Germany 8217 s DAX is Britain 8217 s Brexit Index

Traders wishing to express a view on the stock market impact of Britain’s ‘in/out’ referendum, face a dilemma. The FTSE 100 would appear to be […]

Traders wishing to express a view on the stock market impact of Britain’s ‘in/out’ referendum, face a dilemma. The FTSE 100 would appear to be […]

Traders wishing to express a view on the stock market impact of Britain’s ‘in/out’ referendum, face a dilemma.

The FTSE 100 would appear to be the obvious choice among stock market indices given numerous ways to trade it. But it’s widely known the benchmark is only loosely connected to Britain. FTSE 100 companies generated only about 22% of their revenues in the UK last year, according to Thomson Reuters. Broader indices, like the FTSE 350, for instance, will have more sales exposure to the UK. But who trades the FTSE 350? Only a tiny fraction of City Index clients placed FTSE 350 (or FTSE 250) trades over the last year. ‘Economically British’ UK indices are a minority pursuit. It’s the same at the ‘professional’ end of markets too. The biggest daily volume so far this year in Intercontinental Exchange’s FTSE 250 index futures was a skimpy 5,184 on 16th March compared to more than 234,000 in ICE’s FTSE 100 future on the same day.

So what are the alternatives? On the face of it, opting for a broad European index has some logic. The EU on aggregate is the UK’s second-largest ‘true’ trading region (balancing imports with exports) after the United States, and the Office for National Statistics this week announced a record deficit with the EU for the third month in a row, backing views that Europe has just as much to lose in a Brexit as the UK, perhaps more. On that basis, the Euro STOXX 50 index of Eurozone blue-chips could be a reasonable UK-EU proxy. Furthermore, Euro STOXX futures liquidity is similar to levels seen in many mid-cap stocks. Their highest daily volume so far this year was around 3.3 million on 16th March, living up to the exchange’s claim that the future is “the most liquid derivatives instrument in Europe.”

However, transaction and clearing charges for futures tend to make them the least cost-effective way to trade indices for all but the deepest-pocketed individuals and institutions. At the same time, given that the bulk of UK-EU trade is actually with Germany (accounting for about 15% of all UK imports in 2015) Germany’s DAX 30 index might be a better UK-EU proxy. It comes in slightly below the Europe-wide gauge in our ‘futures contract’ test (highest daily volume so far in 2016: 234,040 on 10th March). But demand for the DAX among ‘ordinary’ traders is consistently higher than for any other equity index.

There are obvious problems with treating the DAX or Euro STOXX as straight ‘In/Out’ proxies.However, perhaps we can assume that non-Brexit related ‘noise’ will play second fiddle to referendum risks for the EU in the run-up to the vote, especially given that all large European markets have underperformed major FTSE indices by several percentage points so far this year.

Such assumptions will form the basic rationale of the DAX trader’s strategy around the vote. Bears might decide that the index’s underperformance of its UK counterpart suggests its progress will remain limited until the overhanging ‘risk event’ (the referendum) has passed. Bears will therefore be on the lookout for opportunities to get short of the DAX, particularly whenever it rises to important resistance.

Conversely, DAX bulls may decide that increasing market confidence that Brexit is unlikely to occur provides opportunities to get long, especially whenever the index reaches identifiable support.

Precise strategies will depend on the trader’s risk tolerance, specific aims, and other factors.

For instance, the DAX, like any index can be deployed as a ‘hedge’ to protect positions in single equities or, for outright speculation. It’s worth noting though that ratio spreads—say between the DAX and the FTSE 350—would be prone to cyclicality, reducing the reliability of their signals.

Either way, equity index traders will be confronted with an important wider issue right now: volatility has drained out of equities and into foreign exchange markets, leaving European indices stuck in tight ranges for months. Note ‘implied volatility’ in sterling—strongly tied to the cost of bearish option trades—has been on the rise since the end of last month, having fallen a little from multi-year peaks in mid-April.

In our view, the disparity presents both potential opportunities and risks for those trading less excitable markets, like indices. On the one hand a return to more ‘normal’ volatility is unlikely before 23rd of June, but in theory could occur at any time ahead of the vote, or after, regardless of the outcome. On the other hand, an apparent lack of stock market zing could be masking complacency and mispricing risk, with painful consequences for traders who have not used tight stops. Current re-loading of implied vol. in FX suggests speculators and corporate hedgers smell enough Brexit risk to shell out for pricey options, regardless of bookies odds and polls giving the ‘remain’ camp the edge.

