans to shutter production and that at WTI prices above $30, they can weather the storm. Over the last few weeks the drop in rig counts has slowed down and with demand coming back, is due to correct in the opposite direction. The first in line for reopenings are larger producers in Texas, but more expensive shale basins in North Dakota and Oklahoma are also likely to start coming back on line.

Source: Trading Economics, Baker Hughes

COUNTRY FOCUS: Kazakhstan

During the recent OPEC+ spat over some members’ overproduction, Kazakhstan was singled out alongside Iraq, Angola, and Nigeria as one of the countries that has not been complying with production cut agreements. After subtle (and not-so-subtle) threats from Saudi Arabia, Kazakhstan has committed to cut output by 390,000bbl/day. Ironically, Saudi Arabia may not be Kazakhstan’s largest headache at present.

The outbreak of the coronavirus has threatened to shut down the country’s largest site, the Tengiz field, which is operated by a group led by Chevron, as 950 workers have tested positive. The outbreak in Tengiz made for nearly 13% of all the cases in the country in late May. The cheek-by-jowl nature of the job, the distant location, and the fact that workers not only work but also live in very close quarters makes it nearly impossible to do anything about social distancing and also explains why there have been similar outbreaks across oil fields in central Asia and Russia. For the moment the news flow from Kazakhstan has gone very quiet but it is possible that Kazakhstan’s willingness to comply with production cuts in June partially came about because the country’s hand was forced by the virus.

Separately, for the cuts to happen the government had to bring on board not only domestic producers but also foreign investors, as two of the country’s biggest producers, Tengiz and Kashagan, are operated by foreign consortia: the former by Chevron, ExxonMobil and Lukoil and the latter by local oil and gas producers and by Eni, ExxonMobil, Royal Dutch Shell and China’s CNPC. Now the country has issued individual quotes to oil producers asking them to cut output by around 22%.

In April Kazakhstan produced 31.3 million tonnes of oil and gas condensate, of which 10.2 million tonnes were from Tengiz, 5.8 million tonnes in Kashagan, and 4.2 million tonnes in Karachaganak.

|

When |

What |

Why is it important |

|

Tue 23 June 08.30 |

German June manufacturing PMI |

German manufacturing is slowly clawing its way back out of a decline but is unlikely to have gone back to expansion. PMI expected at 46, still indicating a contraction |

|

Tue 23 June 09.00 |

Eurozone June manufacturing PMI |

The recovery of manufacturing in Eurozone as a whole is proceeding at a slower pace than Germany’s as some member states are worse hit by COVID lockdowns. Expected at 43.8 |

|

Tue 23 June 14.45 |

US June manufacturing PMI |

Expect a pickup from May but manufacturing still not on an even keel. Forecast at 44.0 |

|

Tue 23 June 21.30 |

API weekly crude oil stocks |

Crux time for US oil stocks. The numbers should start declining, if not, it would indicate that the pickup in demand is much slower than expected. |

|

Wed 24 June 15.30 |

EIA crude oil stock change |

Last week stock still surprisingly went up by 1.21m bbl. |

|

Thu 25 June |

China Dragon Boat Festival |

Chinese markets closed for 2-day holiday |

|

Thu 25 June 13.30 |

US initial jobless claims |

This week’s increase in claims was higher than expected showing that the job market is struggling to restore itself despite the reopening. A pickup in the number of cases across Southern States is likely to keep numbers high. |

|

Thu 25 June 13.30 |

US Q1 GDP data |

Expected at -5% |

|

Fri 26 June |

China Dragon Boat Festival |

Domestic markets closed |

|

Fri 26 June 18.00 |

Baker Hughes US rig count |

After weeks of declines the rig count should start stabilizing or picking up |

|

Fri 26 June 21.30 |

CFTC oil net positions |

Money managers’ open oil positions |

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Oil articles

July 24, 2024 09:55 AM

July 21, 2024 01:00 PM

July 19, 2024 01:23 PM

July 18, 2024 01:12 PM