RBS shares flop on very trying results

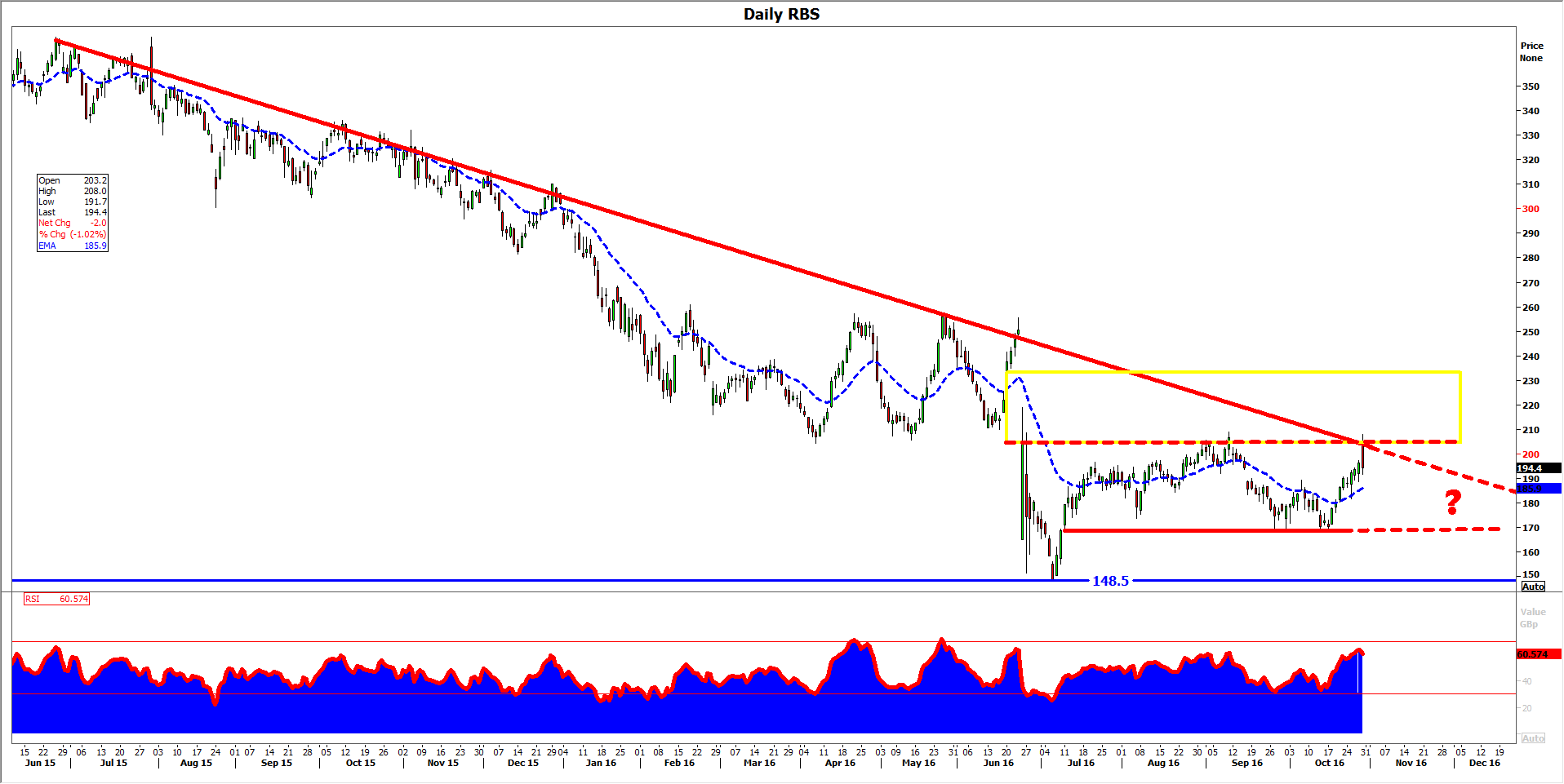

Royal Bank of Scotland’s short-lived rally on Friday speaks volumes.

Royal Bank of Scotland’s short-lived rally on Friday speaks volumes.

Shareholder relief was evident in the immediate reaction to the group’s third-quarter numbers—Britain’s most troubled lender had, after all, emerged from the summer’s volatility in no worse shape than before, albeit no better.

The shares subsequently slipped from their initial 6% jump to fall 1.7% on the day.

Some £1.194bn of value erosion easily swamped £255m of operating profit, and group return on common equity (ROE) still points to low viability, though at 4.6% the Q3 snapshot is obviously a welcome improvement on the negative trailing 12-month result at end Q2.

The strategy of Messrs McEwan and Stevenson looks close to optimum, and has helped the group beat adjusted operating profit expectations (£1.3bn) by some £560m.

At some difficult to define time in the future, there are good reasons to think RBS’s big push to remain UK Plc.’s biggest lender will be applauded too.

A 71% jump in adjusted income at Corporate and Investment Banking to £526m would be outstanding, if the context were more favourable.

It helped keep the attributable loss (£469m) contained well below a widely expected plunge of about £900m into the red.

And the extra wiggle room helped pump the all-important common equity tier one ratio up 50 basis points to 15%.

The ‘albatross division’ ate up another £300m of cash in Q3.

Talks over a sale continue, says its owner, whilst admitting it will miss its own pushed back deadline.

By default, it’s also the EU’s deadline for a sale by the end of 2017, a condition for Europe agreeing to waive state aid rules in 2008.

Meanwhile, no sale, no dividends, according to stipulation by the government, which still owns 70%.

We, like others, though, are not entirely convinced that an addition hasn’t just been delayed.

We note £3.5bn of RBS’s current £4.7bn total PPI set-aside had been utilised by the end of June, whilst the FCA’s new claims deadline is June 2019.

Furthermore, the bolstering of legal provisions, and lack of insight offered into the U.S. mortgage investigation, underlines that provisioning will remain grim.

Please click image to enlarge