Headline risks from the Middle East could direct sentiment

We head into this coming week with the potential for Middle East headlines to dominate sentiment. Reports of Iranian missiles striking a location in Iran of Friday saw oil and gold prices spike, safe-haven flows move into the Swiss franc and indices fall alongside the Australian dollar. Sure, AUD/USD rebounded recouped all of its losses once it was confirmed that the missile strike had not hit a nuclear facility, but it serves as a clear reminder that markets can move quickly during bouts of risk off, and usually driven by panic as the worst is assumed until told otherwise. Therefore, headline risks should be at the front of every traders mind this week.

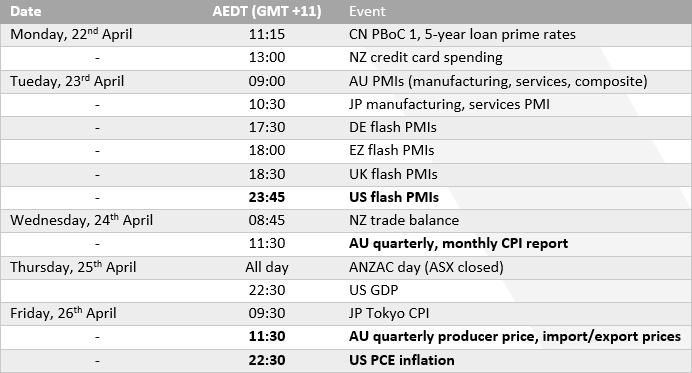

Flash PMIs

As for data, flash PMIs will provide a forward look at growth expectations for global regions, Australia included. Unless of course geopolitical tensions rise – in which case economic data will be quickly ignored. But if sentiment allow, traders will look for any signs of growth or inflationary pressures in the PMI reports. Traders can pair the respective regions against respective currency pairs and look for divergences between the reports. For example, stronger-than-expected PMIs from Australia and weaker-than-expected from Europe could weigh further on EUR/AUD given ECB members are becoming increasingly vocal about a June cut.

