Bullish factors

- FOMC's monetary policy decision should curb more optimistic bets on a Fed interest rate cut in the short term and contribute to a momentary dollar strengthening.

- COPOM is expected to cut the basic interest rate (SELIC) by 0.50 p.p. and indicate that it will maintain the pace of reductions in the next meetings, which should harm the attractiveness of Brazilian bonds and falter the real.

- November CPI in the US is expected to show a slight hike compared to October and signal that the path to price stability recovery may be a bit longer and more tortuous than anticipated, increasing risk aversion and weakening currencies of emerging countries.

- Monetary policy decisions in the eurozone and England should reinforce the economic weakness in Europe and contribute to weakening their currencies versus the USD, favoring the American currency by contrast.

Bearish factors

- The possibility of advancing important economic agendas for the government in the National Congress could reduce the perception of fiscal risks for Brazilian assets and strengthen the real.

Our Brazil team provides regular weekly coverage of the Brazilian economy and the outlook for the Real, accessible by clicking the link in the banner above.

The week in review

The week was marked by fluctuations in bets on the trajectory of interest rates in the US, which reflected the release of several indicators for the American job market. Additionally, data for the Brazilian Gross Domestic Product (GDP) for the third quarter and services in various economies strengthened the BRL and the USD during the week.

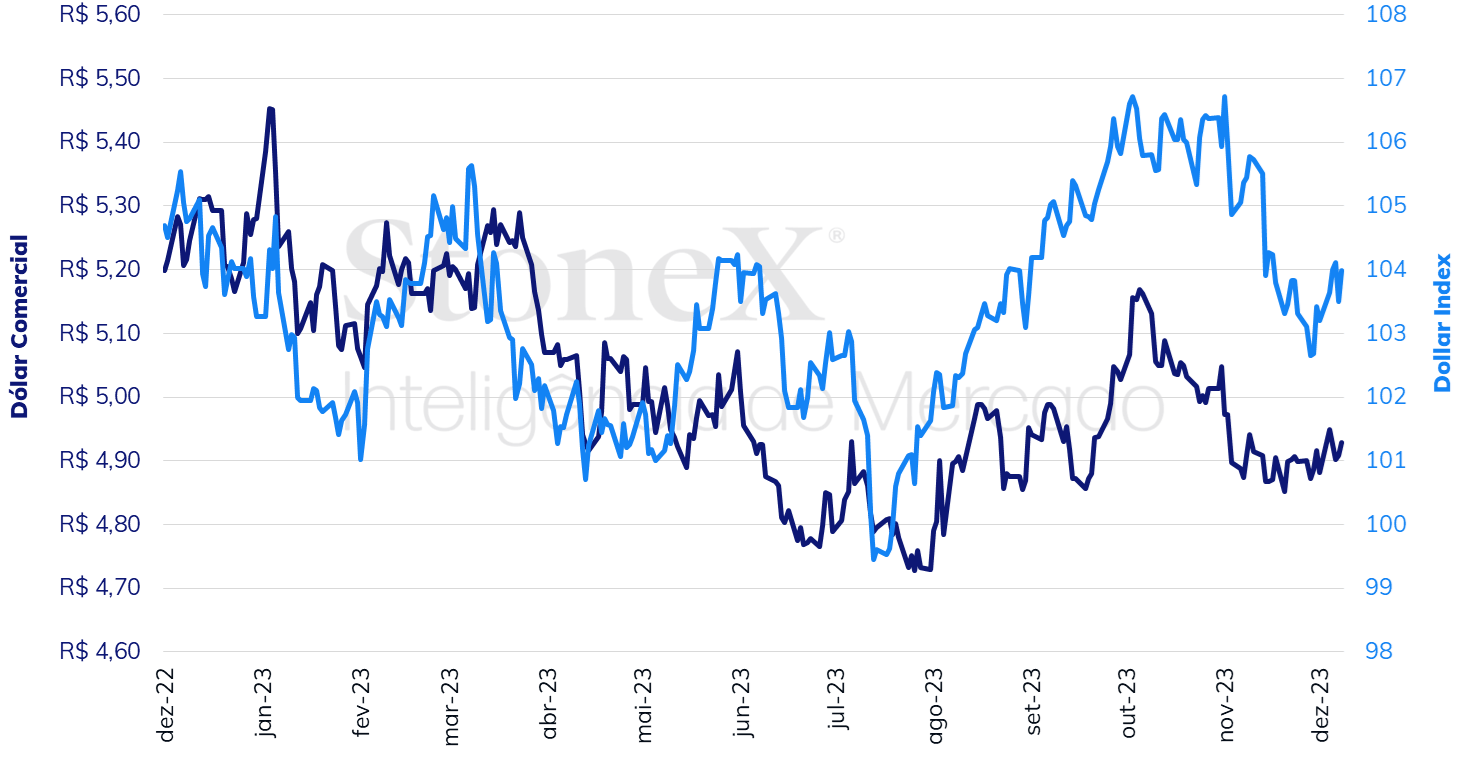

The USD traded in the interbank market ended the week higher, closing Friday's session (08) at BRL 4.929, a variation of +1.0% for the week, +0.3% for the month, and -6.6% for the year. The dollar index closed Friday's session at 104.0 points, a weekly gain of 0.8%, a monthly gain of 0.5%, and an annual gain of 0.7%.

USDBRL and Dollar Index (points)

Source: StoneX cmdtyView. Design: StoneX

THE MOST IMPORTANT EVENT: FOMC interest rate decision

Expected impact on USDBRL: bullish

This week's focus of investors' attention should be the monetary policy decision of the Federal Open Market Committee (FOMC), where there is virtually consensus that interest rates will be kept unchanged for the third consecutive decision, between 5.25% and 5.50% per year. The economic indicators since the last Committee meeting have been milder than anticipated, just like some Committee officials' stance. Thus, it is expected that the FOMC will adopt a more balanced stance, reaffirming the need to observe the release of more indicators to ensure that the trend of price moderation and economic activity smoothing is being confirmed before planning a possible reduction in interest rates. This positioning also reflects the flexibility of the FOMC itself, which seeks to be consistent with the most recent data at its meeting. It is worth remembering that in the monetary policy decision of September 20th, the Committee released more aggressive interest rate projections than in June due to the latest indicators, which showed higher inflationary risks due to better-than-expected performance in economic activity and the labor market.

US November CPI

Expected impact on USDBRL: bullish

