Q2 2024 USD/JPY Outlook: Downside delayed but still forecast

USD/JPY Key Points

- USD/JPY downside yet to materialise despite narrowing interest rate differentials

- Buoyant risk appetite contributing to Japanese yen weakness

- USD/JPY faces key moment as it threatens to break to multi-decade highs

- Upside limited on BOJ intervention threat and weakening fundamentals, but downside capped unless the global economy rolls over

USD/JPY remains in much the same position as when our 2024 outlook was released three months ago, levitating near multi-decade highs as rampant investor risk appetite and vastly different monetary policy settings relative encourage traders to continuing buying the dip.

It looks set to remain that way until we see a significant narrowing in interest rate differentials or major turbulence in financial markets that may disrupt the carry trade, encouraging investors to repatriate capital back to Japan.

Neither screen as probable in the short-to-medium term. But nor are the tailwinds that helped propel USD/JPY to these levels likely to remain this strong, pointing to a similar outlook to what conveyed in early January: medium-term risks are skewed to the downside. However, near-term, a break to multi-decade highs may be in the cards.

We’ll look at the key drivers of the USD/JPY exchange rate in this report, evaluating what’s important and what’s not, along with the underlying message coming from fundamentals and technicals.

Rate differentials now working against USD strength

Make no mistake. When it comes to the main driver of the USD/JPY exchange rate, it’s interest rate differentials. Capital typically moves to areas that offer the best returns, especially when you’re talking about risk-free US Treasuries issued in US dollars. With the Federal Reserve continuing to adopt vastly different monetary policy settings relative to the Bank of Japan, the yield advantage the US commands over Japan remains historically elevated across numerous timeframes. That’s despite the Fed flagging it’s likely to begin cutting interest rates shortly just as the BOJ delivered its first rate hike in 17 years.