Australian CPI, PPI

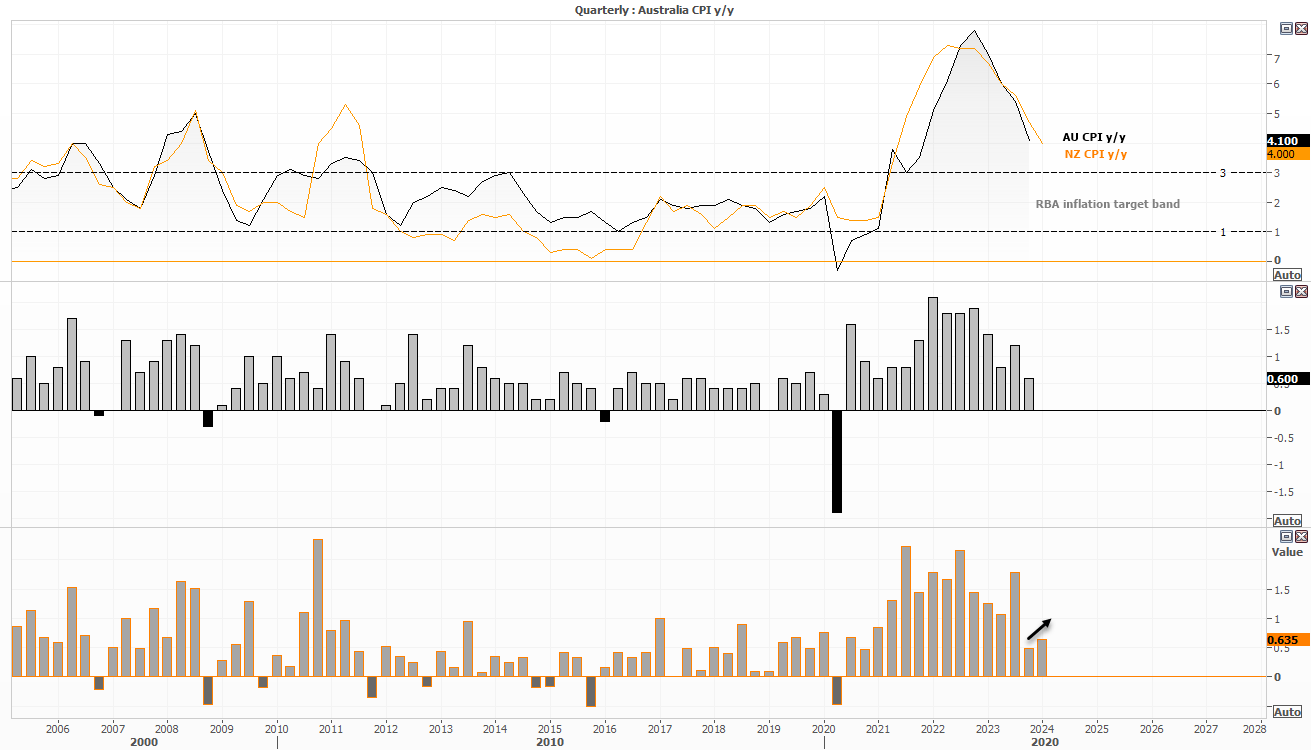

Wednesday’s inflation report will garner a lot of attention from the RBA and traders in general, as it is the quarterly release which tends to carry more weight then the monthly equivalent. We saw last week that New Zealand’s inflation levels remained elevated at 4% y/y and 0.6% q/q and given that Australia’s quarterly CPI tends to trend in the same direction than its Kiwi trade partner than it may be a reasonable to not expect miracles from Australia’s report.

Q3 saw CPI at 4.1% y/y and 0.63% q/q, and unless we see a noteworthy drop with these figures next week then the RBA are likely to continue referring to inflation as “too high” in the upcoming meetings. Furthermore, there’s very little for doves to get excited about in Australia’s latest jobs figures. Jobs are still being added and 3.8% unemployment remains low by historical standards and remains a key reason as to why expect the RBA to remain at a cash rate of 4.35% for much (if not all) of 2024.

For context, Bloomberg is pricing in just a 7% chance of 21bp of cuts this year.

