Kingfisher still struggles in France

Kingfisher has again been wrong-footed in France. The owner of the B&Q DIY consumer chain and Screwfix trade supplier in the UK, said a […]

Kingfisher has again been wrong-footed in France. The owner of the B&Q DIY consumer chain and Screwfix trade supplier in the UK, said a […]

Kingfisher has again been wrong-footed in France.

The owner of the B&Q DIY consumer chain and Screwfix trade supplier in the UK, said a near-17% third-quarter slide in retail profit to £225m was particularly down to the soft market in France, a region that has been at the root of weak figures from the group for much of the year.

There was a moderate adverse foreign exchange translation effect of £13m, but the poor results can’t entirely be attributed to that.

In France, where the group owns the Castorama, Brico Depot and Mr Bricolage chains, retail profit slumped 14.3% at actual exchange rates and would still be 8.4% lower with profit calculated as if exchange rates didn’t change during the period.

As per second-quarter results in July, questions will inevitably be raised about how France–which like the much of the rest of Europe, has been in the doldrums for years—could repeatedly stymie the group’s performance.

Like for like sales in France, the group’s largest market fell 4% whilst the average forecasts were seeing a fall of 3.6%.

On a better note, UK and Ireland LFLs beat forecasts with a 2.6% rise compared with 2.5% expected.

There had been hope that with the newly appointed French CEO, Veronique Laury, who was head of Kingfisher’s French businesses, some improvements would be seen.

In fact Ms Laury doesn’t formally take over until 8th December, with today’s results the last to be presented by her predecessor, Ian Cheshire.

Whilst he has failed to tackle the European conundrum of low growth versus opportunities of potential scale, net income after tax galloped under his 14-year tenure, even though disappointed in recent years

The share price has essentially doubled during his tenure, and he has turned a billion pound net debt to net cash of £238m.

Going forward, I note not only does KGF remain cautious on the outlook, especially in France, it says it is continuing to focus on margin and cost initiatives. That seems at least partly a reference to ‘investment in margin’ –AKA price cuts.

Hand in hand with the poor European outlook and the balance for the group overall, plus a disappointing gross margin performance in both France and Poland, hopes of the near-term sustainable turnaround that had been raised at the half-year stage, are very likely to be dashed.

Having said that, I think the headline miss is too negligible to warrant material downgrades on the full-year forecasts the market has.

That’s not to say the FY outcome could not be even weaker than already pessimistic expectations. Kingfisher made it clear today that there will be no quick comeback, on a group basis.

