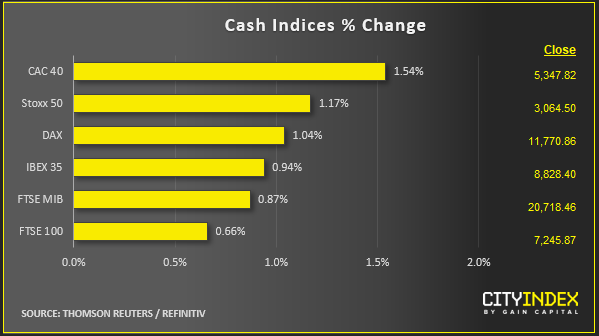

Stock market snapshot as of [8/8/2019 2:40 PM]

Global stock markets and macro

- On the surface, it looks like stock investors have just decided to ‘hold ‘em’ regardless of recent and persisting seismic risks, when the obvious rational choice might be ‘fold ‘em’ again, and run for the hills, just like earlier in the week

- But in the context of fresh instances of long-term government debt turning negative by yield and the latest U.S. term spread inversion—3-month bills to 10-year Treasurys—it is clear that positive stimuli for risk seeking that may have triggered the rallies are not its only underpinning

- Probabilities of a further 25 basis point cut in the Fed’s September meeting implied by Fed fund futures may have fallen from as much as 85%, though the current 76.5% is by no means abject pessimism

- Note a 29 basis-point 10-year Treasury yield slump this month, 34bp in New Zealand and 14bp in Germany, whilst the yen and Swiss franc safe-haven currencies outperform also belie the solidity of Thursday’s risk bounce in the first half of the global session

- The stronger-than-expected daily yuan fixing by the People’s Bank of China continues to echo, even though at 7.0039 yuan, it was still the weakest fix since 2008. The PBOC thereby maintains its stance of avoiding an all-out aggressive devaluation, whilst still responding to the Washington’s latest tariff salvo

- China trade data were not stellar, but a 3.3% annualised bounce in exports, is still expansion, even if imports fell 5.6%; a tick on ‘risk’ stimulus No. 2

- The outcome is a robust cross-asset risk rally (including in oil, with a little extra help from Saudi jawboning) that makes it into the second half of European trading

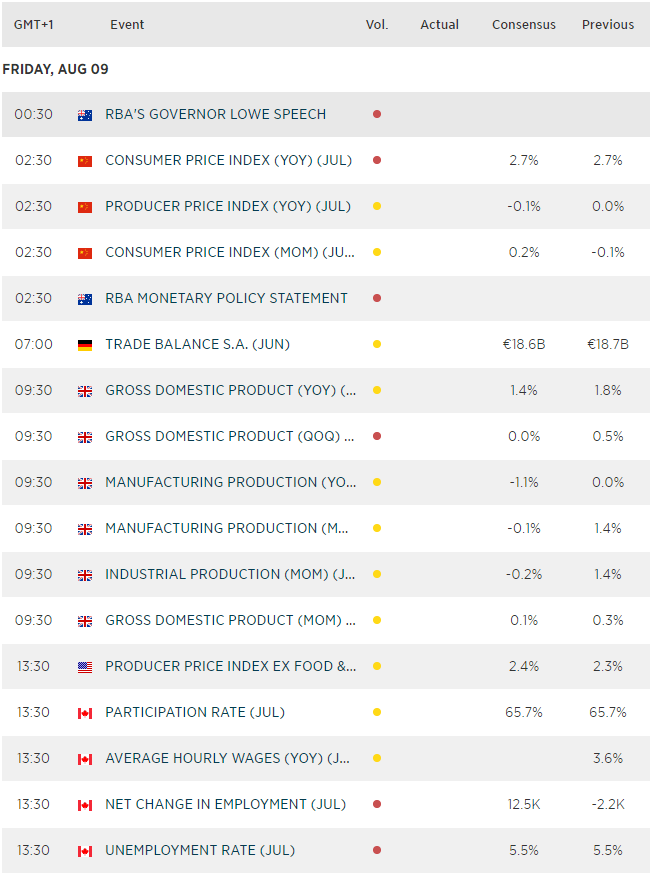

- A back-end loaded data calendar poses risks to the apparent return of optimism, founded on policy help. An RBA statement, a German trade update, UK GDP, factory, industrial and construction readings, as well as U.S. PPI, are all still to come on Friday. Not to mention that the most impactful source of market stimuli in the current period could tweet at any time

