M amp S and Tesco share moves overdue and overcooked

If you blinked, you may have missed one of the biggest retail stock rallies this spring, though perhaps you were hiding under a rock if […]

If you blinked, you may have missed one of the biggest retail stock rallies this spring, though perhaps you were hiding under a rock if […]

Marks & Spencer first; where a rout of more than 10% on Wednesday raised some eyebrows in The City.

After all, currency pressures which M&S said would help cap gross margin gains in its key Clothing & Home division to 50-100 basis points (after +245bps in 2015/16) have been well flagged.

And the profit guidance cut revealed on Wednesday would logically have gone hand-in-hand with whatever turnaround was planned (though the extent of the downgrade—c.10%—was towards the most negative end of assessments.)

Furthermore, it’s difficult to see the turnaround plan announced on Wednesday by M&S’s recently installed CEO, Steve Rowe, as anything worse than sensible.

The crux of investor disquiet was probably Rowe’s caution that it would take time for customers to notice improved product offerings, refined customer service, ditched promos and new “everyday” price cuts.

After six years of unsuccessful revamps by Rowe’s predecessor Marc Bolland, disappointment over another long wait was partly understandable.

But Rowe was certainly being realistic in the face of external threats and internal challenges, the former partly represented by Next, Primark and ASOS, targeting the under-35s, and the latter in the shape of increased store staffing, investment in price and scrapped promos, all before widely suspected structural issues in Clothing & Home are identified and fixed.

On that basis, perhaps M&S’s 10%-plus tumble on Wednesday was not so much overdone as overdue.

