Marks amp Spencer shares peak as CEO honeymoon fades

Marks & Spencer’s new CEO is making good use of his ‘honeymoon’ (with investors). Worries at the iconic retailer which reported a second bleak […]

Marks & Spencer’s new CEO is making good use of his ‘honeymoon’ (with investors). Worries at the iconic retailer which reported a second bleak […]

Marks & Spencer’s new CEO is making good use of his ‘honeymoon’ (with investors).

Worries at the iconic retailer which reported a second bleak Christmas in a row in January didn’t ease much in the March quarter.

A 20th sales slide out of 21 at the softly re-branded ‘Clothing & Homeware’ division (still formally known as ‘General Merchandise’) confirmed it is Marks’ Last Chance Saloon Dept., if the group wishes to survive in its current form.

But Steve Rowe, an M&S ‘lifer’, if 26-years equates to that term, was still more candid than most CEOs tend to be, including him, probably; given a few years, or perhaps even months at the helm.

“Although the sales decline in Clothing and Home was lower than last quarter, our performance remains unsatisfactory and there is still more we need to do,” he said.

“Let me be really clear: this performance was not good enough.”

Quite what more can be done remains open to question, after his predecessor, Marc Bolland pumped billions of pounds over five years into Gen. Merch. only to receive negative returns, in terms of sales, though gross margins fared better.

On the other hand it is Rowe to whom the bulk of Marks’ sector-leading food division performance over the last few years can be attributed.

Whilst the likes of Sainsbury’s, Tesco, Morrisons and others were beginning to wonder whether there was a future for their type of ‘grocery’ business, Rowe, who began heading up food in 2012, oversaw 25 consecutive quarters of like-for-like food sales growth.

The question is then, is whether he has met his match in Gen. Merch., which will be no less daunting a proposition to fix, even with a cutesy name.

Whilst opportunism is not unfamiliar in the utterances of Next’s senior management—OK, yes we do mean CEO Simon Wolfson, who has been lording it over retailing for decades—the group’s warning last month that 2016 could be its toughest year since 2008 was read by investors as just as much a warning for rival M&S.

The iconic British retailer’s shares, still ailing after the Christmas let-down, plunged to 18-month lows straight after Wolfson’s comments in March, including his view that “The outlook for consumer spending does not look as benign as it was at this time last year.”

Again Next, which for several of the last few years blamed dwindling sales growth on the British weather, before a relatively temperate 2015 put a stop to that, might not be the most reliable source on the retail outlook.

However, Wolfson undoubtedly has a point.

Thursday’s strong general retail sector bounce, in the wake of Marks’ not-as-shabby-as-expected figures—Dunelm Group (+3.6%) Carpetright (+2.7%), Next (1.7%), Home Retail (+1.3%) et al—suggested investor relief as well as illustrating the concerns Next had flagged.

Conversely, the advance in favour seen by ‘purer’ homeware purveyors like Dunelm—which has inched 8.4% higher this year vs. M&S’ 2% fall—is another dimension of the challenge M&S faces. Rivals are beginning to look like they can do better, at what it used to do well.

Don’t forget the UK’s best-performing retail stock so far in 2016, Tesco, which has risen 27% year-to-date, partly on the supermarket’s increasingly refined incursions beyond fresh food.

Sainsbury’s, the current supermarket leader in terms of sales growth, may not be far behind.

Its plans to ‘generalise’ its offering hand-in-hand with leading-edge store space ‘optimisation’, are coming to fruition with the Home Retail Group buy.

On the plus side, Marks can boast consistent gross margin wins, whilst the likes of Next cannot.

M&S’s latest was a guidance upgrade on Thursday which firmed expectations for a top-end-of-forecasts margin rise in Clothing & Homeware itself.

That ought to cause rivals some unease, as should progress at M&S’ food business despite the stall in Q4.

The flat like-for-like result may have ended a 25 straight quarter run of growth, but it still ‘trounced’ Big UK Grocery by 3.5 percentage points, taking market share to a record 4.3%.

Take that Tesco.

Well, Tesco CEO Lewis & Co. might do just that.

Which is one of the key reasons why from a technical basis, we were somewhat cool on M&S’s rally on Thursday.

