UPDATE Rio management in focus after dividend cut

Updated 1636 GMT Rio Tinto has finally bitten the bullet and its ‘progressive dividend’ has bitten the dust. Customary gnashing of teeth among the […]

Updated 1636 GMT Rio Tinto has finally bitten the bullet and its ‘progressive dividend’ has bitten the dust. Customary gnashing of teeth among the […]

Updated 1636 GMT

Rio Tinto has finally bitten the bullet and its ‘progressive dividend’ has bitten the dust.

Customary gnashing of teeth among the remaining investors hoping against hope has ensued—sending the stock as much as 9% lower on Thursday—even if their faith had been puzzling for some time.

Abandonment of Rio’s promise to never to cut its payout from year to year had been on the cards.

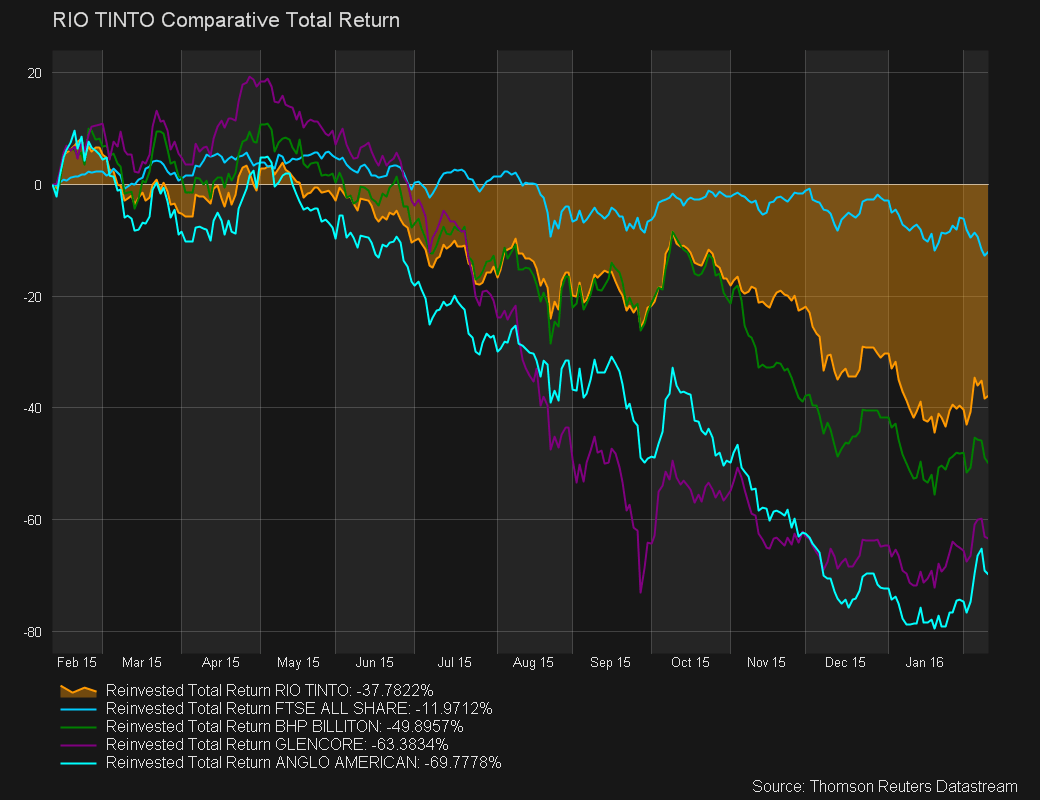

Check out the comparative total return chart below.

Please click image to enlarge

It reveals Rio Tinto had been the most generous to its shareholders amongst the gargantuan UK-listed miners since at least October 2015.

That position was arguably already untenable six months before.

In fact, Rio will still lead the pack even after Thursday’s news.

After all, it has maintained the annual pay-out at the same level as last year of $2.15 per share.

Yet all its rivals are widely expected to cut or even suspend their dividends entirely.

(Rio’s most direct rival, BHP Billiton will release its own earnings in a fortnight.)

On that basis, it might well be that Rio will transition from a ‘progressive dividend’ policy to a ‘progressively lower’ one.

For now, it has promised to pay at least $1.10 in 2016 as a transition to the new policy, limiting any cut to 49%.

The net loss of $866m Rio has been forced to report for 2015 was instrumental in concentrating the minds of its senior managers on the returns policy.

Countenancing payment of $2.15 on 1.19 billion shares floated whilst also writing off a further $1.8bn must have been surreal.

In the end, common sense prevailed.

It might be concerning that it took rather long for reality to set in.

There has been no shortage of pressure, albeit relatively low-key, from investors and ‘encouragement’ from credit rating agencies.

The remainder of the Rio’s main 2015 financial report is also bereft of good news.

“Whilst 2015 was a volatile year, 2016 is shaping up to be even tougher. The macro outlook remains challenging,” Rio CEO Sam Walsh told reporters.

This is the same Sam Walsh who said in 2014: “Now is not a time for the best iron ore producer in the world to take a step back. Now is the time for others to really feel the consequences of the price against their operating costs and for them to make decisions”.

He was of course alluding to the essential ‘do or die’ strategy of the biggest global miners.

In other words, the aim was to defeat rivals by producing the most metal at the lowest cost.

