The unpredictable HK backdrop keeps guidance static despite a promising first half

Burberry shares are justifiably pricing back in profit expectations that were trimmed on worries over Hong Kong unrest and China growth. Britain’s leading purveyor of finery comfortably matched first-half 2020 sales expectations whilst pacing revenue and earnings forecasts, as sales accelerated in recent months.

Key H1/Q2 results

- Comparable H1 retail sales +4%, in line with estimates

- Comparable Q2 retail sales, +5% vs. +4.6% est.

- H1 revenue: £1.281bn vs. £1.26bn est.

- Comparable H1 operating profit: £186m vs. £172.3m est.

(Note H1 op. profit was £202m under recently adopted IFRS accounting standard)

Solid results partly reflect delivery on the promise of debut collections by chief designer Riccardo Tisci. Any doubt that a strong initial reception would hold into later quarters ought to have been softened given double-digit growth based in new products. Robust figures and firm demand overall demonstrate that anticipated disruption from unrest in Hong Kong was contained though the extent of its impact was still sobering. Burberry shares initially surged 9% on Thursday, their best one day move in four months. But the revelation in a post-earnings presentation that retail sales fell 38% in Hong Kong trimmed the rise to as little as 3.5%. With further “significant negative impact” expected in over Q3, the risks to full-year forecasts—which Burberry has maintained—can’t be ignored.

What’s positive about the HK situation is that the group doesn’t foresee further impairment charges there, after booking a £14m H1 hit, without details. More broadly, other key regions gave no fresh cause for alarm. And whilst currency impact and advantages from the new accounting format gave a non-operational lift, resilient demand still underpinned underlying profits. As well, the efficiency programme is on track for annual £135m savings targeted by 2022 with £110m in costs also intact.

The final impression is that the firm played its latest challenging hand adroitly, whilst the trump card of exclusive and rarefied designs is working out better than planned. True, old inventory continues to weigh on margins. And the verdict on the strength of new high-margin items (e.g. handbags) needs to be withheld till availability of Tisci’s collections reaches 80% of the ‘mainline’ offer from 70% in Q2. The buzzy Tencent alliance is just as difficult to quantify, though nice to have. It will neither hinder nor help Burberry with key challenges in the months ahead.

The positive though volatile stock reaction reflects improved stability but also continued uncertainty that the luxury group can escape its minnow status and also-ran valuation relative to European rivals anytime soon.

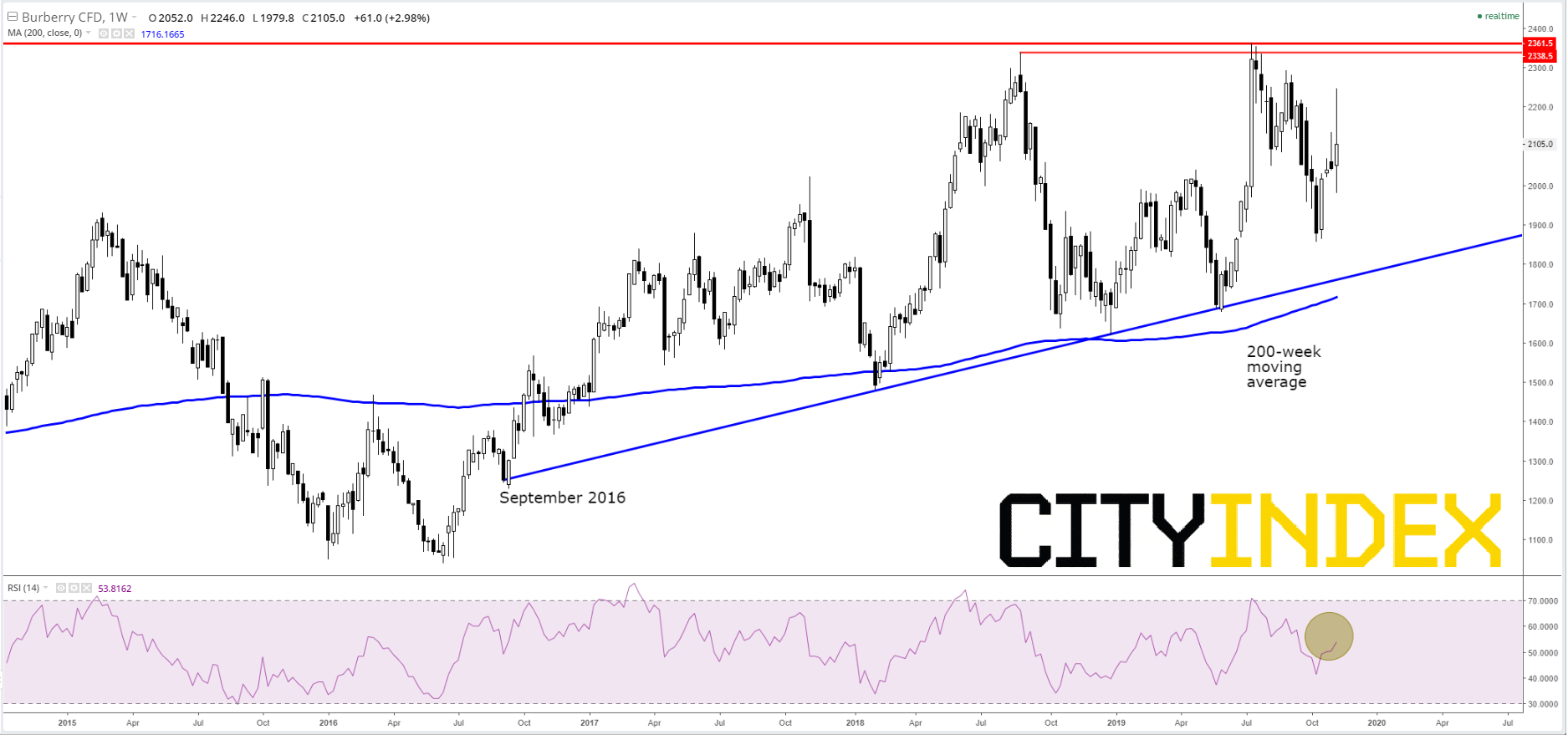

Chart points

Uptrend intact, the upside case continues to hinge on the difference between the cleanest trend of recent years, stemming from early September 2016, and peak resistance around 2340p-2360p. Investors must decide when or whether momentum will suffice on the share’s next attempt at the above highs, to surpass them. Sellers will have the opposite judgement to make. With the 200-week average now adding support to the dominant rising line, whilst RSI momentum also rallies with plenty of room to run, BRBY at least looks set to drift up towards another attempt at those highs as the year winds up.

Burberry Group Plc. CFD – Weekly

Source: City Index

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Shares market articles

November 2, 2023 01:41 PM

November 1, 2023 01:33 PM

October 31, 2023 01:15 PM

October 31, 2023 10:24 AM