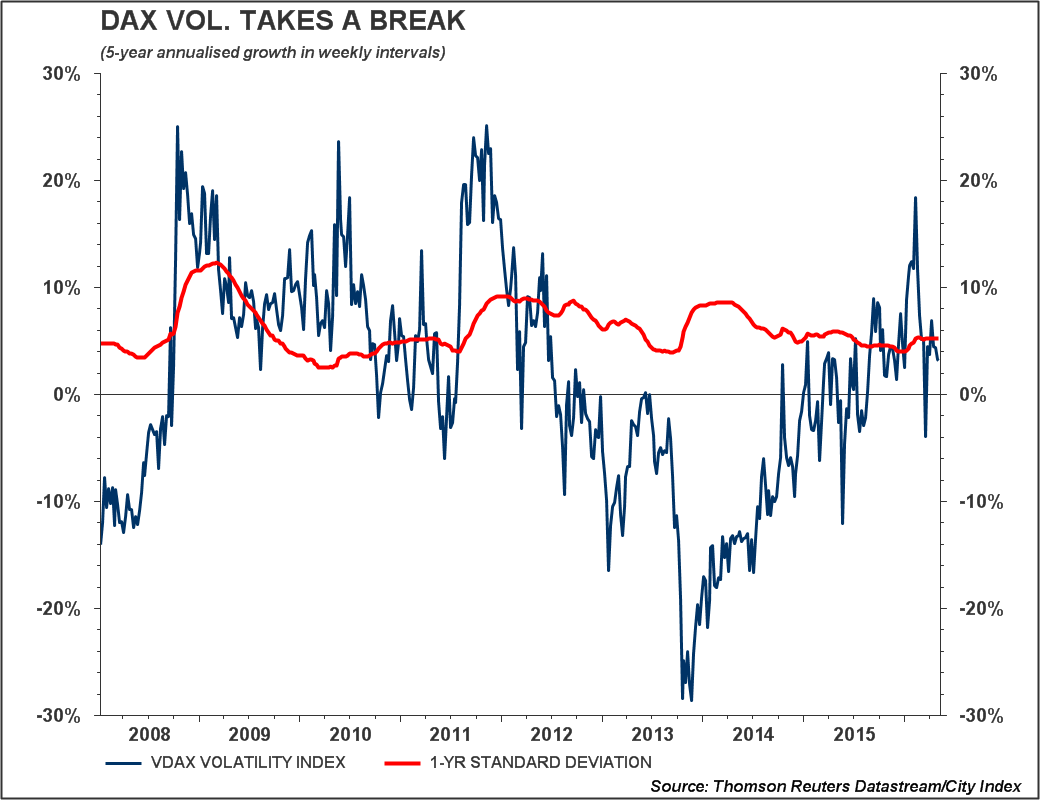

In comparison, DAX trading looks quite relaxed. Deutsche Boerse’s VDAX Volatility Index shows 30-day DAX options vol. is currently below its 5-year trend (see chart below). Like its UK counterpart, Germany’s stock market is quiet, perhaps too quiet.

Figure 1 – VDAX Implied Volatility Index: 5-year growth rates annualised in weekly intervals

