Flybe shares nosedive as rivals rise on cheap oil

Shares of Flybe Group, the small UK-based low-cost airline were the worst-performers on London’s stock exchange today after its comments on the outlook were interpreted […]

Shares of Flybe Group, the small UK-based low-cost airline were the worst-performers on London’s stock exchange today after its comments on the outlook were interpreted […]

Shares of Flybe Group, the small UK-based low-cost airline were the worst-performers on London’s stock exchange today after its comments on the outlook were interpreted as a profit warning.

The firm said it expected to break even before tax in its financial year ending in March 2015, despite a fall in third-quarter revenue.

Investors seemed disappointed though, apparently expecting— judging by forecasts compiled by Thomson Reuters before today’s trading update—net profit for the current year to be at least £3.48m, after just £200,000 the year before.

Having undergone a severe cost-cutting exercise Flybe managed to report its first pre-tax profit in four years in the year that ended in March 2014.

Some of the economies the carrier was forced to make in order to avoid what appeared to be a risk of bankruptcy included the sale of highly-prized airport slots, drastic job cuts and grounding parts of its fleet.

Whilst these measures worked to the extent that it made a slim profit for 2014, Flybe was back in the red in the first-half of the current year, amid unforeseen costs and a charge for its decision to break up a joint venture with Finnair.

The full-year forecast on Monday followed a 3.8% drop in passenger revenue in the final three months of 2014 to £126.8m amid competition on some new London City airport routes.

“We believe that this competitive pressure will extend the period of time that these routes take to reach maturity and deliver the full contribution we expect,” Flybe said.

Excluding costs relating to grounded Embraer E195 aircrafts and the impact of some loan revaluations, Flybe would break even before tax in the year ending this March.

In other words, it now expects to post a loss after tax and costs.

Investor disappointment undoubtedly also takes into account that Flybe won’t see any benefit from the collapse of crude oil prices to multi-year lows.

Flybe indicated its current hedging cycle would not enable it to take advantage of lower fuel prices before 2016/17.

Flybe is a minnow in a sector that’s rapidly being rearranged to accommodate what look sets to be long-term switches in pricing.

Its sub-£200m market cap signifies its obvious disadvantages against its giant, diversified, dividend-paying UK rivals worth billions.

Flybe shares look priced for growth, but its trailing price/earnings ratio shows a contraction of more than 200 times in 12 months, whilst on a forward basis the sector average is far better at 12.9 versus Flybe’s 9 times.

Its closest listed rival could be Dart Group Plc., whose market value is £405.4m and at least yields 1% whilst largely matching the average forward P/E of UK listed carriers.

Flybe has done no better against the wider sector over the past year.

The stock was left with a 17% lag after the 52 weeks since 23rd January 2014, whilst the FTSE 350 Travel & Leisure index gained almost the same amount during that period.

Ryanair shares led the sector with a 40% rise, and easyJet is still a net 10% up over the same time period, despite retreating from all-time highs in April last year.