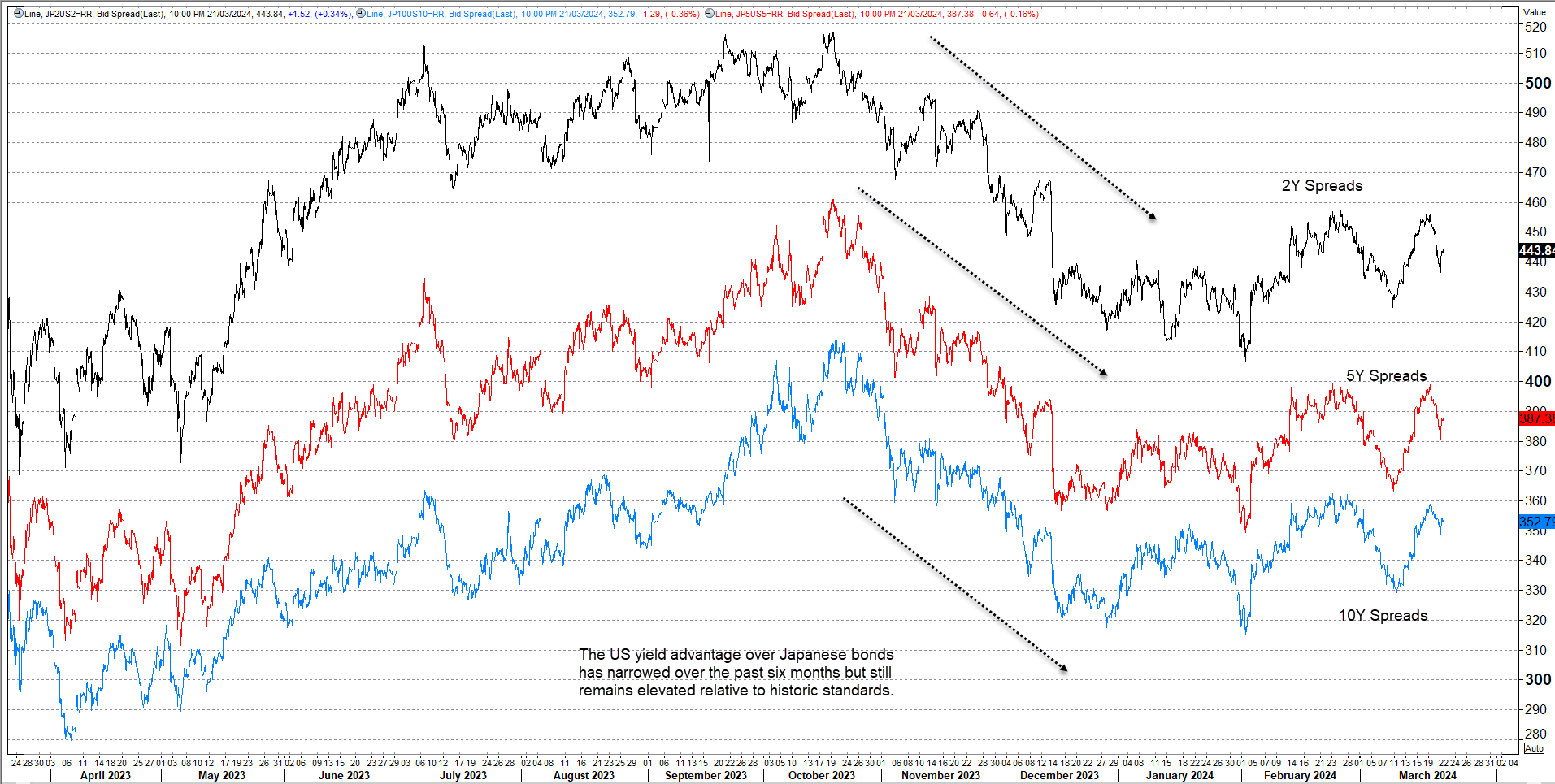

This chart shows the differential between US bond yields and Japanese bond yields over a two, five and 10-year timeframe. Even though the “spread” between the two has compressed from the levels seen in the September, the US still offers significantly greater relative returns on a pure yield basis. However, the narrowing is a less powerful tailwind for US dollar strength, contributing to downside risks.

