Thomas Cook caps comeback year shares tank on bungled CEO change

Thomas Cook announced the shock departure, with immediate effect, of its best-performing CEO for many years. The market reacted by slamming the shares as much […]

Thomas Cook announced the shock departure, with immediate effect, of its best-performing CEO for many years. The market reacted by slamming the shares as much […]

Thomas Cook announced the shock departure, with immediate effect, of its best-performing CEO for many years.

The market reacted by slamming the shares as much as 23% lower.

Whilst some of the selloff was down to the CEO exit, much of the sharp increase in investor caution today should also be put down to Thomas Cook warning that growth will slow to “a more moderate pace” in 2015, as trading conditions become more competitive.

The company said on Wednesday Harriet Green’s remit had been to overhaul the firm, and with this goal now achieved, it was time to “transition” to new leadership.

Green suggested in a statement that her departure was well planned.

“The transformation of Thomas Cook into a company with a market capitalisation of just under £2 billion and a share price of over 130 pence is one I have been proud to lead”, Green said.

She added: “I always said that I would move on to another company with fresh challenges once my work was complete. That time is now”.

Thomas Cook’s chairman Frank Meysman said in the same statement: “The succession plan (Harriet Green) devised will now take effect”.

Later in the morning he sought to damp down suggestions that Green’s departure had beeen hastily brought forward.

He said in press interview that it was always his plan to bring in a new CEO once Thomas Cook was overhauled.

“It’s a matter of balance, everybody has their own qualities,” Meysman told reporters.

“We now move to a new phase where the implementation of (Thomas Cook’s longer-term strategy) is becoming the more important part, and therefore we feel it is time to move to somebody who has been groomed as a CEO who comes from the industry.”

He was referring to Harriet Green’s replacement as CEO, Peter Fankhauser, whose first official day in the job is today.

With Fankhauser having been the firm’s chief operating officer for just a year, the company sought to stress that he is nevertheless a Thomas Cook insider.

He has more than 20 years’ experience in the travel industry, with 13 of those in various roles at Thomas Cook.

However, with little suggestion in recent months that Green was going to leave, and the solid turnaround she has overseen at Thomas Cook since its severe problems just three years ago, there’s some justification for investors to be wary of today’s news.

Even so, there is another fairly material weight on the shares today: TCG said growth this year will be at a more moderate pace due to a tougher trading environment.

This sort of statement immediately reminds investors that Thomas Cook is up against the biggest travel company in the world, TUI AG, and their mutual core market is Europe, where economic growth has stagnated, dampening business prospects.

Bigger players will tend to invest in margins (AKA, price cuts) at the expense of their smaller competitors and this can rapidly turn into a damaging trading environment.

Having said that the former CEO has stripped out costs and improved margins, placing the firm on perhaps the firmest financial footing it has been on for years.

It surely has a fighting chance for the year ahead.

And even under tougher circumstances, I expect TCG’s underlying gross margin performance for next year to remain around the 5-year mean of about 22.38%, not very far from its margin performance for the full-year at 22.3%.

Taking all this on board, it seems likely, the share price fall of 23% after the firm reported a 44% jump in EBIT to £323m, will eventually be regarded as overdone, so long as the firm is able, in time, to convince the market that it was always its plan to make the major management change announced today, sooner rather than later.

It is also worth noting the shares have rallied about 30% from October lows and that these shares were worth around 10p about three years ago.