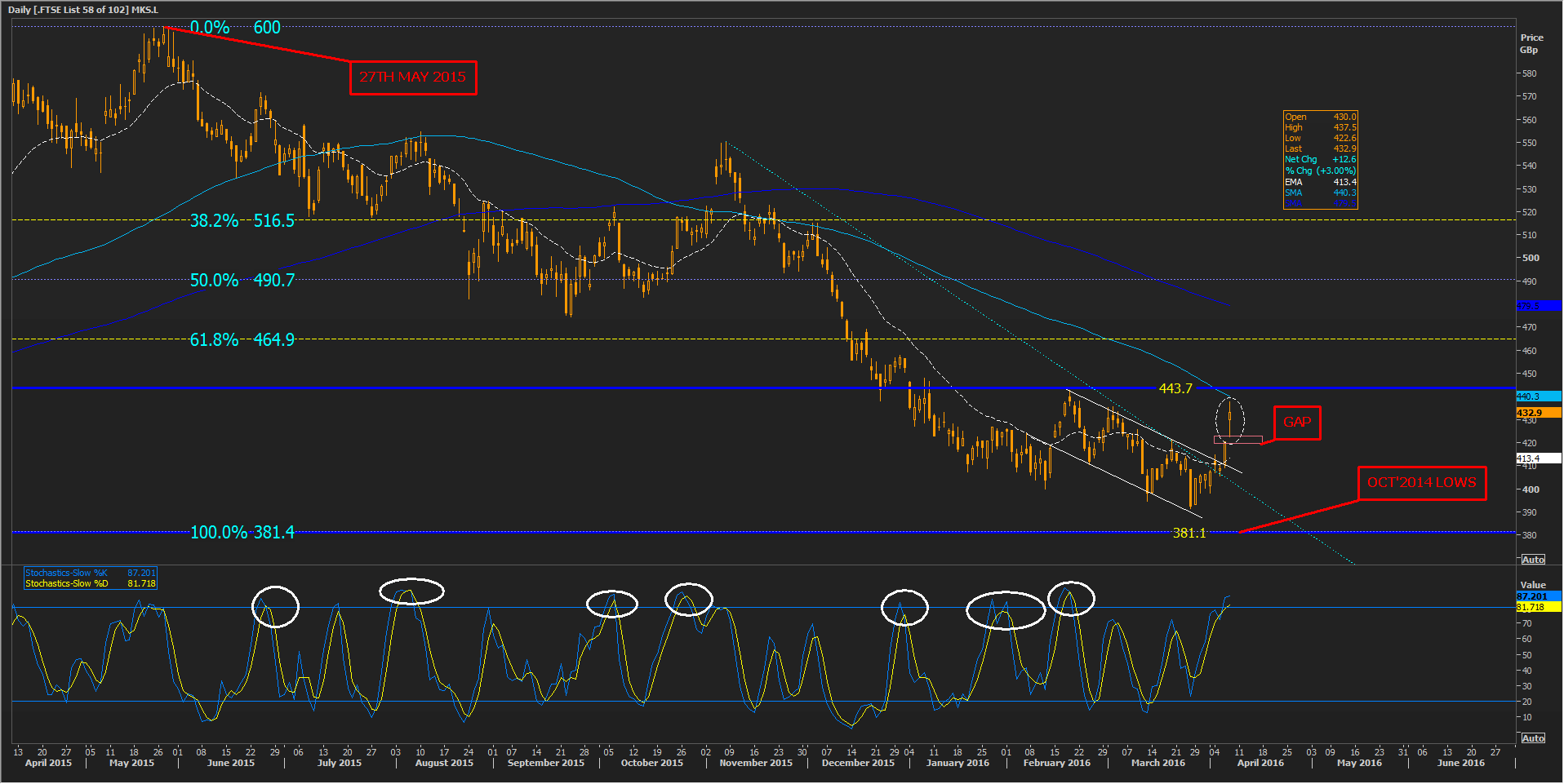

Please click image to enlarge

MKS’ 10.7% upswing off from 2016 lows seen in March; post-Wolfson, looks almost parabolic; with Thursday’s curiously lengthy and thin candle shooting for but falling short of the declining 100-day moving average (light blue).

Also overhead is 443.7p; worrisome for sellers throughout January last year, and probably equally so for buyers in the near term.

A breach of the latter two thresholds in the near-to-medium term ought to be a fair enough sign that the stock would be ready to resume outperformance.

If the stock manages to stay above a sharply descending trend in place since November, that would also strengthen its prospects.

Finally, as we know momentum (see Slow Stochastic sub-chart) can stay ‘overbought’ for ages, for many stocks, but MKS hasn’t been one of them over the last several months.

The stock’s reversals have been quite orderly.

If Rowe’s honeymoon phase really is drawing to an end, further share slippage may be seen soon.

Marks & Spencer’s finals are due on 25th May.