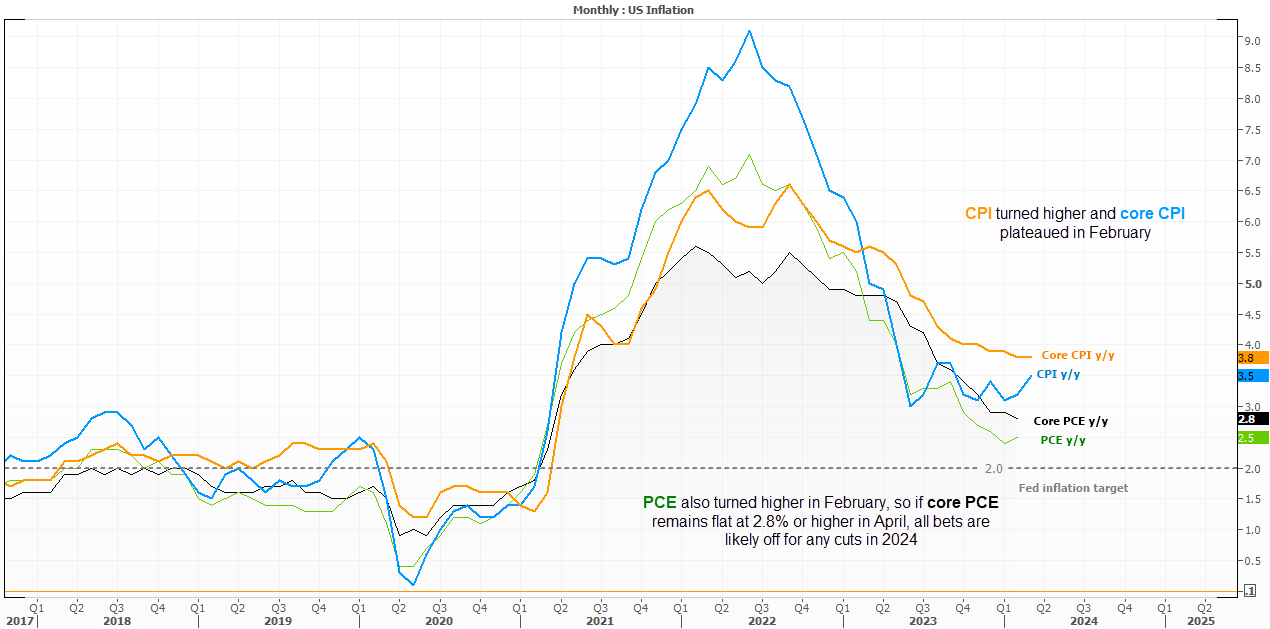

US PCE inflation

With Fed members including Jerome Powell himself aggressively pushing back on rate cuts, it would take quite the soft inflation report next week for markets to regain confidence of even a single cut this year. And as PCE inflation tends to not be volatile (and headline CPI was hotter than expected) then I see little chance of a soft PCE report next week. Whether this results in a stronger US dollar and yields (to the detriment of AUD/USD) remains debatable, as the US dollar and yields were actually lower following hawkish comments from Powell. One theory is that if the Fed are perceived to be taking inflation more seriously with higher for longer rates, bond investors are stepping back into the market on the bet inflation will come down in future (and weighing on yields, and therefore the US dollar now). We’ll simply have to assess how markets respond next week to confirm this theory.

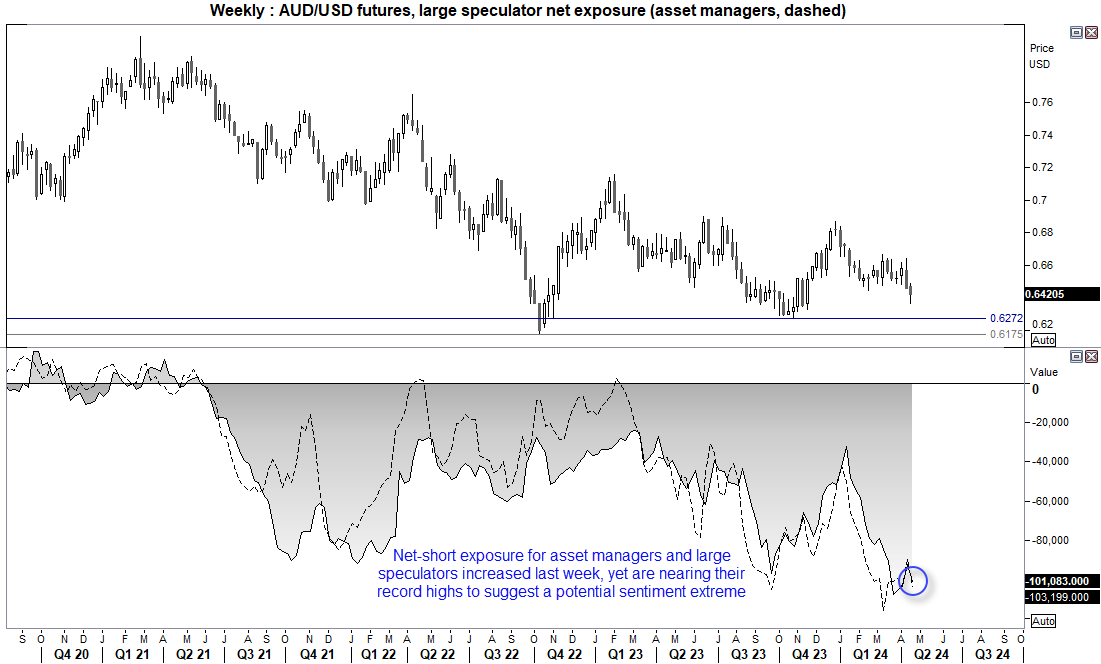

AUD/USD futures – market positioning from the COT report:

- Net-short exposure to AUD/USD futures rose $0.35 billion for the week, as of last Tuesday

- Large speculators increased net-short exposure at the fastest weekly pace in 14 years

- Net-short exposure among large speculators and asset managers rose by 8.7k and 13.3k contracts respectively

- However, net-short exposure for both sets of traders are nearing their record high set in March, which leaves the potential for a sentiment and extreme (and bullish reversal)