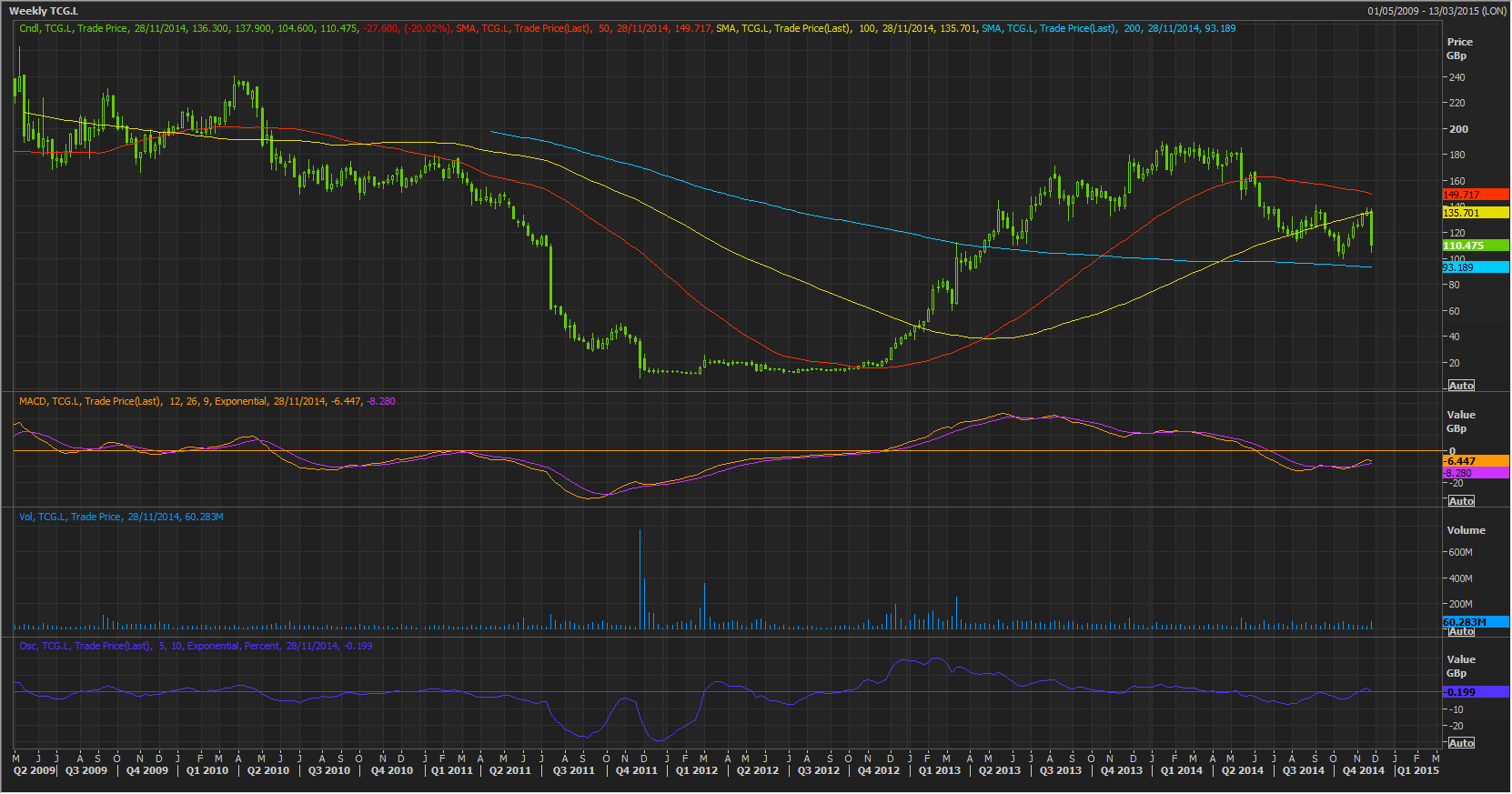

Looking at trading on a weekly basis, it’s already clear today’s drop has actually been fairly judicious, albeit severe–the shares have stopped short of their 200-week moving average.