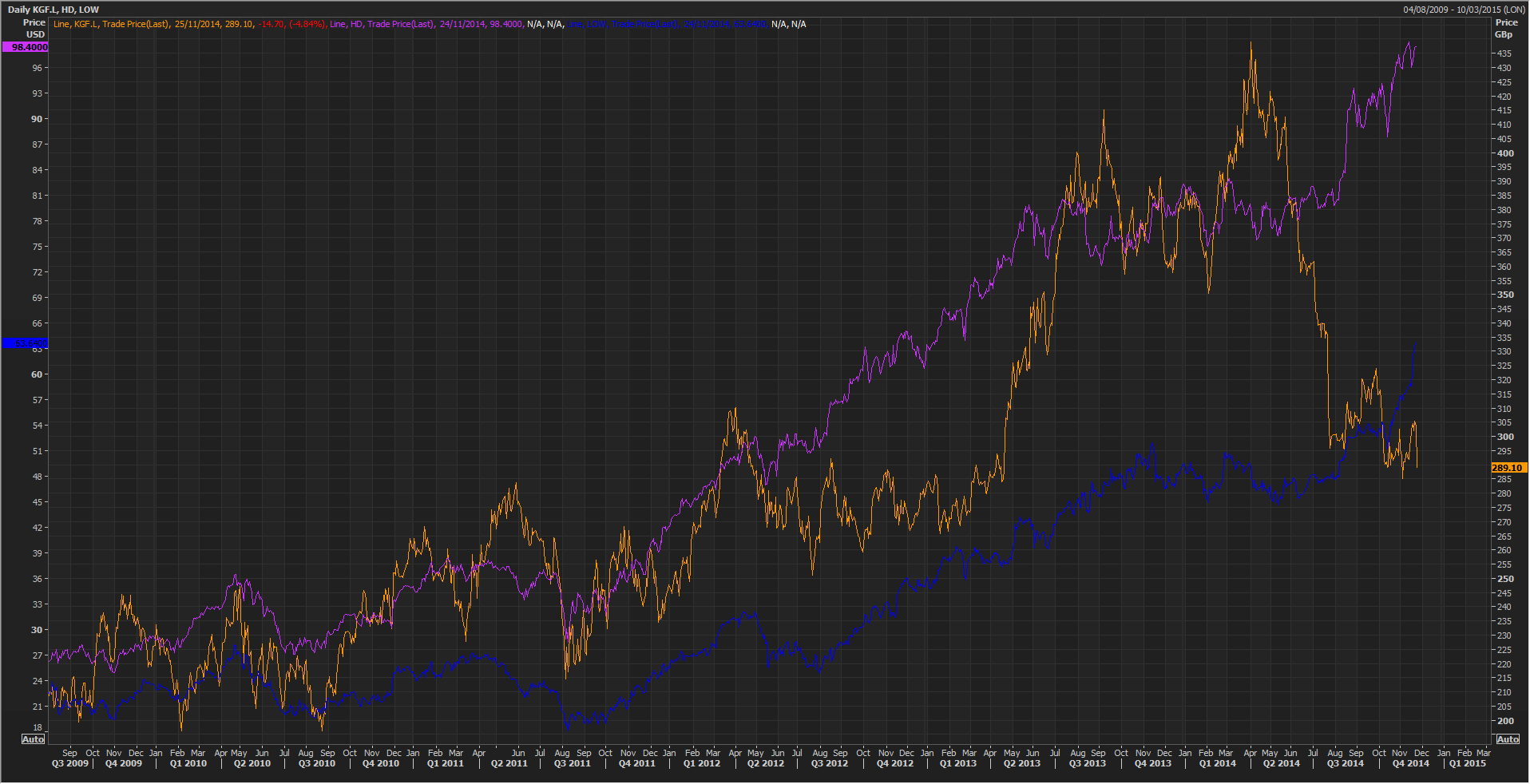

All in all, Kingfisher’s, No. 3 position in the DIY stakes, behind US groups Lowe’s Companies Inc. and Home Depot, continues to look somewhat in question, its shares falling off a peak of 439.08p on 3rd April, whilst Lowe’s continue their steady advance.

Continued flaccidity in earnings from Kingfisher are likely to widen the discount compared to its close peers even more.