Source: Refinitiv

But they remain the key driver for USD/JPY

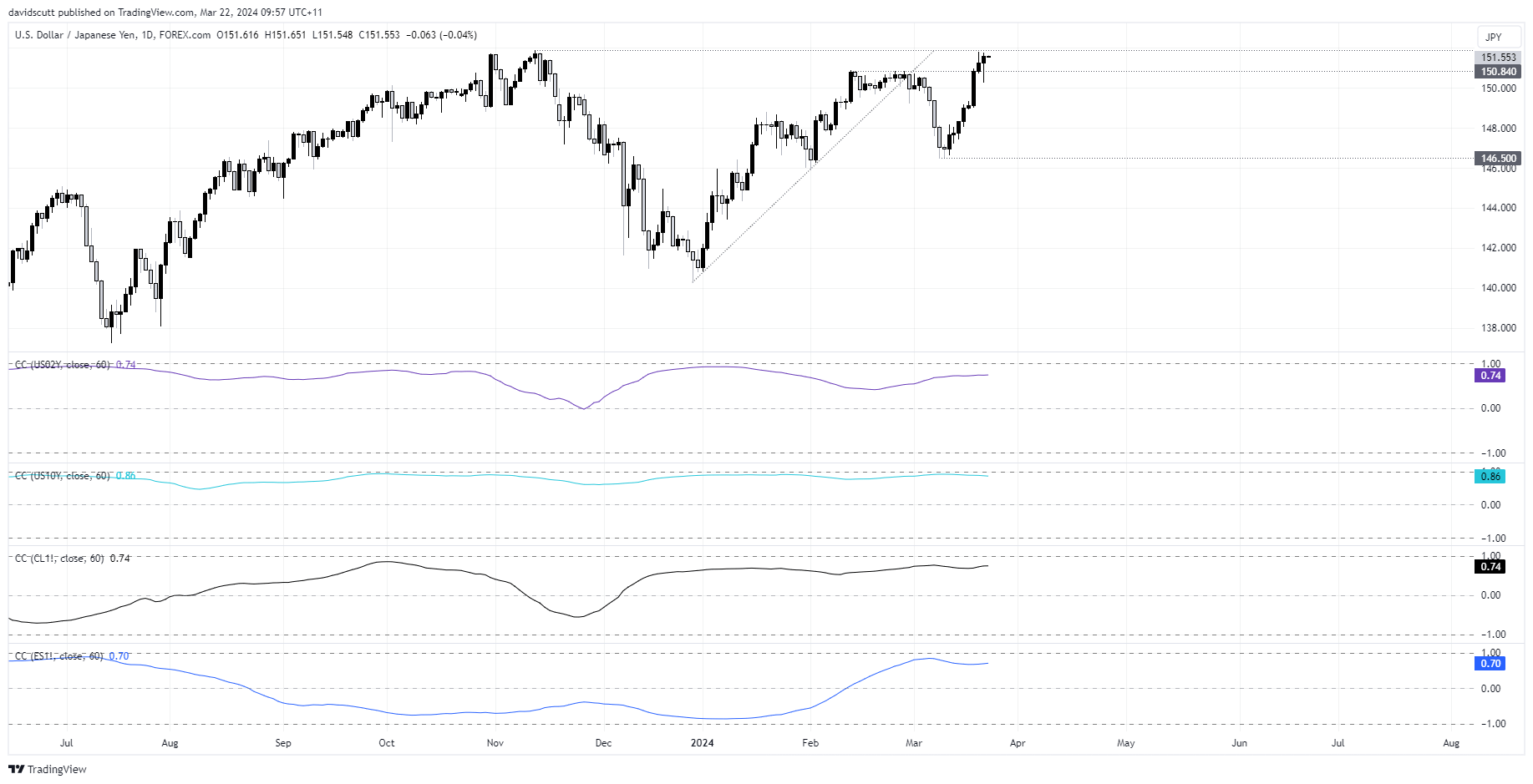

This next chart looks at the rolling quarterly correlation USD/JPY has with multiple market indicators using a daily timeframe.

At 0.86, USD/JPY had a strong positive relationship with US 10-year bond yields over the past quarter, meaning they frequently moved in the same direction. The relationship wasn’t quite as strong with US 2-year bond yields, indicating relative central bank interest rate expectations are not as influential as they were when the 2024 outlook was published.

However, while USD/JPY often moved in the same direction as US yields, it didn’t fall anywhere near as much as spreads would suggest, continuing to knock on the door of multi-decade highs.

These factors may explain why.

Oil rebound positive for USD, negative for JPY

With the US a major oil exporter and Japan a large oil importer, it comes as no surprise that USD/JPY also has a relatively strong positive correlation with crude oil futures at 0.74. The US benefits from higher prices while Japan does not, and vice versus. So, the rebound in crude prices bolstered the USD over the past quarter.

Conditions are ideal for JPY carry trades

But it’s the last correlation that may explain why USD/JPY is levitating above 150. It tracks movements in USD/JPY against US S&P 500 futures, a proxy we’ve used to reflect investor risk appetite. While the two had the weakest relationship over the quarter at 0.70, it’s the recent strengthening that’s interesting.

With stocks rallying, volatility low and major central banks signaling looming policy easing, carry trades swapping low-yielding Japanese yen into higher-yielding currencies would likely be flourishing, exporting Japanese capital around the world.

That may explain the reason why USD/JPY downside has yet to materialise. Narrowing yield differentials are being offset by buoyant risk appetite and crude prices.

BOJ should be a secondary consideration

While the Bank of Japan has provided plenty of headlines recently after ditching negative interest rates and yield curve control, the brutal honest assessment is the JPY side of the USD/JPY equation is nowhere near as important as the USD side.

This next chart explains why.

