Burberry 8217 s sterling benefits buy some time

There always was a flaw in the logic of Burberry’s share price rise out of doldrums that were amongst the FTSE 100’s worst earlier in the year, to amongst the best.

There always was a flaw in the logic of Burberry’s share price rise out of doldrums that were amongst the FTSE 100’s worst earlier in the year, to amongst the best.

A 30% comparable UK sales surge in the second quarter is quite an achievement. But it was almost entirely due to tourists attracted by the weak pound.

Apart from that, the same Burberry of the recent past was very much in evidence in its first half, reported on Tuesday.

Demand was still crimped in its pivotal region of Hong Kong, where footfall continued to decline and there was another big fall in comparable sales.

On top of that, an issue that will be relatively new for most Burberry investors arose.

A 14% revenue hit from weak US department store orders has drawn attention—they recently represented around a quarter of the total sales.

Sterling’s slide has bought more time for self-help measures—like customer service refinements, cost and productivity sharpening—to take hold.

But the group’s first-half does underline that margin for error remains tight.

A hoped for rebound in erstwhile fastest-growing region Hong Kong is still key—and is nowhere in sight.

Where have Burberry’s Chinese customers gone?

The answer is of course: ‘the world’s other luxury retail spots’ (and not just Burberry stores in them).

The next question is whether the shift has now rendered Burberry’s regional focus superfluous.

Lurking beneath Burberry’s exaggerated-looking share price correction on Tuesday is the worry that affluent Hong Kong flows may simply have evolved beyond what Burberry recognises as its market.

The view will get further backing if rivals like LVMH continue to outperform at constant currencies, as per recent updates.

Its shareholders have, after all, been reacting more to an expected top-line lift from the weaker pound of late, than the group’s inability, so far, to rekindle organic growth.

The group now expects currency benefits in the full year to exceed the £90m it forecast in July and reach at least £105m, given further falls of sterling since July.

And it has kept profit guidance unchanged, whilst its ongoing share buyback programme will help keep shareholders on side too.

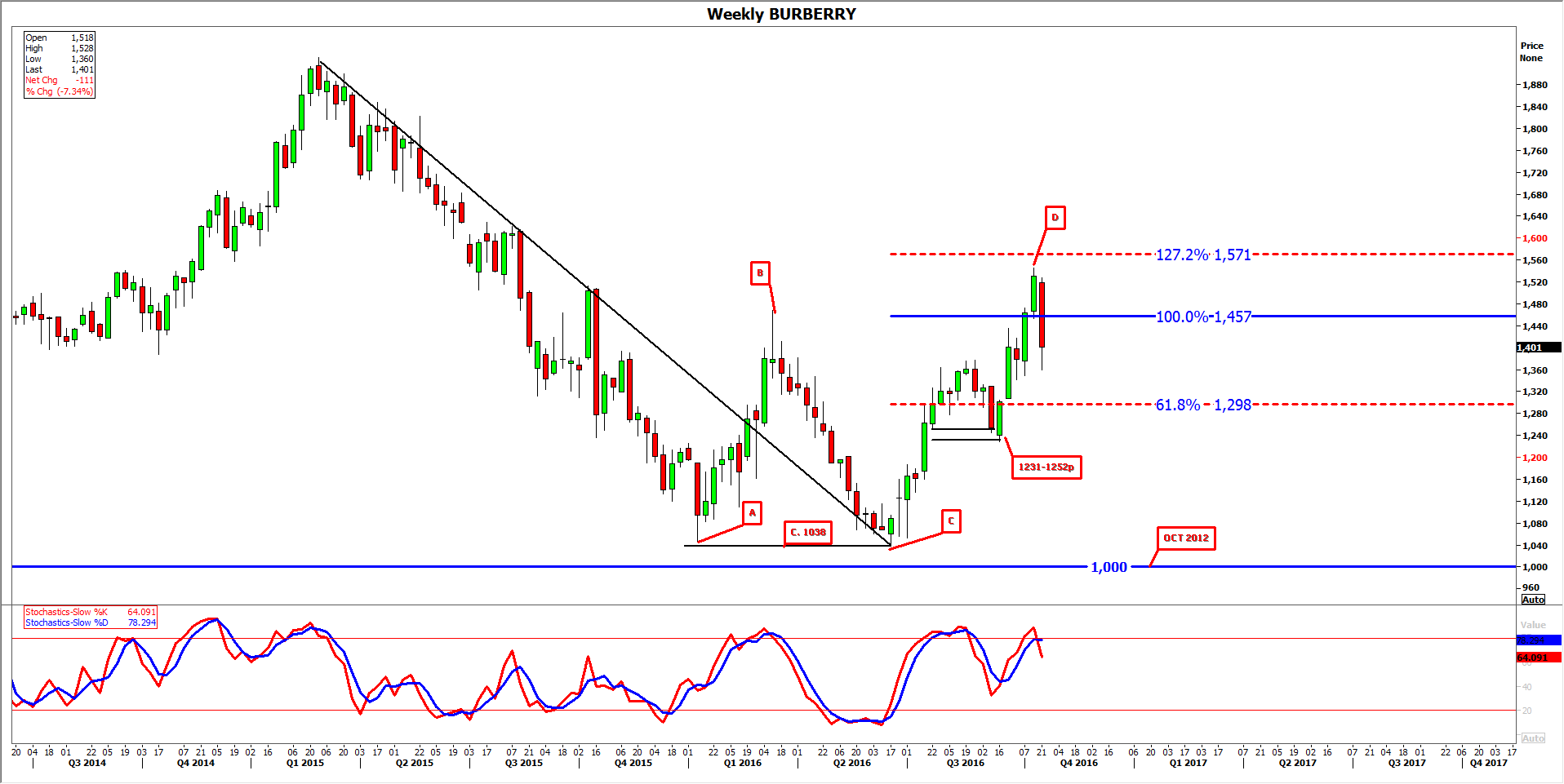

Given the stock duly reversed following the completion of a bearish long-term AB/CD pattern, weakening overall prospects for sustained gains in the medium-term, we expect serious buyers to first wait and see whether support holds: theoretical at the closely watched 61.8% retracement (1298p) and proven in the 1231p-1252p region.

Prices near those late-2015 doldrums will attract again, in the event that either of the above supports are breached.

Please click image to enlarge