Crude oil drops to test key support

Crude oil has had a bit of stop-start to 2017 and both oil contracts are still down on a year-to-date basis after rising a good […]

Crude oil has had a bit of stop-start to 2017 and both oil contracts are still down on a year-to-date basis after rising a good […]

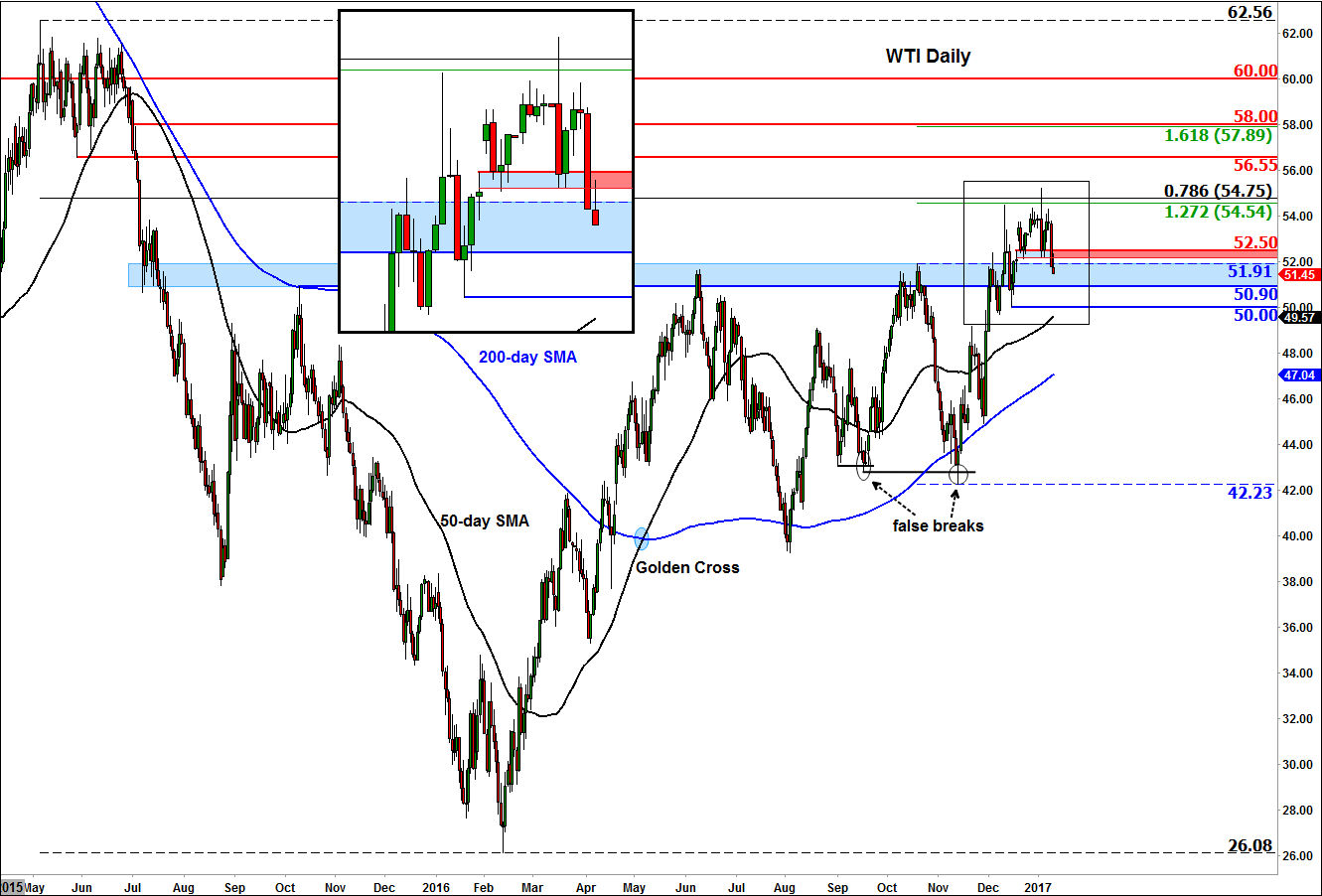

Crude oil has had a bit of stop-start to 2017 and both oil contracts are still down on a year-to-date basis after rising a good 45% last year. Fundamentally or indeed technically nothing has changed, however. I still think oil is heading much higher in the coming months and thus view the slight struggle here as a normal hesitation in what essentially is a rising market. The OPEC’s decision to reduce its oil output was a game changer, which will likely remain the number one driver behind oil prices in the months to come. The market is curious as to whether the cartel and those non-OPEC producers who took part in the deal will honour their agreement or whether cracks will start to appear. I would be very surprised if producer nations breached their agreed quotas by noticeable margins because while that might be profitable in the short-term, it could be very costly in the long-term. Why sell more oil for less when there is a chance to sell less oil for more in the future?

Some of the weakness in oil prices can be attributed to signs that US crude production is set to rise again. Already, the number of active rigs drilling for oil in the US has risen by the tenth consecutive week. In total, 529 oil rigs are now online, which is the highest since December 2015. It remains to be seen whether and by how much drilling activity will increase under the presidency of Donald Trump, who has promised to streamline permits to drill on federal land. This is a factor that could limit oil price gains this year. Even so, the OPEC’s decision to reduce its oil production should continue to help drive prices towards $60-$70 a barrel.

Thanks to a brighter fundamental outlook, oil prices made significant technical breakthrough at the end of last year as they finally broke out of their consolidation ranges. However the follow-up technical buying pressure has been mild thus far. In fact, WTI finds itself back to the point of origin of the breakout around the $50.90-$51.90 range after the rally stalled on the first trading day of the year around a Fibonacci convergence area of $54.55-75. If WTI now breaks below the lower end of the 50.90-51.90 range (i.e. $50.90) this would significantly reduce its appeal for the bulls. In this potential scenario, I wouldn’t be surprised if WTI goes on to fall back below $50 again.