Exxon tracks oil price relapse

The wheels have come off the U.S. energy sector rally.

The wheels have come off the U.S. energy sector rally.

The S&P 500′s volatile energy sector gained 24% in 2016 as the world’s biggest oil company Exxon, a clutch of other majors and scores of smaller energy names dragged themselves off the floor, a year and a half after one of the biggest oil price collapses for decades.

Currently contributing just 6.5% of the benchmark index’s total capitalisation ($1.4 trillion) down from almost 17% at the last energy ‘cycle peak’ in 2008, the industry still nevertheless packs a punch. That’s due to its volatility in recent years and because it is often front and centre in investor perceptions.

Exxon certainly exerts a real-terms drag on the sector. It is down 14.6% since hitting two-plus year highs last July and is the worst performer over 6 months amongst all but one (Hess) of its closest S&P 500 peers.

Exxon is certainly the heaviest weight contributing to the overall sector’s underperformance, leaving the S&P energy index down 5% since December 31st 2016.

That’s in step with a 4.9% slippage of Nymex crude oil futures, tracking the frustrating lack of significant inventory depletion (underscored by the EIA’s latest update on Wednesday). Data earlier this month and last pointing to dwindling demand in China, has also eroded bullish sentiment that followed OPEC’s supply agreement inked late last year.

At the end of last month, the group reported its lowest quarterly profits since 1999. True, BP, Shell and others followed soon after with their own negative milestones. However, almost every other major oil producer showed stronger underlying profitability, and crucially, with prices 50% higher in a year, faster production growth too. Exxon’s production fell 3% to 4.1 million barrels of oil equivalent per day.

A $2bn write down of the group’s natural gas reserves acquired with its huge buy of XTO Energy in 2009 also dragged profits. Investors are now wondering if, as seems the case with rivals like Shell and BP, Exxon has reached the end of a brutal phase of rationalisation.

Problem is, following an annual asset review, Exxon says it may have to reduce the value of some reserves in the U.S.’s Rocky Mountains too. New estimates are set to be released some time this month, though no precise date has been set.

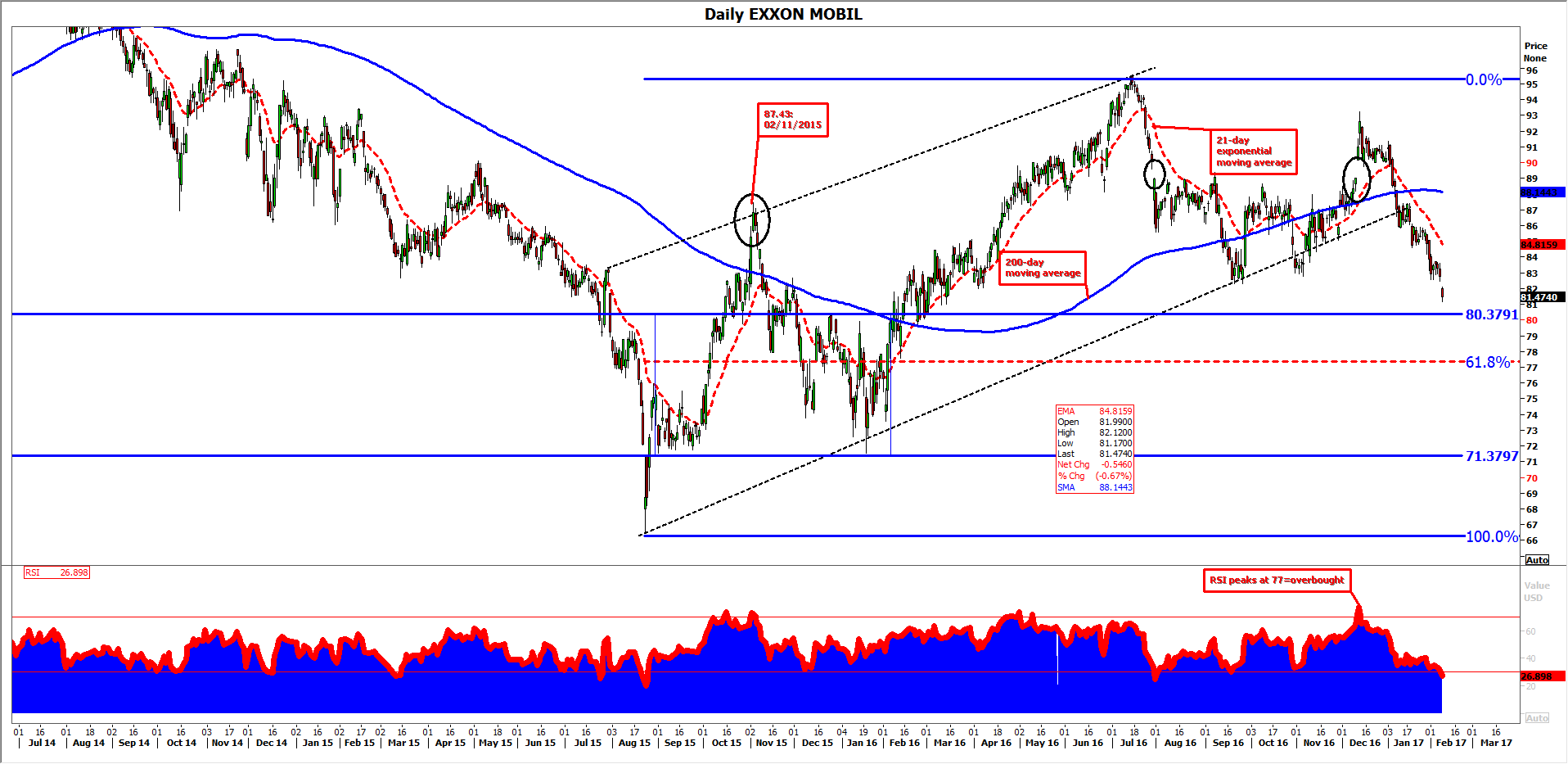

The promising albeit erratic rise off August 2015 lows signally ended when XOM broke down from its 1-year standard deviation channel in January.

It is now a question of how far the decline might extend. Indicators offer little solace. The 200-day moving average (MA, blue), is inverting lower, the 21-day exponential MA (red; dotted) is trailing the stock’s sharp decline and the finest measure, the Relative Strength Index is still consolidating from its most ‘overbought’ indications since 2011.

Given the erratic nature of the prior exhausted uptrend, little clear support is visible on the way down.

61.8% of the August 2015-July 2016 up move may come in as support, if reached at $77.

That marker is intercepted by a consolidation band (blue rectangle on the chart below) spanning from a low of $73.30 in September 2015 to highs near $80 in December of that year.

Source: Thomson Reuters, City Index / please click image to enlarge