Have Walsh’s words come back to haunt him?

Yes and no.

The strategy had a grim but inevitable logic, which has been vindicated to a degree.

Many of the weakest, costliest producers have been forcibly shunted down the cost curve, and have either had to temporarily shutter production or have gone out of business altogether.

But metal industry production dynamics at a time of global demand collapse and economic retreat, have, of course had dire consequences even for the most cost-efficient producers.

After disquiet among investors, albeit polite, about Rio’s dividend strategy, further consequences cannot be ruled out altogether.

Any management changes that may come would probably disrupt Rio’s already severely kyboshed shares even further.

On balance though, some shareholders may see that as a risk worth taking at this point.

The shares were down some 60% on Thursday, since Sam Walsh took over as CEO in January 2013.

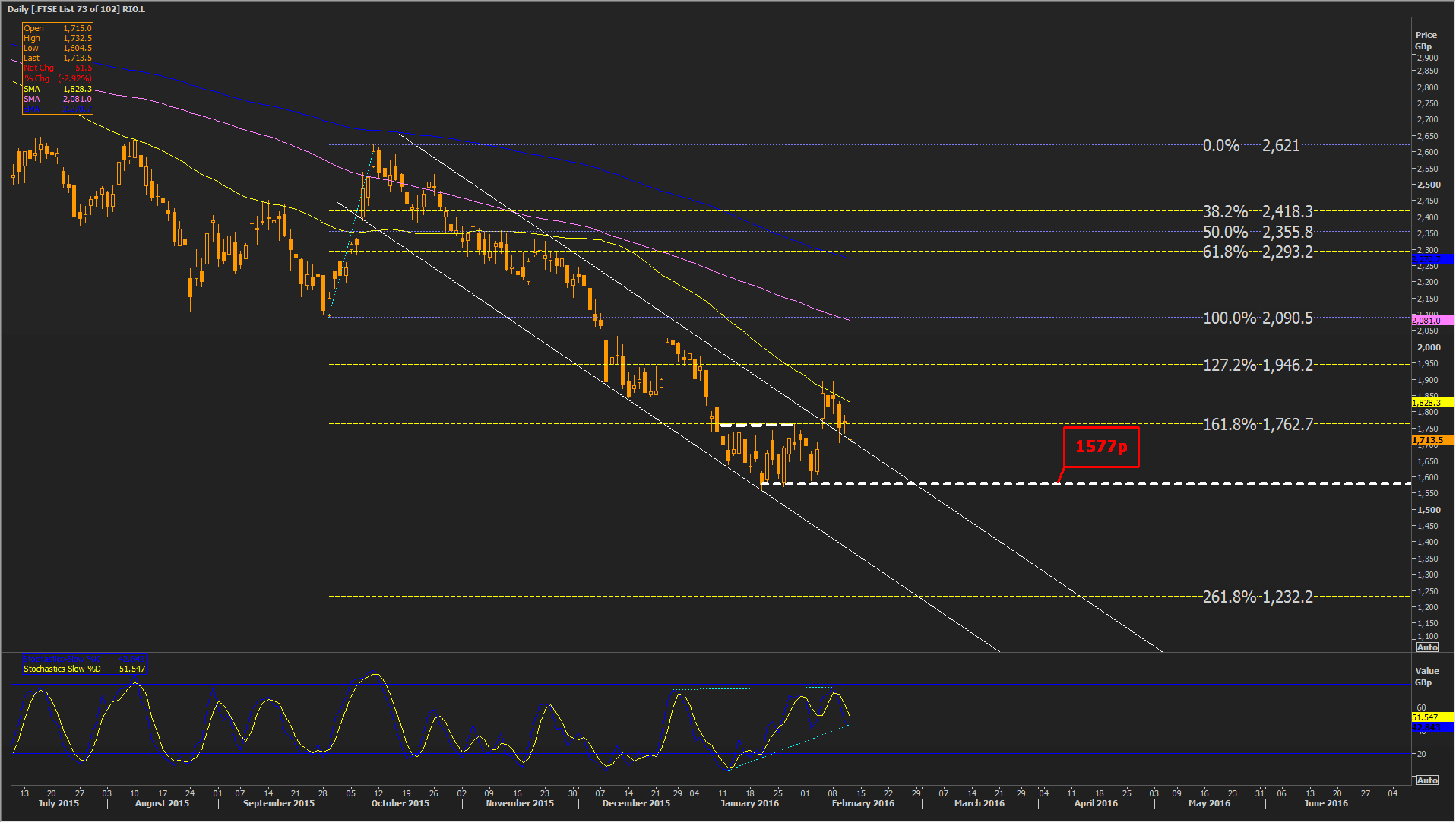

From a technical perspective the shares look set to return to the channel in place since last October, after apparently breaking out last week.

Thursday’s low was just 27 pence from the base of the consolidation zone (1577p) seen since early January.

RIO stabilized in the course of the session after trading as much as 9% lower; corroborating the support.

Stochastic momentum has also been supported for several weeks, though looks set to face a triangle break-out soon.

In the current environment, at best a drift down to fresh all-time lows appears likely.

Topside, clearly, 1762p, which obstructed progress during consolidation is back in play and should be a first hurdle before any sort of recovery.

Please click image to enlarge