Tesco keeps the kitchen sink

It looks like Tesco CEO Dave Lewis took the opportunity offered by its shares bumping along 10-year lows last week, to wash out more bad news. And so […]

It looks like Tesco CEO Dave Lewis took the opportunity offered by its shares bumping along 10-year lows last week, to wash out more bad news. And so […]

It looks like Tesco CEO Dave Lewis took the opportunity offered by its shares bumping along 10-year lows last week, to wash out more bad news.

And so we come to Tesco’s fourth profit warning in five months (including the profit restatement).

The supermarket now says group trading profit for its financial year ending in February 2015 will not exceed £1.4bn.

That compares with the £1.94bn expected by the average of a bunch of analysts’ forecasts compiled by Tesco itself, putting today’s downgrade at about 30%.

This time, Tesco is linking its revised forecasts to the recent changes and investments its made in an effort to turn itself around and clean up its act.

“In recent weeks we have implemented new policies and procedures which will govern our commercial income activities and taken actions to invest in and improve our customer offer”, the supermarket said in its statement this morning.

Tesco reminds the market that it did warn, at the time of its interim results on 23rd October, that full-year profit would probably be damaged by actions it might soon have to take in the wake of admitting it inflated profit figures by some £75m.

Tesco also today suggested it has made efforts to improve long-term relationships with suppliers, aiming to communicate a better awareness amongst them and its own managers of its retail channels, thereby reducing the risk of misstated or erroneous inventory assessments that could erode credibility of revenue recognition.

Today the firm is stressing that the broad review it implemented since the autumn and the first fruits of the strategy revision that the supermarket has begun to implement, are starting to have positive effects.

Of these changes, Tesco singles out its hiring of 6,000 more staff, in order to bring a more personal touch, and frankly, at times, to offer customers directions in its often cavernous stores; changes in availability on key lines and, yes, the ubiquitous ‘investments in price’ (cuts).

“The early feedback from customers is encouraging,” Tesco said.

Arguably though, customer feedback may have suggested the changes so far will not be good enough to propel Tesco above a threshold it calculated it needs to exceed during the retail sector’s all-important winter holiday season, if we take today’s profit revision at face value.

On the other hand, as I suggested at the beginning, there are lots of reasons to see today’s warning as a strong strategic gambit from Tesco’s recently refreshed C-Suite.

At best, lowering investor expectations before the retail sector’s all-important winter holiday season instantly provides a better basis upon which to challenge profit and revenue expectations after the season has passed.

The main problem I can see from Tesco’s statement today is that there’s little evidence within the strictly measured and precisely weighed words that more forecast downgrades are not in the works.

Indeed, Tesco has taken great pains to avoid any implication that today’s profit warning draws a line under its recent troubles for the long term.

Therefore we are obliged to expect further profit warnings in the relatively near term.

We might at this point also revisit the basic play book for ‘special situations’ like the one Tesco is currently in:

It’s worth bearing in mind that history has shown when firm’s like Tesco are still trading on at least parity of prospective total market capitalisation (price) to book (valuation), to use one crucial valuation metric, pressure for a rights issue is still only moderate.

Even so, all things considered, the overall picture suggests there have been no material changes in Tesco’s outlook compared to when it released its last major results late in October.

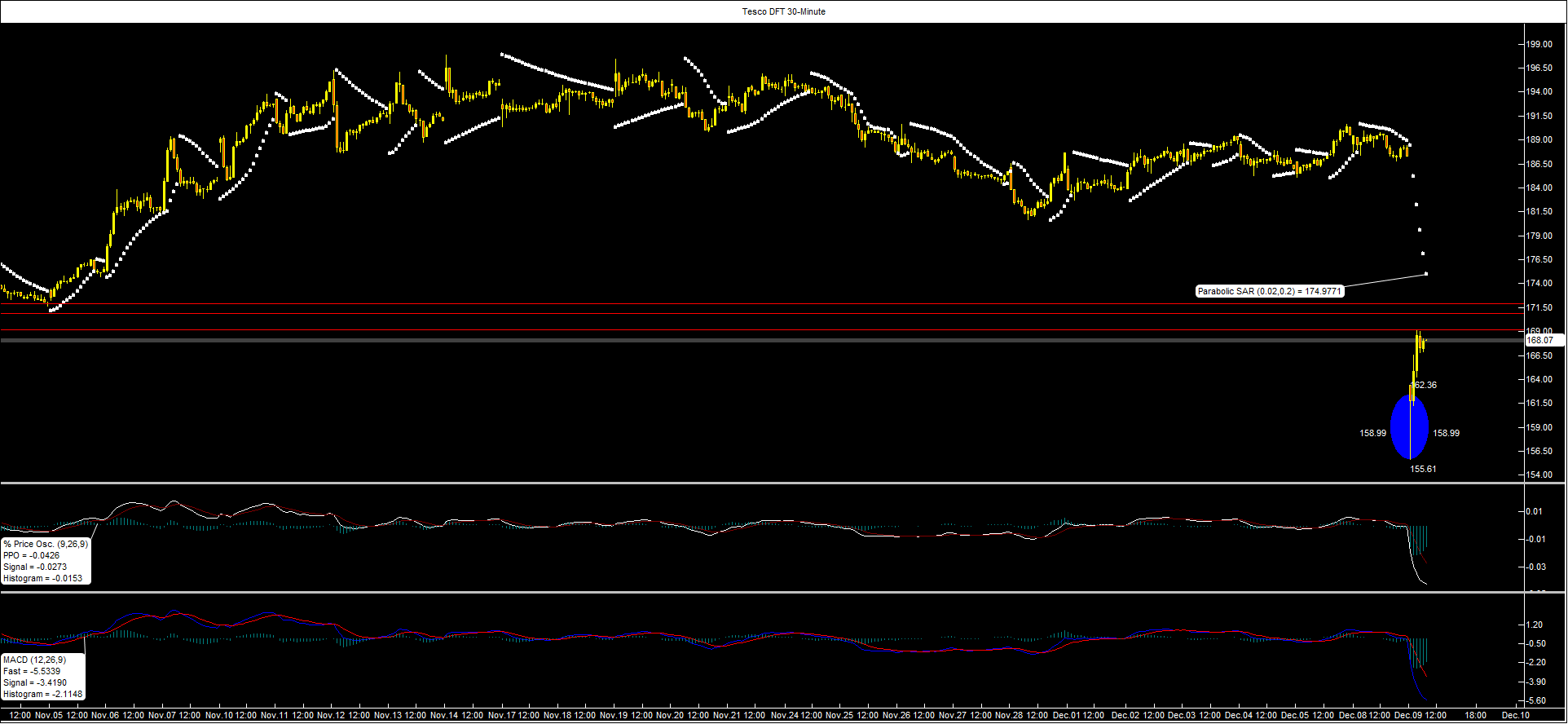

It was that basis at the time which increased our confidence that significant sections of the market continued to visualise Tesco stock prices toward and slightly below 160p.

And that remains our broad view.

The last significant visit to such levels was in 2000 (the closing price on 9th February 2000 was 156p and the opening price a day later was 160p).

Those levels also seem to be magnetic for traders of City Index’s Tesco Daily Funded Trade.

Having said that, we note the title has now plumbed the equivalent of slightly lower prices, having seen 155 earlier this morning.

With momentum indicators markedly extended on a half-hourly basis, it’s likely the early morning visit to 155 will be the DFT’s weakest point, for the very immediate term.