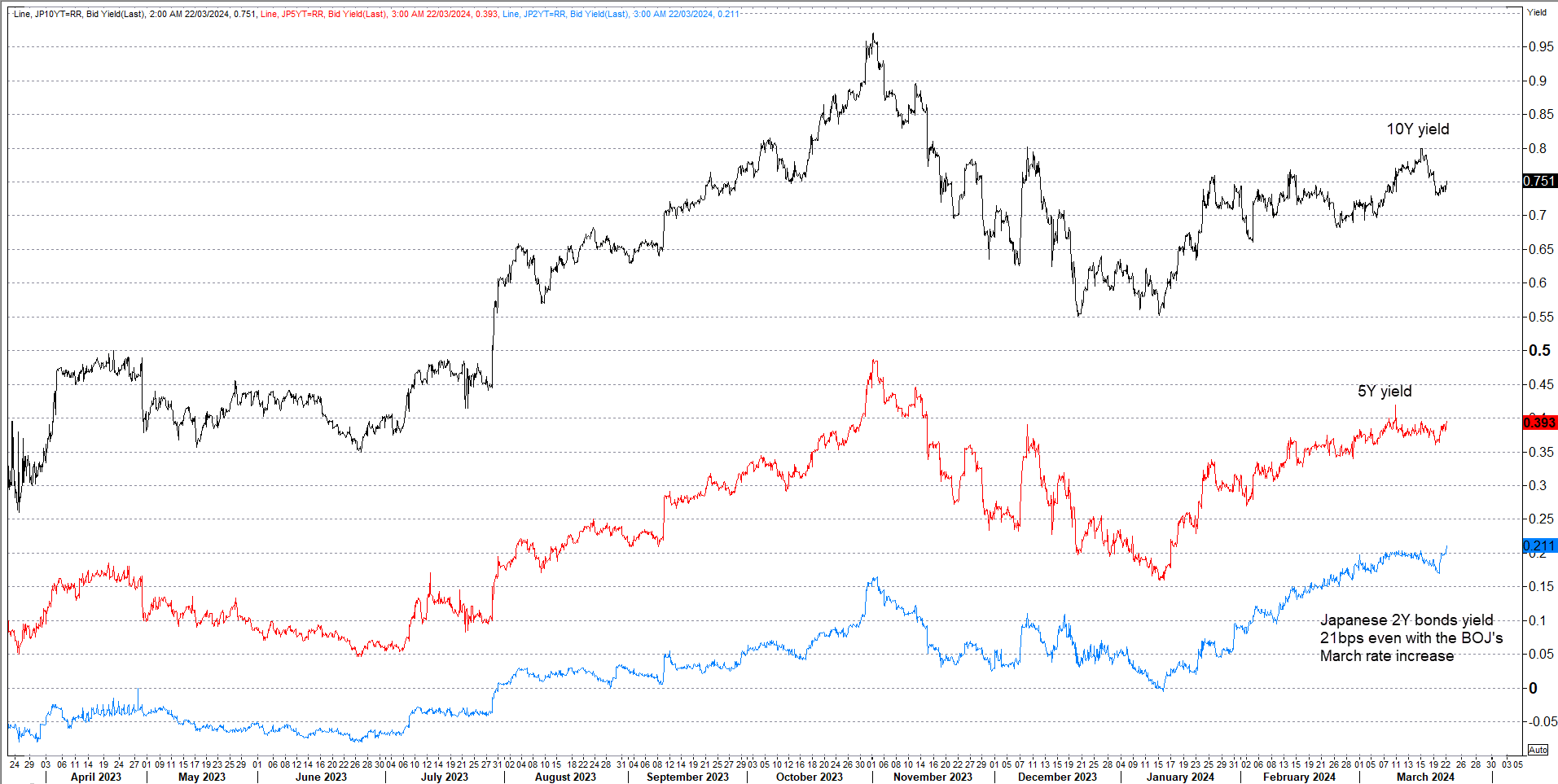

Going back to the first chart tracking yield differentials, spreads between two and 10-years ranged between 352 basis points to 444 basis points. Huge. Then consider Japanese bonds yield 20, 39 and 74 basis points for two, five and 10-years respectively.

When yield differentials are measured in the hundreds of basis points, and they’re the main driver of USD/JPY, it’s obvious that if there’s to be any significant shift in spreads and exchange rate it will driven by the US.

