Brexit risks for supermarkets point to Morrisons

Sainsbury’s sales offer the freshest look at the impact of Brexit concerns on supermarkets, and Morrisons looks most vulnerable.

Sainsbury’s sales offer the freshest look at the impact of Brexit concerns on supermarkets, and Morrisons looks most vulnerable.

As the current leader in terms of growth (albeit modest) Sainsbury’s outlook should be instructive. UK grocer No.2, by market share, repeated its caution from earlier in the year that business “remains challenging”, with prices still deflationary.

As the best-performing supermarket over the last two years, with more frequent market share gains than rivals, Sainsbury’s seeing more trouble ahead is a worry for the battered sector.

Particularly for still fragile groups like Morrisons and even for market leader Tesco, where four months of improving sales came to an abrupt halt in May, according to independent researcher Kantar.

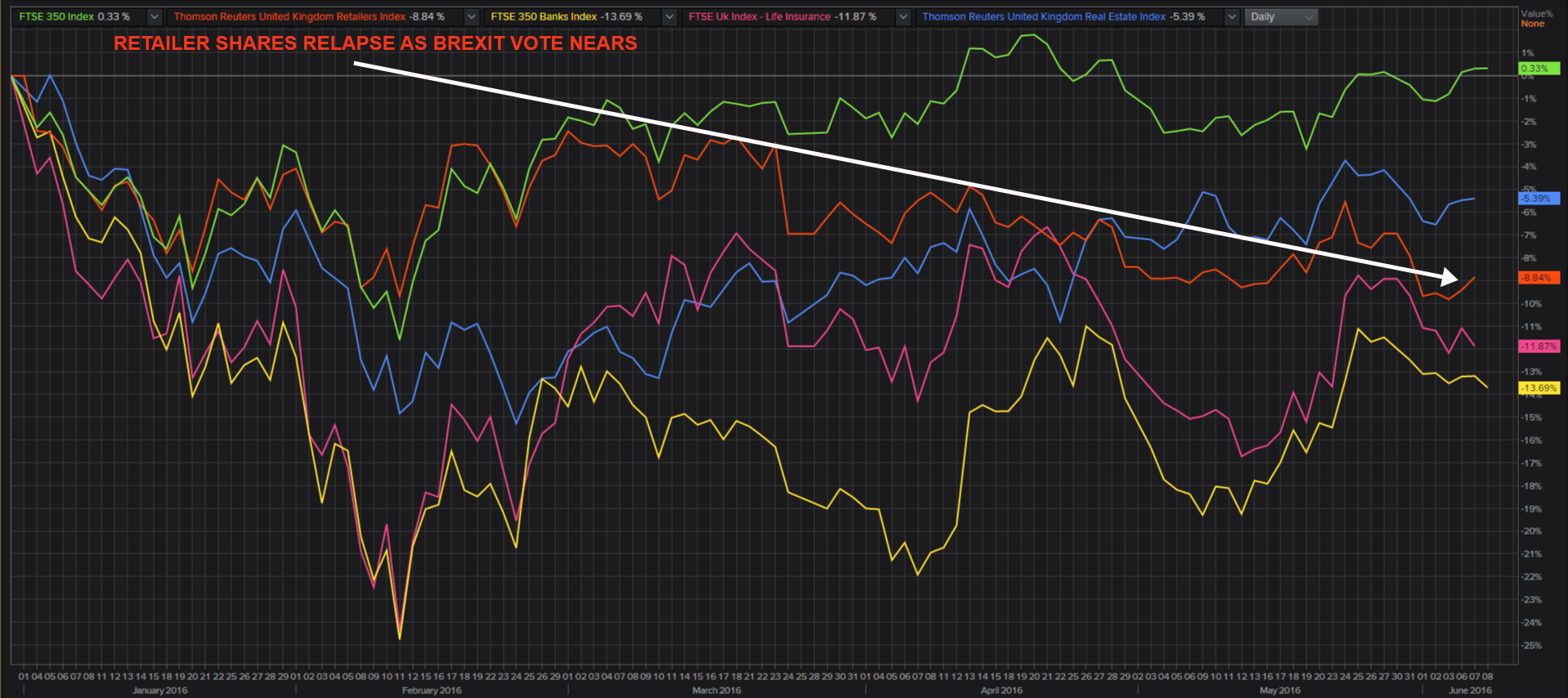

Sterling jitters this week from the Leave campaign gaining ground read directly across to Sainsbury’s, Tesco and Morrisons shares, pulling them even lower than the overall market for the year.

Though Sainsbury’s quarterly sales at established stores dropped 0.8%, that wasn’t as bad as the average market forecast of a 1.4% fall, even if weaker than +0.1% in Q1. The group’s stock was a bit higher at the time of writing reflecting some relief, especially after a 10% fall in the quarter.

More widely, supermarket and general retail shareholders need no reminding of risks to sterling-denominated revenues and from spooked consumers. The industry is among the worst stock market performers this year.

Please click image to enlarge; source: Thomson Reuters

On a cash and leverage basis, Sainsbury’s should be favoured among the Big 3 for fastest debt reduction. However, its aggressive self-help leaves it exposed in other ways. The Competition and Market Authority’s announcement on 27th May that it will review Sainsbury’s takeover of Home Retail Group was unexpected bad news.

In all probability the CMA won’t go ahead with a full investigation, given how dicey retailing has become (CMA will decide by 25th July). But the watchdog’s informal assessment still calls into question the kind of self-help supermarkets can do (like grabbing market share in home electronics, electricals and more, which is Sainsbury’s rationale in buying Argos-owner HRG).

If diversification or consolidation hits regulatory barriers, potential growth avenues close.

In the short term, that worry caps Sainsbury’s stock (down 9% in 2016). But Brexit or Remain, in the longer term, Morrisons looks more vulnerable, after a 28% sprint in 6 months, despite losing more share market share on average over the last year than any of its rivals.