It should also be highlighted this week the release of the Consumer Price Index (CPI) for November, which is expected to show an increase compared to October, increasing 0.1% overall and 0.3% in the core of the indicator, which excludes the volatile components of food and energy. However, the November increase will likely be driven by more unstable items, such as used vehicles and airfares. After the Employment Situation Report from last Friday (08) showed a stronger-than-expected reading, with job creation, a fall in the unemployment rate, and wage gains better than estimated by analysts, November's inflation should reinforce the perception that the path to price stabilization in the United States may face some setbacks, which in turn should frustrate the most optimistic bets for cuts in the basic interest rate by the Federal Reserve.

Copom and IPCA

Expected impact on USDBRL: bullish

The Monetary Policy Committee (COPOM) of the Central Bank (BC) is expected to make a new 0.50 p.p. cut to the basic interest rate (SELIC), reducing it from 12.25% to 11.75% p.a. Additionally, the Committee should signal that it will maintain the pace of cuts for the "upcoming meetings" due to the moderation of inflation in the country, the prospect of a reduction in Gross Domestic Product growth, and the recent easing of international monetary and financial conditions, even though concerns about the management of public accounts in 2024 keep inflation expectations slightly higher than desired by Copom members. It is worth noting, also, that the National Broad Consumer Price Index (IPCA) for November will be released on Tuesday, with expectations of a reading in sympathy with the IPCA-15, that is, a slight hike compared to October, around 0.3%, driven by increases in food prices and airfare.

ECB and BoE interest rate decision

Expected impact on USDBRL: bullish

The European Central Bank (ECB) and the Bank of England (BoE) are expected to keep their interest rates unchanged in their monetary policy decisions this week but in slightly different contexts. In the eurozone, investors believe that the ECB may begin to reduce its interest rates as early as the first quarter of 2024 amidst signs of an economic slowdown and inflation rates falling faster than anticipated. Already in England, the economic slowdown is more intense. At the same time, inflation moderation has been a bit slower, which should lead the BoE to keep rates at high levels longer than its unified currency pair.

Economic Agenda in Congress

Expected impact on USDBRL: bearish

The end-of-year parliamentary recess is approaching on December 22, and members of Congress are pressuring the Brazilian Administration due to dissatisfaction related to the release of funds for amendments to the Budget presented by parliamentarians. Still, while the two Powers negotiate, the agenda for the week is full of strategic topics for the government, such as the hearing of Flávio Dino for the Supreme Federal Court (STF) and Paulo Gonet for the Attorney General's Office (PGR), the vote on the bill that regulates sports betting in the country, the vote on the Budget Guidelines Law (LDO) and the Annual Budget Law (LOA) for 2024, and the opinion on the provisional measure (MP) that changes subsidies for investments, including changes to the mechanism of Interest on Own Capital (JCP).

