RBS s seventh straight annual loss unlikely to be its last

RBS news flow over the last week had been signalling that investors needed to wind-back hopes of a profit in 2014, after seven-straight years of […]

RBS news flow over the last week had been signalling that investors needed to wind-back hopes of a profit in 2014, after seven-straight years of […]

RBS news flow over the last week had been signalling that investors needed to wind-back hopes of a profit in 2014, after seven-straight years of losses.

Sure enough, instead of the £3.9bn adjusted profit investors were hoping for, judging by even the most recent consensus forecasts, the 79% UK government-owned bank booked a £3.5bn loss.

It apparently decided to continue for another year, the long, painful wash-out of missteps it made during more fortunate times.

This time, the loss was due to a write-off from RBS’s problematic US-based Citizens business, charges from various foreign exchange investigations and for provisions related to mis-selling of financial products.

This brings the total losses reported by the bank since the financial crisis to £49.5bn, more than the £45bn UK taxpayers paid to bail it out in 2008.

Even so, unfortunately, further annual losses seem all but inevitable.

There was some more positive disclosure this morning—it included that RBS is continuing to withdraw from riskier business activities, aiming to concentrate on its core domestic clearing and lending segments.

It said it’s exiting from 25 countries in the EMEA region.

It’s also reducing assets within institutional-focused businesses by 60% over 5 years.

On the closely-monitored capital adequacy issue, RBS announced its Core Tier 1 ratio improved to 11.2% by the end of 2014 from 8.6% the same point a year before, and the bank now targets CT1 at 13%.

These capital achievements and targets represent decent progress on the regulatory capital front, leaving regulators at least one less stick to beat the bank with.

Additionally, the implied reduction of provision capital RBS may have to set aside without the expenses of more volatile businesses has raised hopes that the bank may be moving closer to being able to recommence dividend payments.

The bank said by next year it hoped to be able to start discussions with UK regulator the Prudential Regulatory Authority (PRA) about resuming dividends.

RBS’s CEO has made it clear such talks would wait until one of RBS’s numerous litigation costs, this one from the US probe into the sale of mortgage-based bonds, had peaked.

That’s expected to happen this year. In turn, any talks over dividend would be unlikely to bear fruit for shareholders before 2016 financial year at the earliest.

As the day progressed, this realisation and also what appear to be indirect cautions within RBS’s full-year statement about potential for costs to come in higher than expected, have weighed on its share price.

In its statement, the bank noted with reference to “conduct and litigation issues” that it was “possible that the costs relating to settling these could be substantial in 2015”.

RBS shares had traded as strongly as 2.4% higher earlier on Thursday, but eventually, lost those gains and fell almost 4% lower than Wednesday’s close.

Additionally, a number of independent research notes circulating in The City in the last few weeks suggested RBS faces a higher burden from increasingly stringent capital adequacy assessments.

These views are centred on the Bank of England’s new stress testing regime (the first tests were run in December).

The BoE’s regime is expected to soon coalesce with international tests overseen by bodies like the European Banking Authority, under the “Basel III” framework.

Broadly speaking, the upshot for all UK banks is likely to bring increased provisioning and impairment charges and possibly weaker capital ratios.

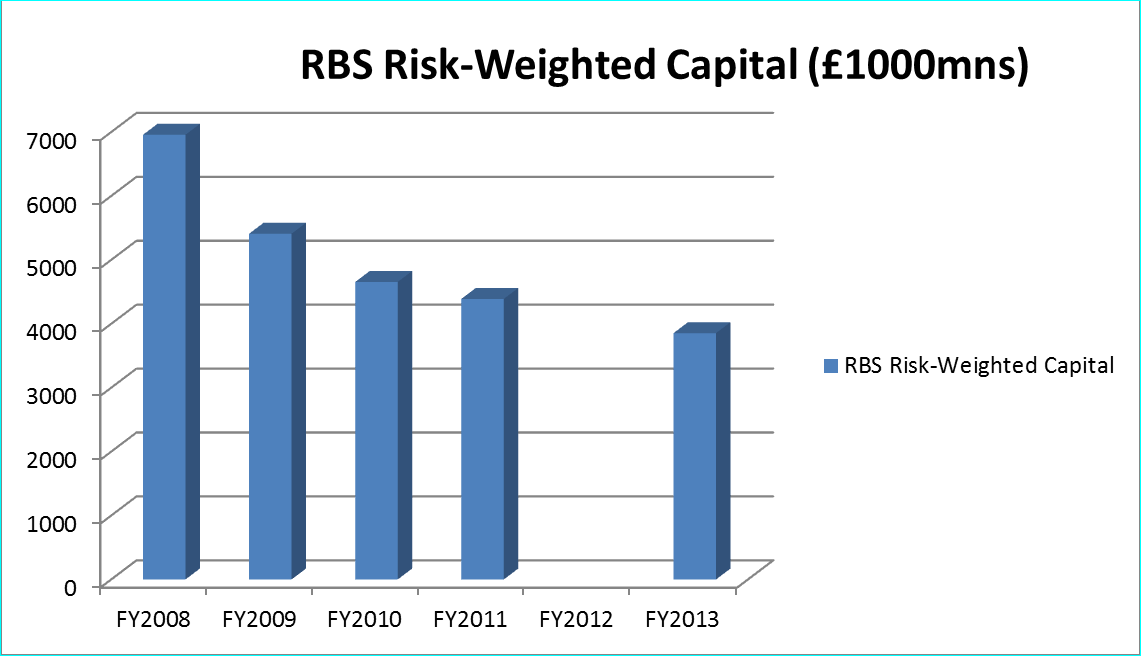

With average provision per risk-weighted capital at RBS latterly around 0.2%, the concern is that there could be a reversion towards its circa-2% run rate of the last five years.

Whilst RBS’s risk weighted assets (RWA) are falling, as it makes progress with its strategy of reducing risks on all fronts, even a moderate uptick in related costs would severely damage profitability.

Source: Thomson Reuters

The bank stated on Thursday that it managed to lop off another £40bn in 2014 from its RWA tally of £385.5bn the year before, suggesting RBS’s regulatory risk capital stood at £345.5bn by year end.

That implies impairment charges or provisions could have been be as high as £6.91bn–about double the total of these costs in the current year–assuming RBS returned to prior average levels of such costs.

(Join Chief Market Strategist Josh Raymond for a @CityIndex #markettalk session on banks on Friday, 1pm-2pm. Lloyds Banking Group reports annual results on the same day and Barclays on Tuesday).

Despite these risks, even a cursory look at RBS charts shows investors are now very well habituated to the seemingly never-ending train of negatives from the bank.

Trading in the stock today has seen an uptick in volatility (see the sub-chart line in blue that displays the extent of variance from the stock’s last closing price).

But again, whilst these jumps are occasional, they’re certainly common for RBS stock, and for most of its larger peers, as they come to terms with an era of increased scrutiny of their business practices.

For shorter-term trading, the main point of interest is the equivalent of 389p support, which the Royal Bank of Scotland Daily Funded Trade offered by City Index is currently testing, in a half-hourly view.

I have also drawn a light red line in the chart of the underlying stock at the circa-385p level (please see the first chart).

In combination, the range 385p-389p and its equivalent for RBS DFT, are likely to prevail for the rest of Thursday’s session.

The attached momentum trading systems strongly suggest the current wave of the sell-off is close to limits.

However, there has been no signal from the Slow Stochastic Reversal system since it triggered an exit from its last long trade at 4pm on Wednesday.

Adhering to strict stochastic concepts dictates exits from short holdings will occur only when the ‘slow’ moving average (blue) line crosses above the yellow ‘fast’ one.