Stocks/sectors on the move

- Europe’s technology sectors are in the lead as STOXX’s hardware, software and chip sectors do what they usually do when U.S.-China trade optics appear to improve. The Automobiles & Parts index is among the consumer segments to advance, whilst Metals & Mining also strides ahead on the same motivation. It’s worth noting that this is a broad rally—including defensive industries, with the Utility index flat though Health Care and Consumer Staples are as much as 1%-1.6% higher

- A German focus for the big-cap movers included continuation of Europe’s lacklustre results season. Deutsche Telekom fell 1% after reporting in-line earnings but also fixed-line subscriber losses and slowing broadband growth. ThyssenKrupp gained 4% despite slashing its outlook and flagging persistently weak units. A plan to get shot of those businesses offset weak, albeit as-expected earnings. Lighting group Osram tumbled 7.2% after its biggest shareholder rejected a long-trailed €3.4bn private equity bid. Nokia shares continue their recovery from a weak year so far with more news reflecting the side-lining of erstwhile 5G leader Huawei. The Finnish group said it won its latest 5G network deal, this time from Vodafone New Zealand

- There’s a tech flavour for early big U.S. stock market movers too: Uber rose 5%, after noting its post-IPO lock-up period would be ending early. Not to be outdone, rival Lyft also volunteered to allow investors an early exit from lock-up terms following its own IPO. Uber reports earnings tonight. Lyft rose 7% in apparent recovery from an after-hours slump on disappointment over its results. Advanced Micro Devices also gained 7% after unveiling a ‘game-changing’ new server processor, according to analysts. Symantec surged 13% on takeover expectations. Roku extends its rally this year to 230% following results and a 17% surge

Upcoming corporate highlights

BMO: before market open AMC: after market close

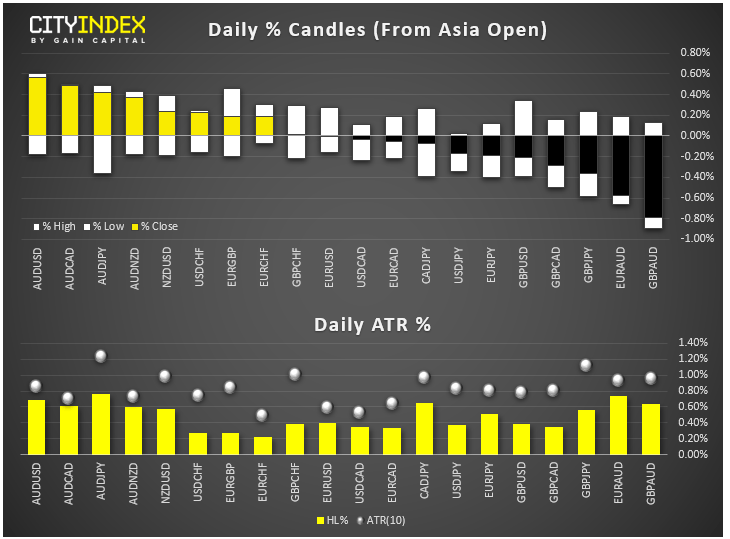

FX market snapshot as of [8/8/2019 2:42 PM]

FX markets and gold

- AUD is the strongest thanks to stronger-than-expected Chinese exports data and slight improvement in risk appetite following Monday's big stock market drop. EUR and GBP remain among the weakest

- CAD was supported by a sizeable rebound in the price of crude oil (although it was easing off its highs at the time of writing). Prices were also supported by short-covering following a 5% plunge the day before and slightly better sentiment towards risky assets across the board. In addition, the slump in prices have raised speculation that Saudi and her OPEC+ allies could take further action to support the oil market

- Thanks to the slight improvement in risk appetite, gold was easing back a day after it surged through $1500 for the first time in six years

Upcoming economic highlights

Latest market news

Today 07:57 AM

Today 03:18 AM

Yesterday 11:43 PM

Yesterday 11:05 PM

Yesterday 02:23 PM

Latest Crude Oil articles

Yesterday 12:04 PM

May 3, 2024 12:11 PM

May 2, 2024 01:18 PM

May 2, 2024 04:02 AM