Morrisons gets benefit of doubt after bleak but steady quarter

Another big fall in quarterly underlying sales at Morrisons. It’s continuing to be hurt by its decision to cut prices in a bid to stem […]

Another big fall in quarterly underlying sales at Morrisons. It’s continuing to be hurt by its decision to cut prices in a bid to stem […]

It’s continuing to be hurt by its decision to cut prices in a bid to stem market-share losses to discounters.

Like-for-like sales were 6.3% lower in the third quarter to 2nd November.

This looks to be quite a bit worse than forecasts for a decline of 5.2% although it’s not as bad as the 7.6% fall in the quarter before.

This theme of ‘bad, but not as bad as before’ is one which echoes throughout Morrisons’s statement this morning.

Still, the sales slippage seems to confirm Morrison has lost out in the war against ASDA for the Number 3 position in UK groceries.

We know ASDA is the only major UK supermarket to have actually increased market share in the last few months, and today’s figures from Morrisons actually suggest Morrisons weakness relative to ASDA deteriorated in the last few weeks.

Some further bad news here: a mini profit warning.

WM Morrison has reduced guidance for underlying pre-tax profit for the full year to £335m-£365m, having expected £325m-£375m before.

The supermarket explains the unexpected forecast cut by saying it is spending £65m more in new business development costs than forecast earlier, and it now sees £70 million pounds more in one-off costs.

The additional slowdown in profit is possibly ‘small change’ in context though, when we remember full-year profit in 2013-14 was £785m.

Morrison was already forecasting profit would more than halve, compared to the year before. Its outlook has today been worsened slightly.

Yes, it’s raised the minimum level of profit it expects to make, but Morrisons is now also saying the maximum profit it will make this year is £10m less than previously forecast.

The supermarket, which in March embarked on an unprecedented multibillion pound program of investments, divestments and cost cuts, reiterated this morning that it does not expect to see major benefits from its turnaround plan before the end of the second half of its next financial year.

Morrison is trying to draw attention to ‘items-per-basket’ this morning. Again, it’s trying to promote the view that even though the average amount of stuff Morrisons customers buy is down 2.4% in Q3 year-on-year, this fall is not as bad as the one seen in the fourth quarter of last year, when customers cut down the amount of items purchased from the supermarket by almost 7%.

It’s worth remembering when looking at such metrics that the average price of a basket of groceries this month was about 0.2% less than a year ago, according to recent retail data.

One improvement which the market will probably take more seriously: the grocer now expects year-end net debt to be £2.3bn-£2.4bn, £100m better than initially guided and £400m-£500m lower year-on-year.

Unlike its rival Tesco, Morrison therefore has a lower risk of seeing its credit rating being moved closer to ‘junk’ by rating agencies, which would increase its debt servicing costs.

These are bleak numbers overall, and they look even bleaker in the context of the relatively promising results we’ve had this week from Primark and Marks & Spencer.

However, something seems to be afoot among investors in the UK retail sector, judging by the reactions to the earnings reports and trading statements from the raft of big-name retailers that have reported this week.

Among these, only Primark’s can be said to be in any way a ‘blow-out’ strong set of results.

Both Marks & Spencer’s earnings yesterday and Morrisons’ this morning were just relatively steady—not absolutely astounding. Far from it.

It seems investors are happy to take the relative view on retailers at the moment, following several bleak developments in the sector this year.

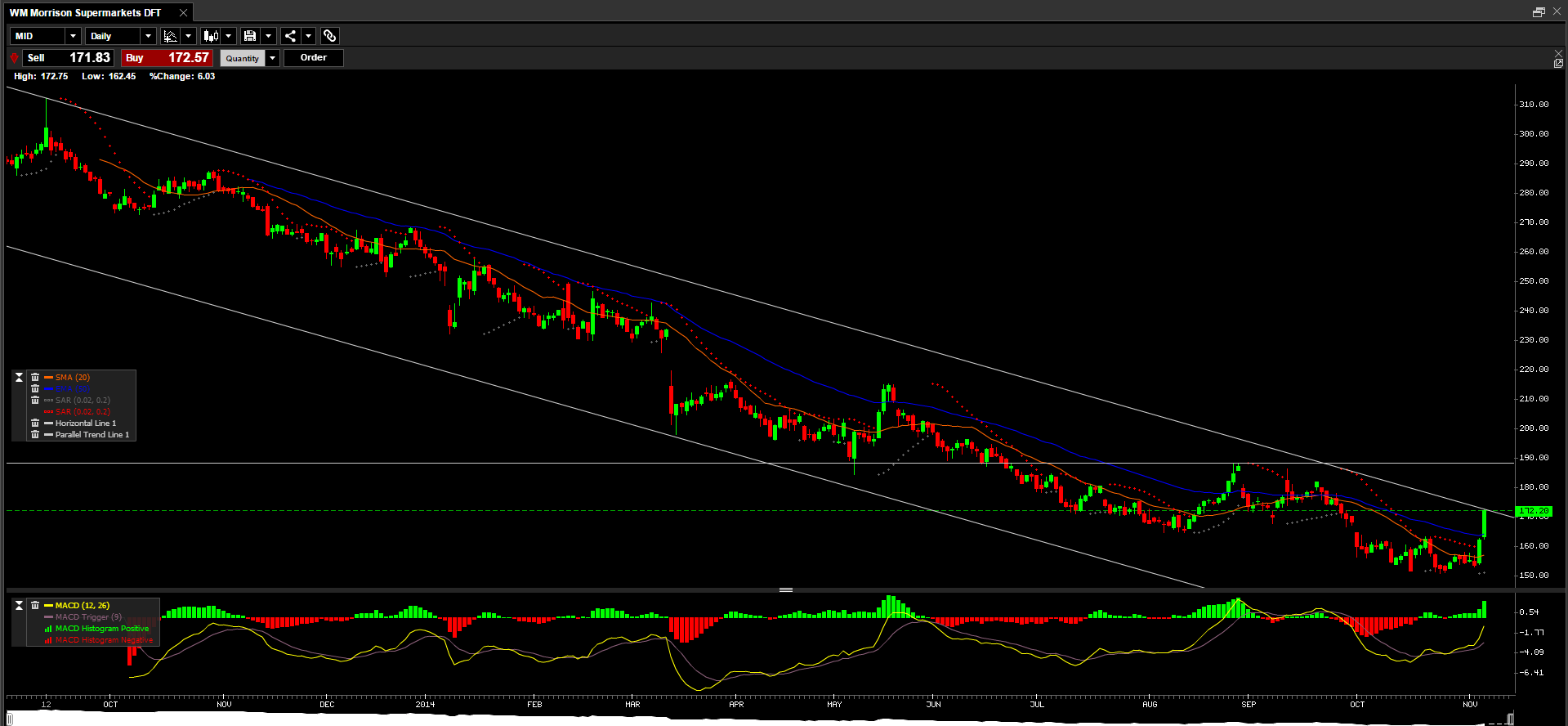

Like M&S, Morrisons stock has opened firm and is trading firm, with another rise approaching 6% adding to a 6% gain of the stock on Wednesday.

On that basis, City Index clients trading WM Morrison Supermarkets Daily Funded Trade certainly seem willing to test levels close to the stock’s peaks in August and September. Though there appear to be hurdles for the trade getting above the current level which seems to be near the top of a trendline