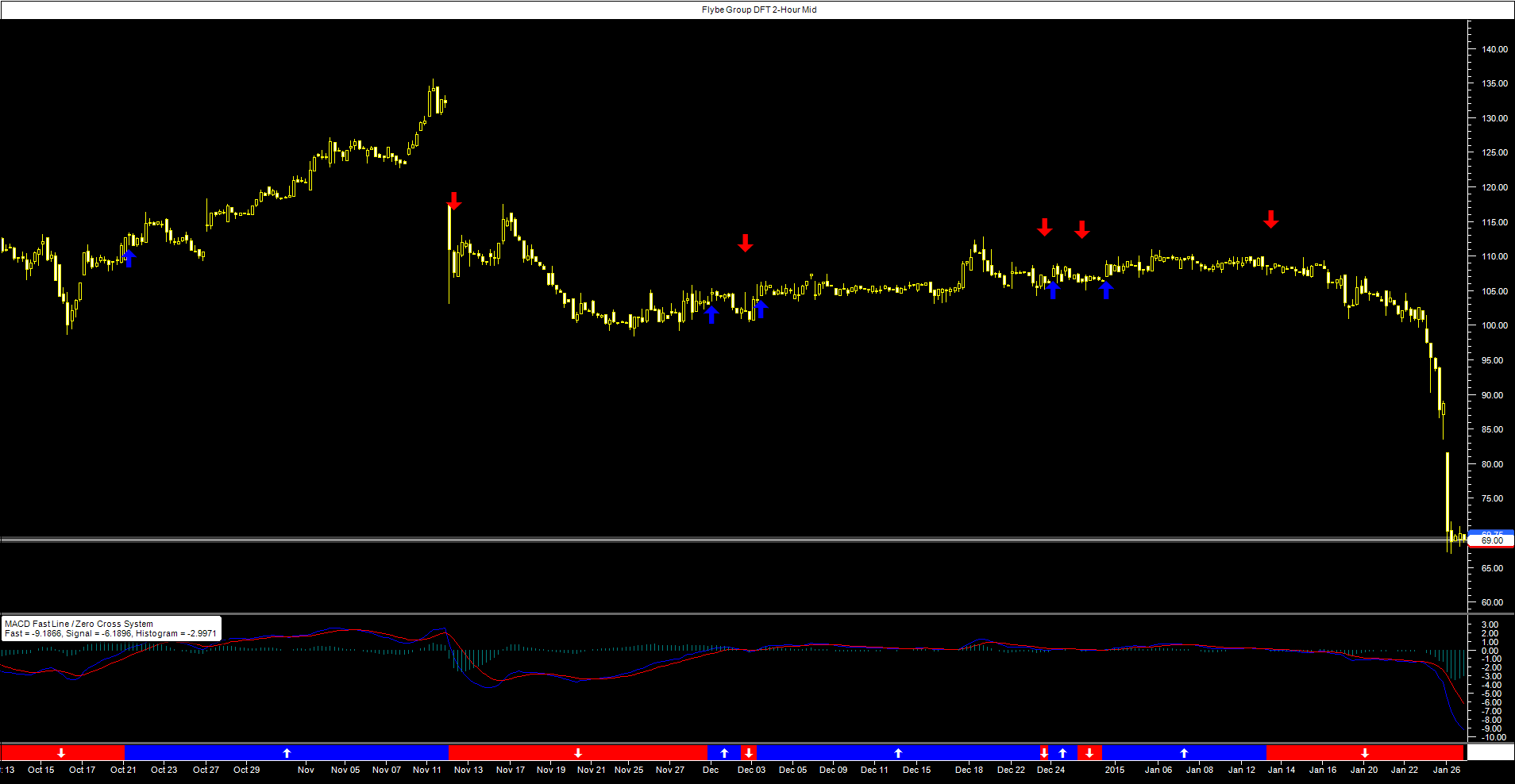

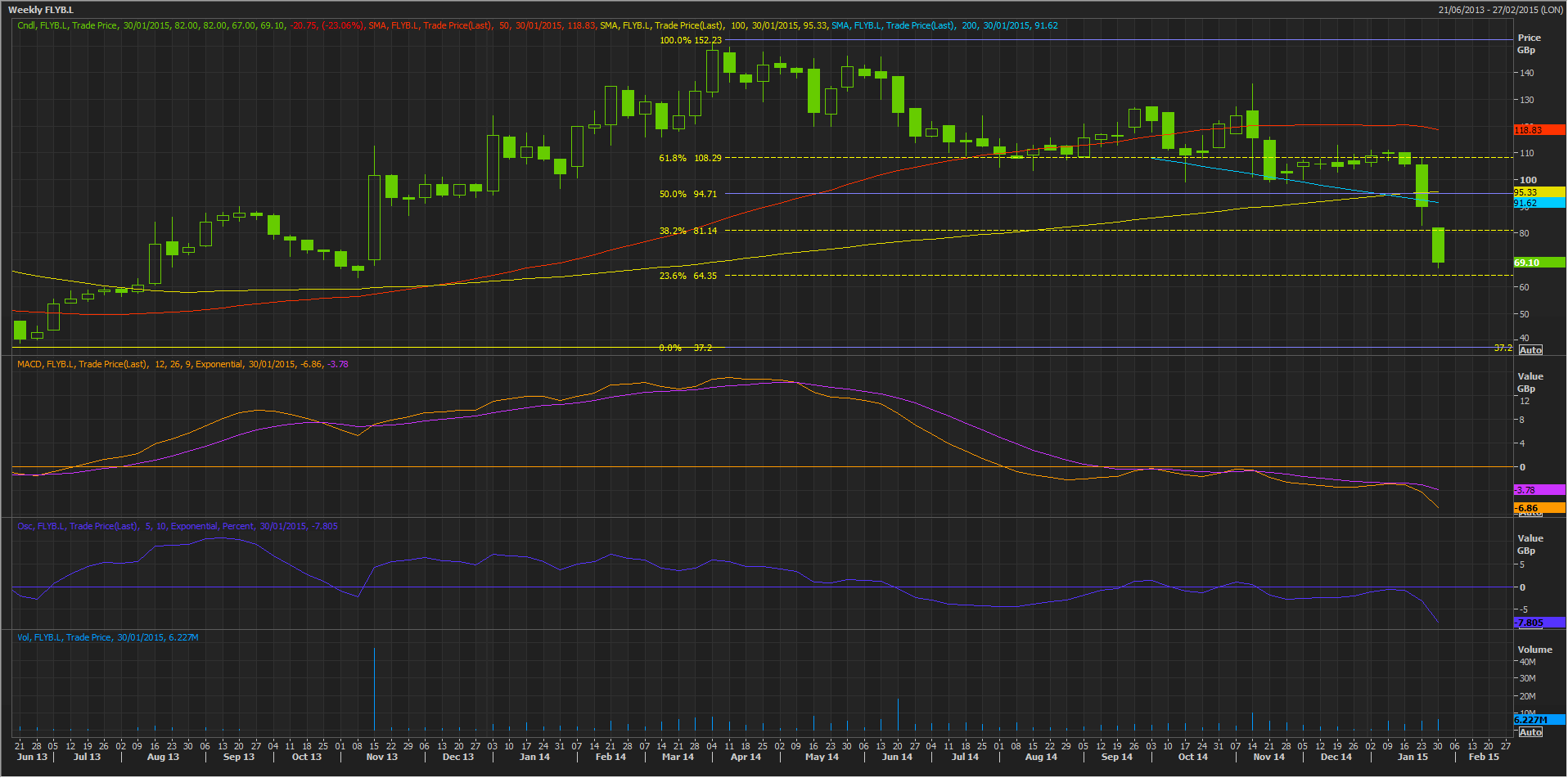

Flybe shares have been a buy to regret since their flotation above 300p in 2010.

It’s been downhill all the way, to all-time lows below 40p, last seen early in 2013.

Off that floor, the current price around 68p is nudging a 23.6% retracement marker.

Traders know this Fibonacci level tends to be amongst the weakest in the series.

It may not provide much protection against a return to the stock’s nadir, even if overstretched selling evidently attracted some marginal buying as Monday wore on.