Sky shares shine after customer influx despite 475m write off

Sky Plc. said on Tuesday profits jumped 20% as the picture in Germany and Italy improved and this powered its shares back up to levels […]

Sky Plc. said on Tuesday profits jumped 20% as the picture in Germany and Italy improved and this powered its shares back up to levels […]

Sky Plc. said on Tuesday profits jumped 20% as the picture in Germany and Italy improved and this powered its shares back up to levels not seen since 2001.

The company that was formed from combined UK, German and Italian subsidiaries last year, said new customers in Germany and Austria joined in record numbers during the nine months to the end of March, and it saw the best third quarter for customer growth in Italy for three years.

Satellite and online TV customer growth in its core UK operations grew 41% to 127,000 in Q3, the biggest influx of new users in 11 years, Sky said.

Across the group, new customer additions rose at 242,000, 70% higher in Q3 than in the third quarter a year ago.

So-called ‘churn’ or customers who dumped Sky’s services during the period showed a “stand-out performance” in each region, Sky said.

Strong customer sign-ups are Sky’s lifeblood and the news that these hit a more than 10 year record gave the FTSE 100 stock a firm leg-up.

Still, the main profitability measure that Sky and the market focus on, earnings before interest, taxation, depreciation and amortisation (EBITDA) rose 20%—and that was just in line with expectations.

Additionally, the EBITDA figure is presented on an ‘adjusted’ basis.

These adjustments were probably at least partly related to Sky’s attempted metamorphosis from a primarily UK-facing broadcaster before consolidation of its European assets, to one looking more widely to the continent and beyond, after the tie-ups.

Sky said depreciation of assets—almost certainly including some of the recently unified European ones—together with debt payments (amortisation) eroded £475m from earnings during the nine-month stretch, leaving £1.03bn.

Adding back the fall in value from the adjusted EBITDA, the 9-month profit could have been closer to £2bn.

Whilst the slippage in value might have largely been expected by analysts, given the scope of disparate assets Sky has undertaken to concentrate into a single entity, there seems a fair risk of further instances of depreciation in the quarters ahead.

That would tend to reduce the margin of error for Sky, in terms of top-line expectations for 2015.

In turn, such fears can also be linked to Sky paying £5.136bn, 70% more than before, to the Premier League to keep hold of the 7 package football rights for another year.