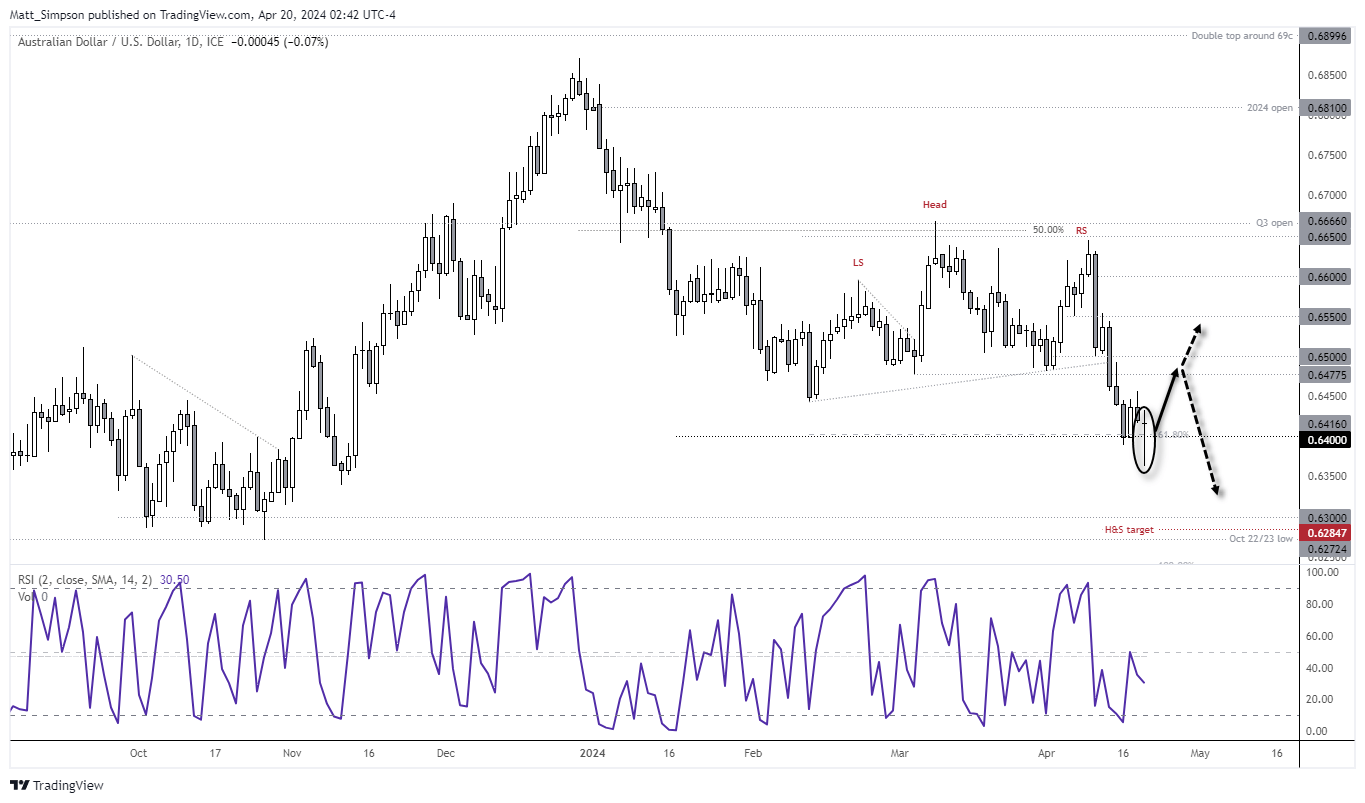

AUD/USD technical analysis

The Australian dollar reached the 64c downside target, and even briefly traded beneath it on Friday. Yet reports that Iran did not intend to retaliate against Israel helped markets reverse their earlier risk-off moves and send AUD/USD back above 64c by Friday’s close. Assuming there are no further surprises from the Middle East, the bias is for AUD/USD to build on its false break lower and head for at least 0.6450 in the first half of the week, with the potential for a move towards 0.6500. Beyond that it becomes murky – and likely down to the US PCE inflation report as to whether AUD/USD can truly rally. At this stage, my assumption is for a limited bounce and a potential swing higher to form next week.