Key indicators

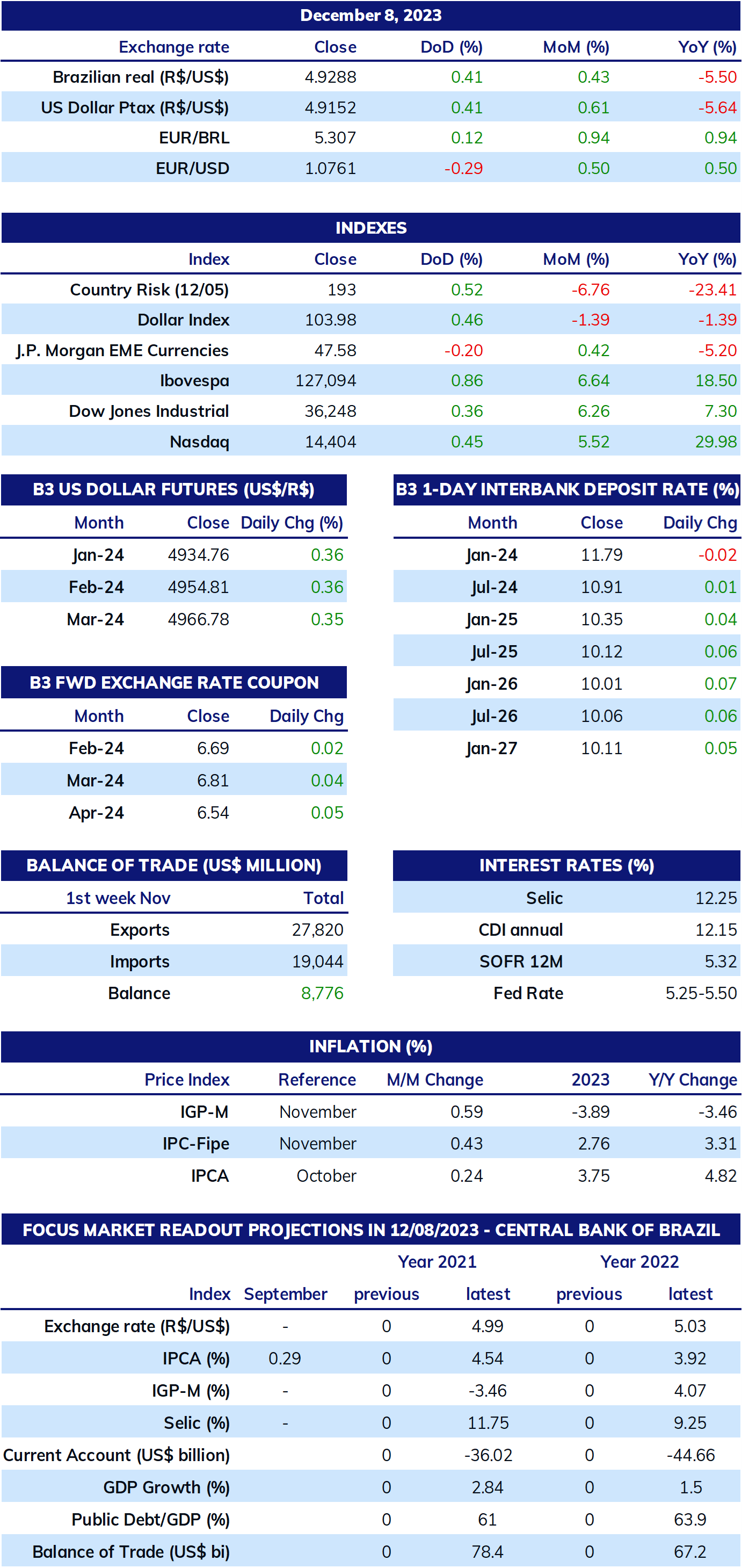

Sources: Central Bank of Brazil; B3; IBGE; Fipe; FGV; MDIC; IPEA and StoneX cmdtyView.

Analysis by: Leonel Oliveira Mattos (leonel.mattos@stonex.com), Alan Lima (alan.lima@stonex.com), and Vitor Andrioli (vitor.andrioli@stonex.com).

Translation by Rodolfo Abachi (rodolfo.abachi@stonex.com).

Financial editor: Paul Walton (paul.walton@stonex.com).

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest US articles

January 5, 2024 03:09 PM

January 4, 2024 06:55 PM

January 3, 2024 07:55 PM

January 2, 2024 08:00 PM