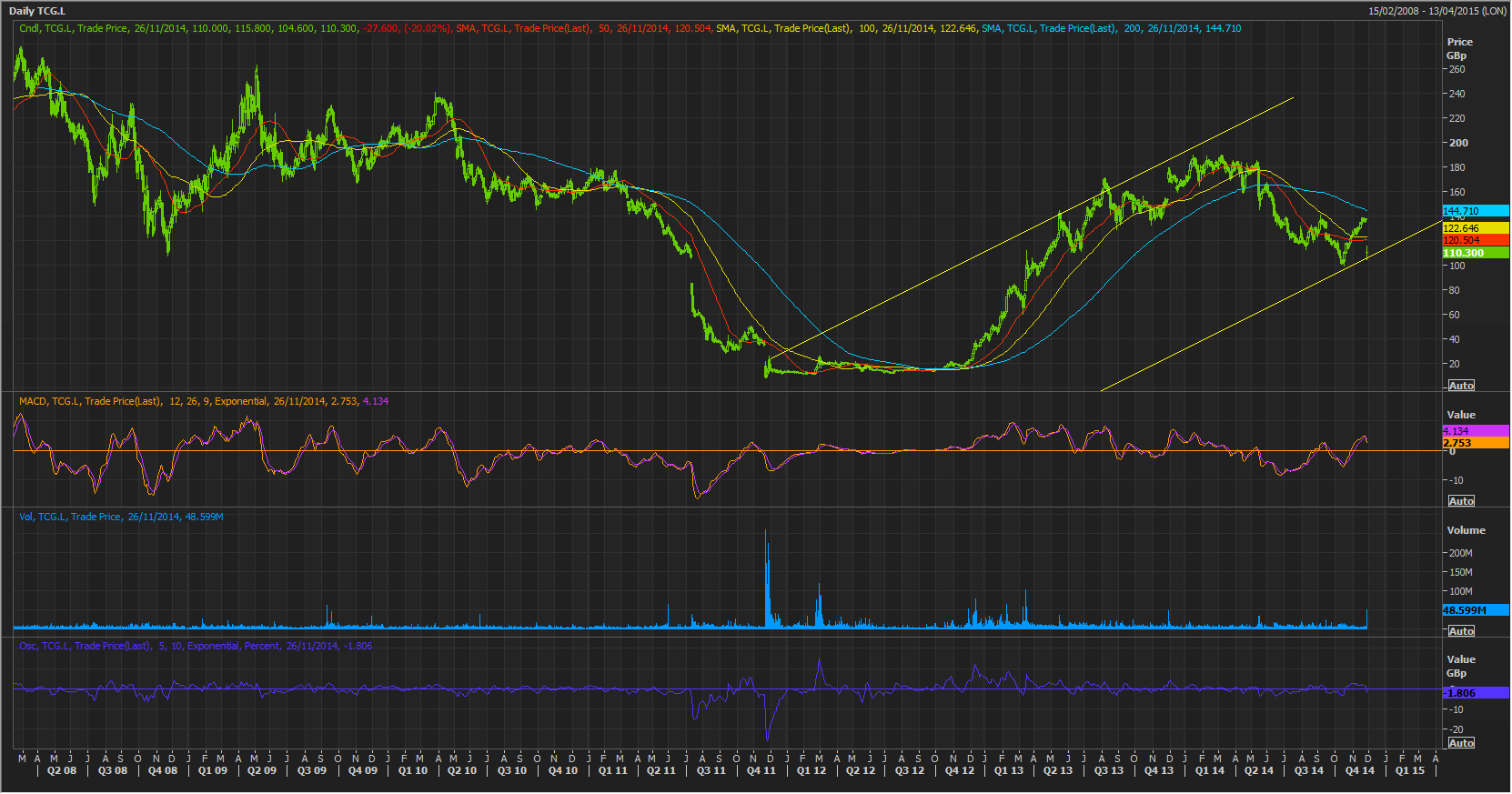

On a daily basis, bulls will not want to see the stock fall much further, given that they would leave the wide recovery channel commenced three years ago.

Selling momentum is not in fact biased to the downside (Moving Average Convergence Divergence is above the ‘zero’ line) though it may be pushed that way by sentiment today.

(It’s interesting to note there was a gigantic order in the market today by the international arm of US brokerage Jefferies.

At the time of writing, the order constituted 25% of all institutional trading in Thomas Cook shares tracked by Thomson Reuters. The brokerage has been quoted in the media today making strongly bullish statements on Thomas Cook stock.)