Assessing the BOJ intervention threat

Barely a day passes now without a Japanese official warning that speculative FX moves that don’t reflect fundamentals are undesirable, keeping the threat of market intervention from the BOJ at play. But if you asked the same officials in private if they really want a stronger yen, it’s debatable if they would say yes.

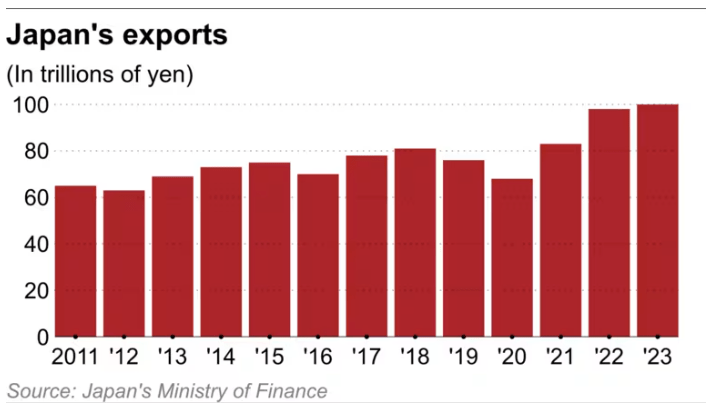

Japan’s external sector has been firing on all cylinders thanks to the weaker currency, helping to boost export revenues and volumes, keeping the flagging domestic economy afloat. For policymakers seeking to create a virtuous cycle of higher inflation leading to stronger wage demands, the weaker JPY is doing a fantastic job of importing inflation.

Source: Nikkei Asia

The BOJ may intervene should we see a dramatic and sustained weakening in the Japanese yen, but its impact would be negligible over the longer-term. USD/JPY trades where it does due to fundamentals, as much as officials don’t want to admit it.

Significant market volatility unlikely but a major downside risk

As discussed earlier, buoyant risk appetite has likely contributed to USD/JPY strength over the early parts of the year, meaning traders should be alert to the risk of the macro backdrop shifting dramatically.

Black swan events cannot be predicted, so ignore trying to preempt them. But grey swans do provide clues on what to keep an eye on. The obvious ones are an escalation in geopolitical tensions or a hard economic landing. Regarding the latter, with the most aggressive monetary policy tightening episode in modern times yet to fully impact activity, the risk remains.

However, central banks are moving to ease policy settings. Bond market volatility is falling, something that should improve economic certainty and benefit broader financial markets. That suggests hard landing risks are subsiding.

Another obvious risk would be if inflation fires up again forcing central banks to backtrack on rate cuts. This appears to be underpriced and would be worth monitoring given the impact on bond yields and carry trades.

USD/JPY technical outlook

At the time of writing, USD/JPY is just 30 pips away from its November 2023 high. For the purposes of this forecast, we’ll focus on the implications should it break or fail at this level.

Zooming out using a weekly timeframe, it shows USD/JPY is sitting in an ascending triangle pattern. Having set a string of higher lows, and with dips becoming increasingly shallow, there’s every chance USD/JPY may take out the level. Momentum is turning higher, as demonstrated by RSI breaking its downtrend. The ducks look to be lining up.

While convention suggests a break may lead to USD/JPY rising to above 180, such an outcome screens as unlikely. Looking out three months, potential upside would likely be capped around resistance at 160, and even that seems a stretch given the risk of BOJ intervention and compression in yield differentials. Between 152 and 160, there are no significant levels to speak of. While that suggests there’s ample room for an explosive move, having already struggled to crack these levels, a more likely scenario would be a slow grind higher, potentially to the mid-150s.

Alternatively, should resistance at 151.95 repel another advance, it will provide a powerful message to traders that there may be more success targeting downside rather than upside. However, unless there’s a dramatic shift in Fed pricing towards large scale rate cuts akin to late 2023, the proximity of long-term uptrend support points to limited downside this quarter, potentially the high 140s in the absence of a major trend break.

That’s not an immediate threat but one we expect will play out in the second half of 2024, regardless of whether 151.95 breaks or holds.