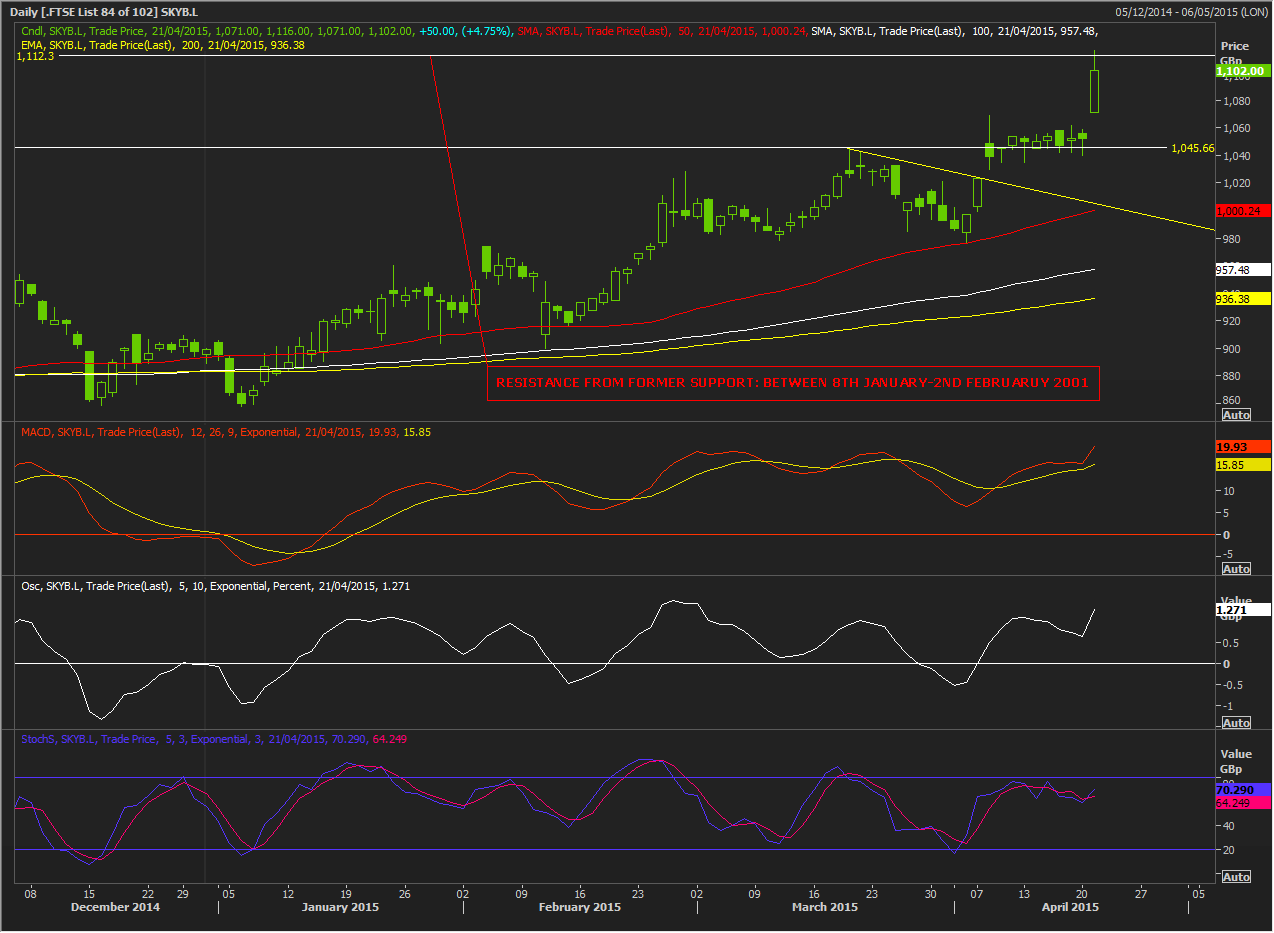

With depreciation risk and the financial leeway reduced by the rights deal, Sky shares could be regarded as ‘toppy’ right now, given they’re at their highest levels for about 14 years.

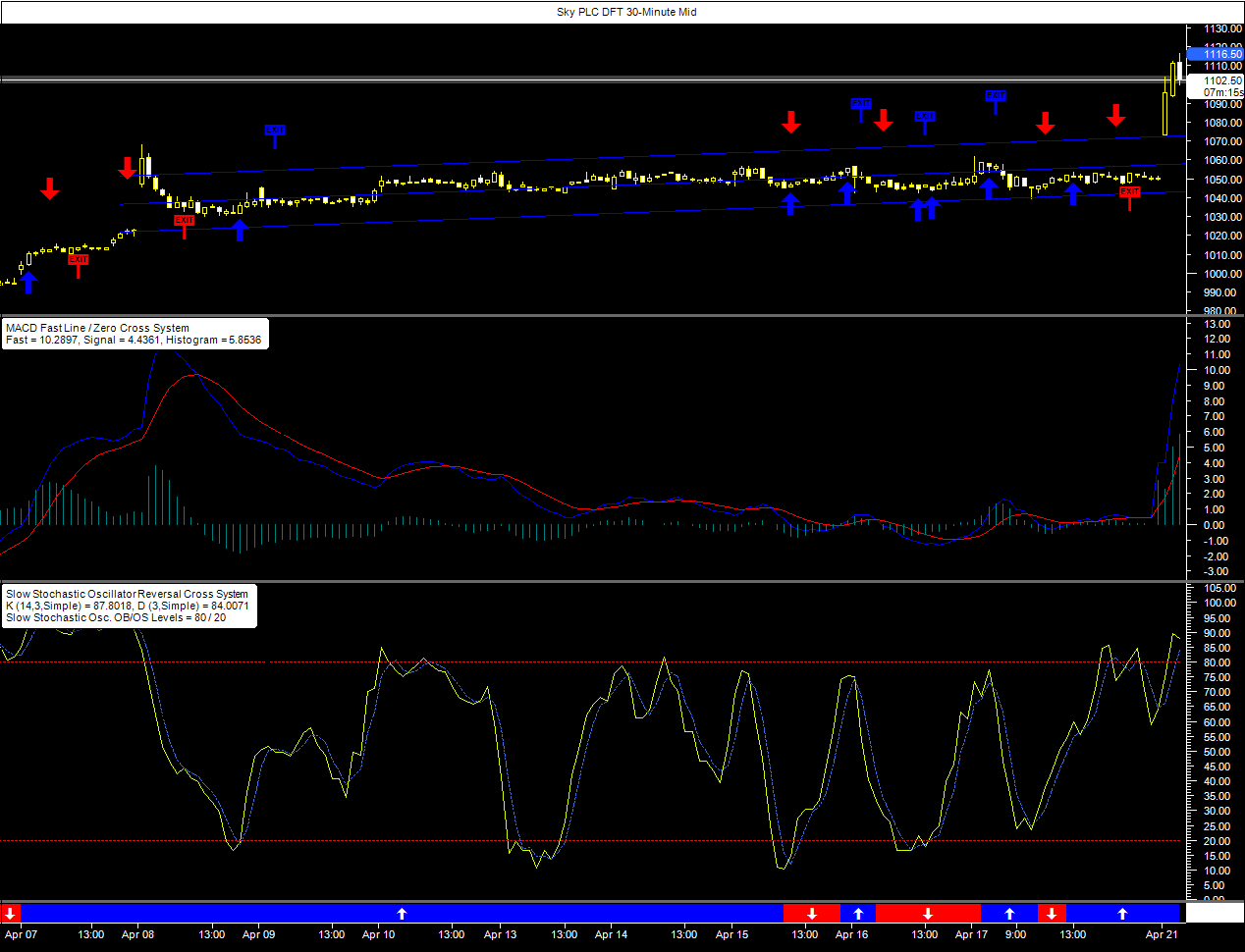

Shorter-term traders of Sky Plc. Daily Funded Trade offered by City Index are, along with investors in the stock, riding the wave of good sentiment from the customer milestones.

But in the half-hourly time frame, the strong upside momentum looks to be at the top of its stochastic cycle and will probably soon reverse.

The DFT has largely been cradled in a distinct channel for the past fortnight and is likely to remain so, unless the market reassesses sentiment more broadly.

The risk of that somewhat longer-term reassessment seems moderate, given that the same Slow Stochastic indicator deployed in the stock’s daily chart reveals that upward momentum could very well be definitively overbought by the end of Tuesday’s session.