Orange: Kingfisher

Purple: Home Depot

Blue: Lowe’s

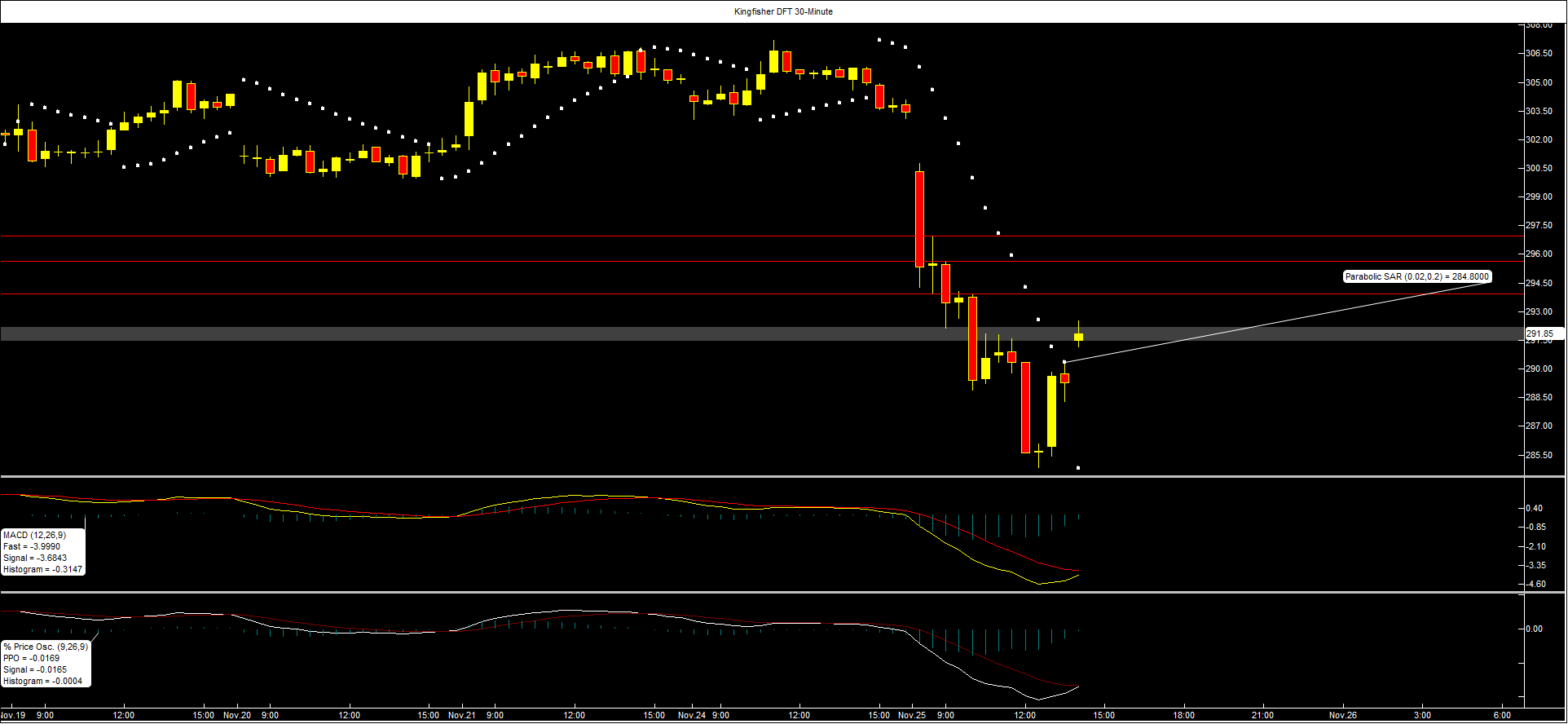

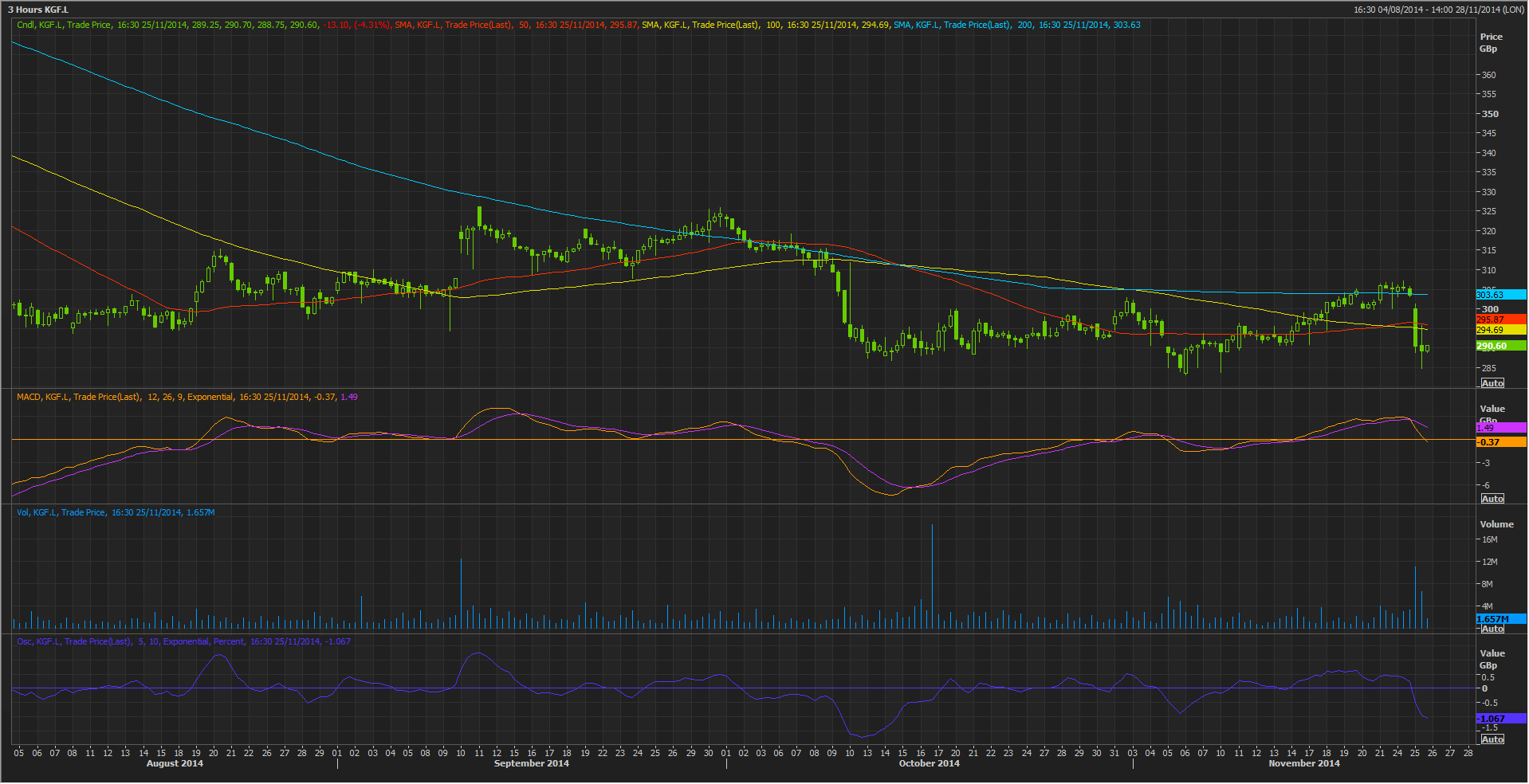

Share price upside of course looks fairly hopeless for now. The picture using three-hourly intervals shows unmistakeable inversion and slide by the percentage oscillator and the Moving Average Convergence systems.

Half-hourly trading in City Index’s Kingfisher Daily Funded Trade is making a somewhat unconvincing attempt to regain the upside; at the time of writing though any of the half hourly down steps seen today could cap this.