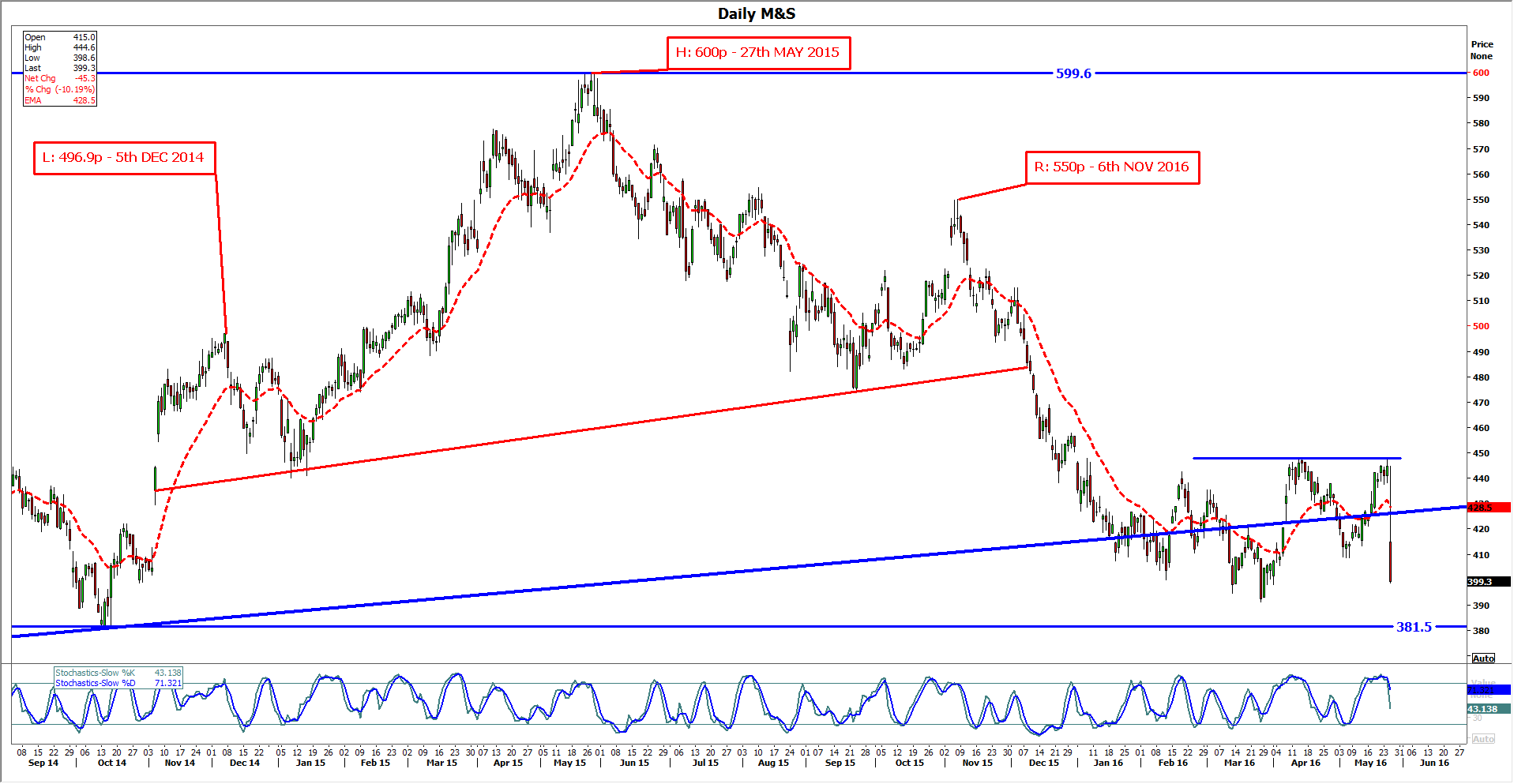

From a technical basis dashed hopes—even those lowered further by the last few fallow years—were evident from the well and truly busted ascending trend (blue line) that has withstood all tests since December 2011.

What’s more, albeit choppy, and therefore potentially unreliable, a traceable head-and-shoulders pattern from November 2014 completing a little over a year later casts a theoretical target as low as 371p for the shares: top to neckline minus the low at H&S completion, or 485.5p x 2 – 600p.

This suggests a further 28p loss on top of the 10.2% fall on the day to 399p, particularly with stochastic momentum pointing sharply lower.

On the other hand, caution looks preferable to chasing a strategy to its theoretical conclusion. Selling here would look more like a bet that the October 2014 low at 381.5 would be broken sustainably. Slim risk/reward right now, though on the other hand it will probably ‘take some time’ before M&S becomes an out an out favourite for many, setting c.450p as a likely cap for the medium term at least.

Please click image to enlarge

As for shares of UK Supermarket No.1, Tesco took the FTSE 100 top spot on Tuesday, albeit fleetingly. The stock closed with a 6.8% lead, though gave 2.3% back on Wednesday, leaving many none the wiser.

Before we get into probable triggers it’s worth reminding ourselves that around two years after Britain’s biggest grocers dragged themselves off the floor at the depths of their crisis, the Big 4 remain among the ‘biggest shorts’ among blue-chips. The 1.41% of Tesco’s free float on loan according to the FCA’s latest update may not sound like much. But relatively speaking, it is, for a large cap stock, and well above long-term borrowed rates in the name.

Which is to say, bear in mind that persistent shorts tend to increase stock price volatility—a short ‘scare’ (and squeeze) like Tuesday night’s, can have eye-catching results, which may or may not signify much for medium term price outlook.

And apart from Tesco’s long-standing aggregate short, another market structural factor which influenced Tuesday’s late rally was reportedly a large order filled during the closing auction.

All that having been said absolute potential triggers were interesting and quite plausible.

A report by bulge-bracket US brokerage Bernstein was cited. The broker noted that both CEO Dave Lewis and CFO Alan Stewart were awarded almost 100% of their potential annual bonuses in Tesco’s financial year ending in March. (In the CEO’s case that equated to £4.6m).

Bernstein chose to interpret the pay-outs as justified. It noted that the group had swung from an EBIT loss and contracting underlying sales at the end of 2014 into profit and a trimmed key sales fall in 2015/16.

Bernstein pointed out that current City/Wall St. consensus forecasts only equate to cash flow of about £8.3bn, a scenario under which Messrs Lewis & Stewart would get zilch.

That raised the question of whether the market’s average cash flow forecast was a credible one. Many investors answered the question on Tuesday afternoon by adding stock.

Their conclusion clearly has some merit, though of course, it also depends on circular thinking for which there is no corroboration, apart from the new top brass’s short record in post.

Risks to the bull case are pretty obvious in the retail sector by now—Lewis himself characterised business conditions as “challenging, deflationary and uncertain” when commenting on Tesco’s finals in April.

These cautions need to be set alongside good progress by Tesco’s new brooms so far, and the fact that Return on Equity is widely forecast to triple to 10% by the end of 2018.

Perhaps it’s no coincidence that the date coheres with when Lewis will be eligible to cash in the portion of his salary that will be paid in shares.

With shares just 30 pence from the almost 19-year lows grazed in January, internal expectations may already have eclipsed much external scepticism.