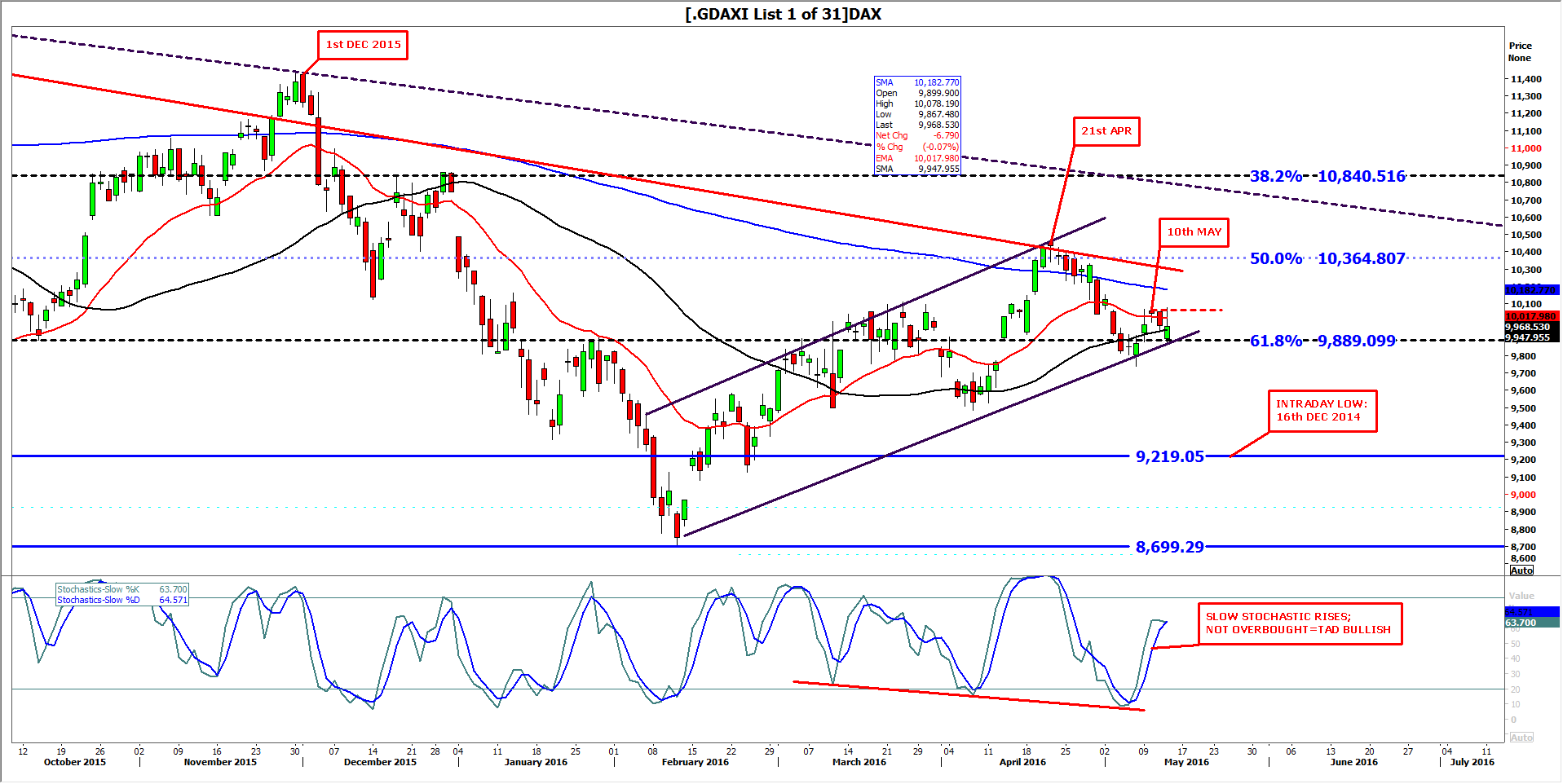

On a technical basis, the scene looks set for the DAX to remain capped by April’s 10340-10474 highs until as late as 23rd June and perhaps beyond, depending on the referendum outcome. The DAX has risen more than 13% from February lows. But despite my best efforts to draw a clean channel, daily peaks have been erratic. In other words, the index has frequently violated the upper boundary of the channel, suggesting some instability despite the low volatility we mentioned above. This air of incoherence, is corroborated by the DAX’s erratic battle with the level of 9890, close to an important Fibonacci interval (61.8%) based on the index’s rise from October 2014 lows to all-time highs in April 2015.

Having last week re-conquered the line for a fourth time since falling below it in August 2015 the index has been testing it anew this week. Although a potentially bearish ‘spinning top’ candle on 10th May might have signified indecision, it was not placed perfectly enough to confirm likely strong selling. (In theory the candle would need to be at the top of an uptrend to be definitively bearish.) Even so, price action a day later—denoted by the shape and size of the next candle—suggested a significant number of trading stops were placed at levels equivalent to Tuesday’s best volume-weighted prices (see short dotted red line).

For sellers, the move played out with much more emphatic price action a day later. Whilst the DAX subsequently bounced on Thursday, likely short-term resistance (that dotted red line again) was corroborated by the DAX testing the level with a peek above it by a few points, before retreating below. Meagre outperformance on Thursday of Wednesday’s highs should also add to the negative balance. Higher still, the 200-day moving average (MA) in dark blue, and what could be the beginning of strong descending trends off the historic peak in April 2015, present further obstacles. (The higher black dotted trend line may have more weight since it remained intact whilst the lower red trend line was broken in late November/December 2015, though that now looks like a false break).

All that above said, momentum, at least judged by the Slow Stochastic sub-chart, doesn’t look like it is playing ball. The indicator is rallying and has quite a bit of room topside before it could be called overbought. But even here, there is ambiguity. Mild but unmistakeable divergence has been visible in the indicator since late February. The falling slope (see red line) may be too gentle to truly qualify as bearish divergence, but it does muddy the picture. Moving back to the price chart, obviously, a break below the lower channel trend line in the near term would clarify things, with circa 9650 likely to be seen in fairly short order under that scenario. But only a rise above 10064 in the next few sessions would be likely to open the way to the higher reference points mentioned above, and a slightly longer term target c. 10300. In conclusion, the picture is inconclusive. The DAX isn’t going gangbusters, but it’s also not ailing badly. Actually, that balance seems quite fitting for a German index facing a headwind from a referendum in Britain.

Figure 2 – DAX 30 Index daily chart