Marks amp Spencer shares surge as food sales remain firm

Marks & Spencer shares opened more than 8% higher, confounding earlier expectations they would fall, after the retailer confirmed its 13th consecutive fall in underlying […]

Marks & Spencer shares opened more than 8% higher, confounding earlier expectations they would fall, after the retailer confirmed its 13th consecutive fall in underlying […]

Marks & Spencer shares opened more than 8% higher, confounding earlier expectations they would fall, after the retailer confirmed its 13th consecutive fall in underlying non-food earnings and tied itself to a sector trend of blaming poor clothing sales on the weather.

After such a long run of disappointments from one of the UK’s largest clothing retailers, in M&S’s case at least, the weather story is wearing thin.

The quarterly non-food disappointment was very much driven by clothing and general merchandise, with Marks & Spencer somehow being wrong-footed, despite 130 years of experience and some of the most sophisticated space and inventory management systems in the world, by a spate of unpredicted mild weather.

Guidance for non-food has risen, which is a small positive, but perhaps that’s the least we could expect, in the hope remedial measures are being taken.

The market has no doubt given Marks some points that first half profits are ahead of forecast at £268m, even though online sales dropped another 4.8%, on top of the 8% decline in the first quarter.

Food like-for-like sales growth is in-line at a measly 0.2%, and although on the face of it, one might be surprised this could win the retailer any brownie points, given the near-collapse of the UK’s grocery sector under sustained attack from discount upstarts, the market is lauding Marks’s food performance.

These may not the best half-yearly M&S numbers, but with food continuing to constitute around 50% of total M&S revenue, there is arguably some justification for the market’s apparent satisfaction with these results, as signalled by the rise in the firm’s stock this morning.

Once the knee-jerk stock market reaction of the morning has worn off though, we continue to expect M&S CEO Marc Bolland’s strategy to come under scrutiny.

Despite Bolland overseeing an expenditure programme of about £2.3bn over the last few years, EPS growth dropped from almost 17% in 2010 to -6.1% in 2013, a year after he took the helm, and –1.8% in the year to March 2014.

M&S’s operating margin has also been trending lower too, 6.2% in 2013, and 7% a year after, with 6.5% in the last financial year.

Even so, despite misgivings, to be fair, we need to return our thinking to M&S’s relative strength in food.

With the broader retail sector beyond non-discretionary groceries–for example, Next Plc.–showing signs of contagion from challenges that have hit major grocers such as Tesco, any sign of differentiation in either non-food, or food looks set to be lauded by investors.

The comparison of M&S with Next is a telling one.

In stock terms, for much of this year, their fortunes have diverged.

Until this morning, despite its weather-related issues, Next stock was up 20% for the year, whilst that of its arch rival in high street clothing, M&S was down almost 18%.

Given M&S has demonstrated at least its ability to hold steady in food amid the grocery sector downturn, and Next’s absence from that sector, the reversal in market ratings for this pair begins to make (a little) sense.

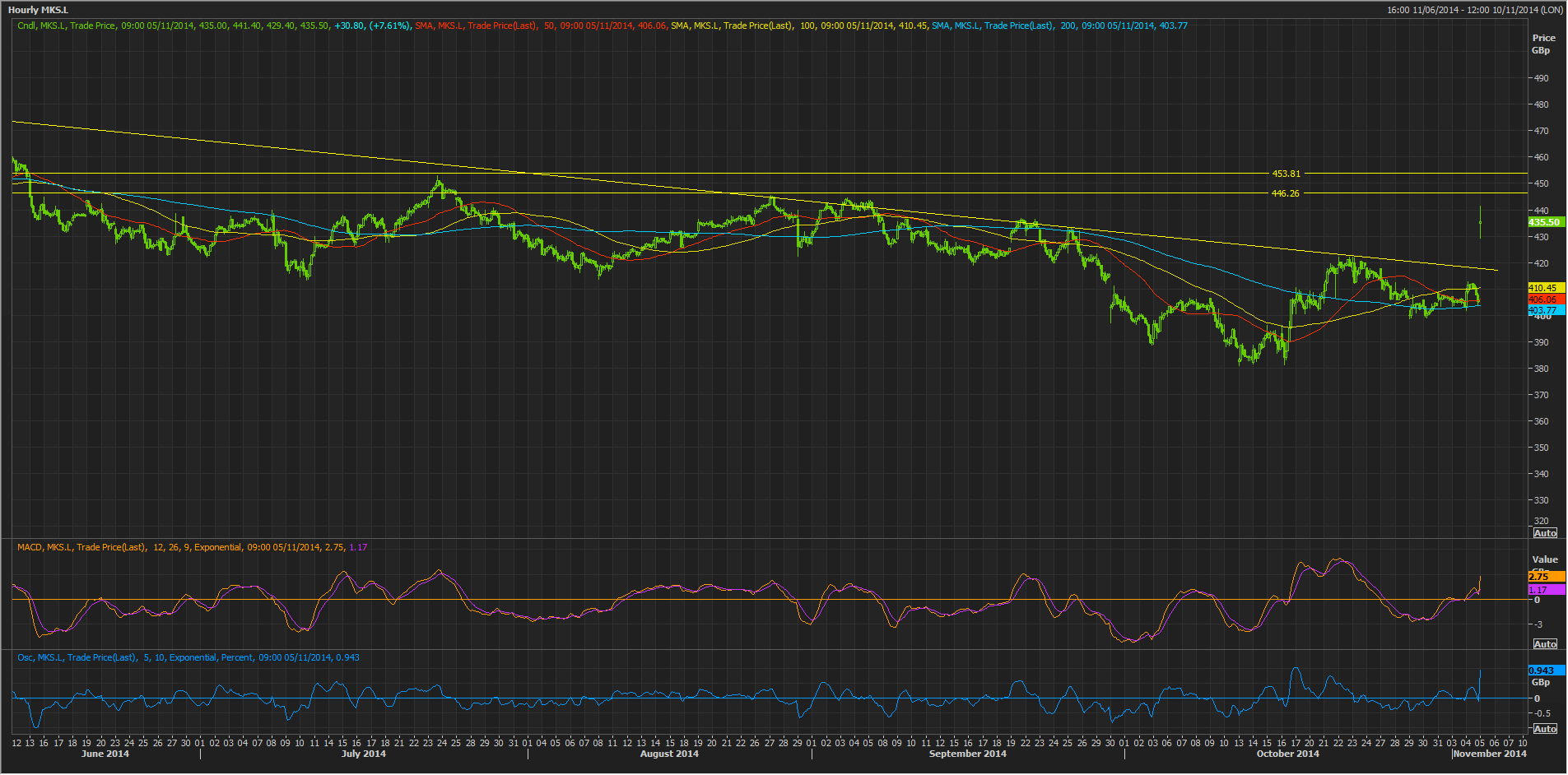

Momentum in M&S stocks looks strong at the moment.

We still consider it very likely this morning’s stock jump will moderate, in the face of hurdles marked on the chart below.

The stock must overcome these if it’s to confirm it has broken the downtrend that commenced in February. Today’s low so far is 429p.