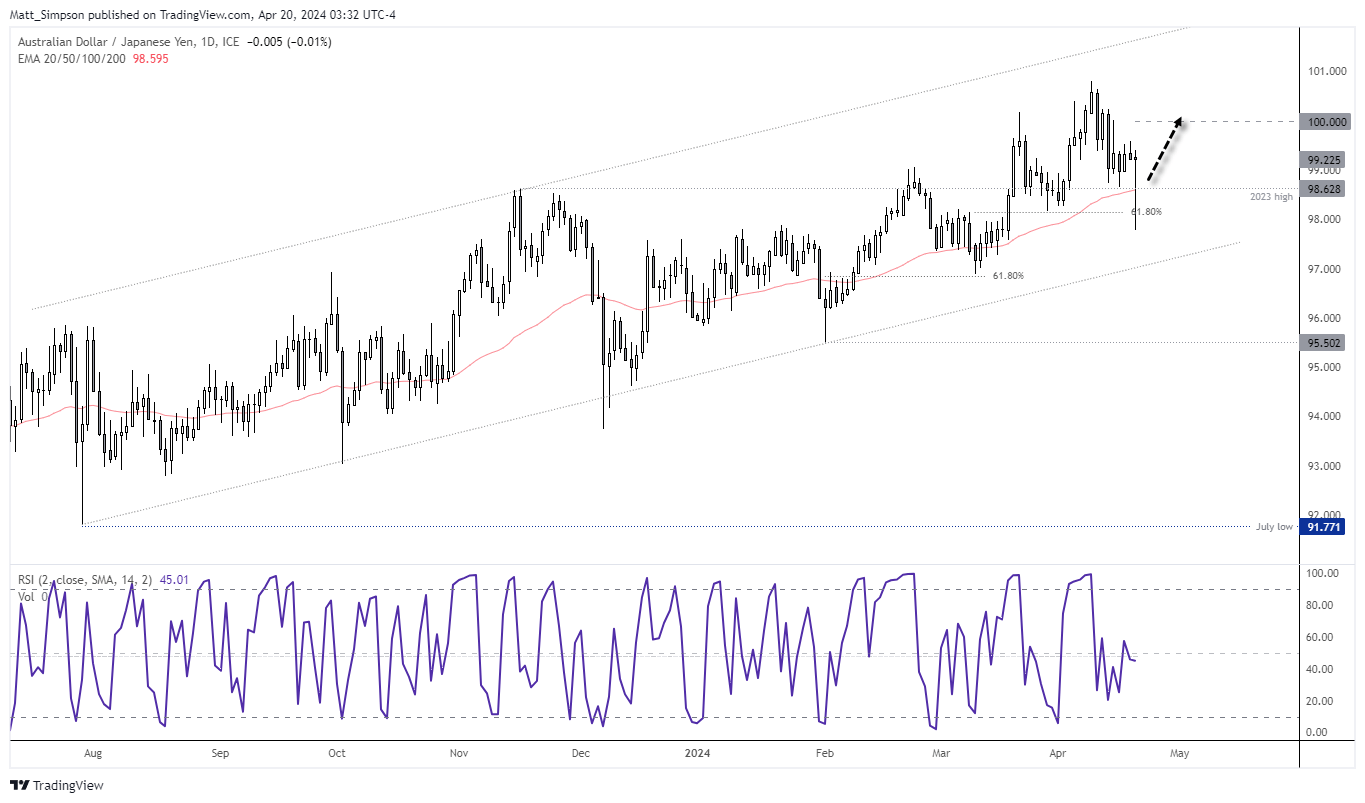

AUD/JPY technical analysis:

An elongated bullish pinbar formed on Friday due to Middle East headlines (as AUD/JPY is a classic barometer of risk for FX, it was the most volatile AUD pair of the day). Yet notice how the 50-day EMA sits perfectly near the 98.63 support level, so any pullback towards it early this week could be tempting for bulls to seek dips – assuming there are no gaps lower on Monday or sentiment-ruining headlines incoming. 100 marks available initial target for bulls, a break above which likely requires a fresh bout of risk on (which seems debatable for now).

-- Written by Matt Simpson

Follow Matt on Twitter @cLeverEdge

How to trade with City Index

You can trade with City Index by following these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the market you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest AUD/USD Weekly Outlook articles

July 21, 2024 06:00 PM

July 14, 2024 06:00 PM

July 7, 2024 08:00 PM

June 30, 2024 08:00 PM