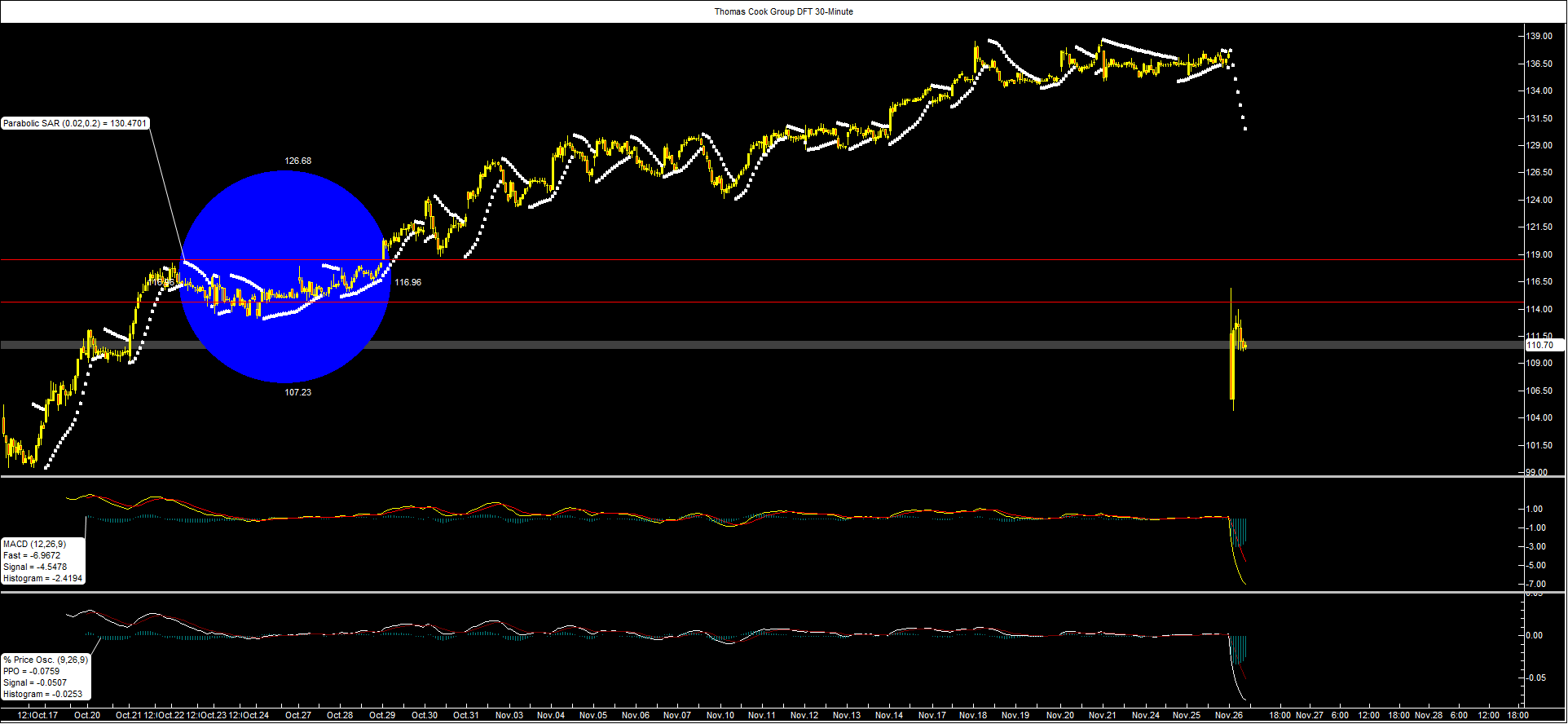

City Index clients trading Thomas Cook Group Daily Funded Trade are less bullish, judging from the chart below showing 30-minute intervals in today’s dealing.

Former support from late October is now acting as an effective resistance, between the late 114s to just under 119, whilst the title is seeing support close to 110, as selling momentum starts to look stretched on a half-hourly basis.