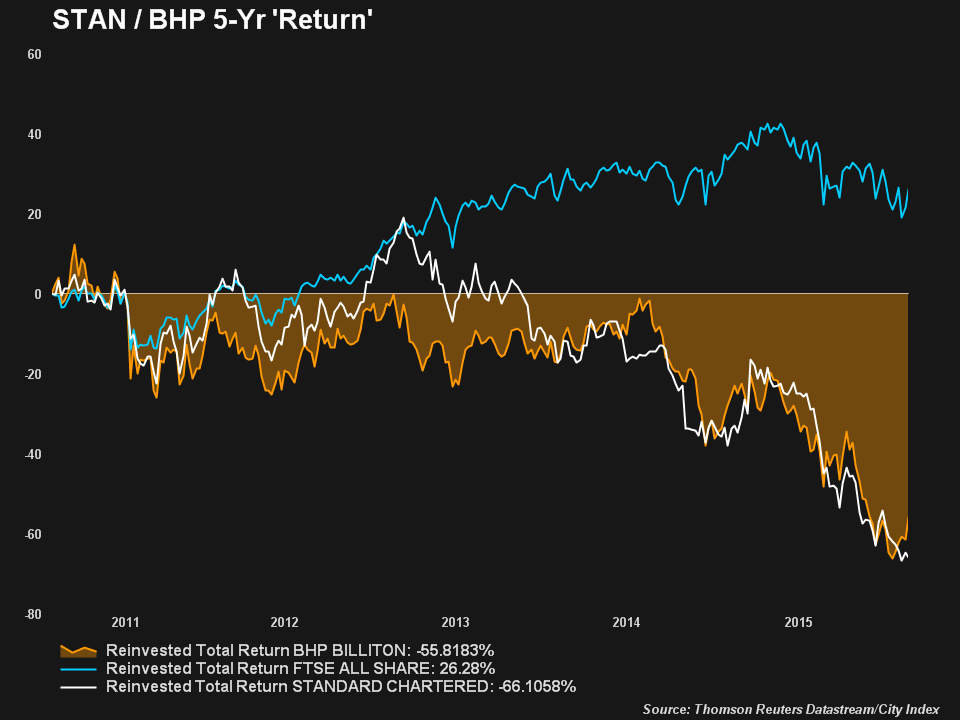

BHP and StanChart shares won t escape commodity complexity

And in a flash, it was gone… Referring to Monday’s ‘commodity complex’ rally that included resources, mining and oil shares and fanned out to […]

And in a flash, it was gone… Referring to Monday’s ‘commodity complex’ rally that included resources, mining and oil shares and fanned out to […]

Referring to Monday’s ‘commodity complex’ rally that included resources, mining and oil shares and fanned out to emerging markets too. (Honest).

Temporary respite drew to a close in synch with the latest EM/commodity bellwethers to unveil their damage from 2015, BHP Billiton, the world’s biggest miner by revenues and, Standard Chartered, the emerging-industrial lender of choice.

And damage there was.

StanChart slumped to the bottom of the FTSE 100 with a fall as harsh as 12% after profit slid 84%, year-on-year.

Billiton stock looked like it might have escaped the worst punishment after it opened higher in Australia, whilst investors mulled a 75% interim dividend cut—sharper than many expected.

BHP even touched a 7-week high in Oz, with help from a 7% jump in iron ore prices.

Later though, traders decided the diversified digger’s red ink—$5.67bn net loss vs. $4.3bn forecast—called for a re-think.

Billiton traded almost 5% lower in London, though had surged 8.6% the day before.

Aside from the pay-out capitulation—which still left BHP with a relatively generous 50% policy ratio going forward, it also announced an extensive corporate revamp.

And assuming spot prices don’t deteriorate any further—after Reuter’s Core Commodity Index tanked 100% since June 2014—BHP could theoretically generate $10bn in operating cash flow in 2016.

Iron ore price action mentioned above was promising.

Whilst there were strong seasonal and speculative factors at play, the strongest industrial metals rally for months could allow higher prices to be locked in for the medium term.

That could give a fillip to the biggest, lowest-cost miners like BHP.

StanChart upside was more difficult to spot.

Its $800m underlying profit was $100m less than expected, taking the pre-tax loss to $1.5bn.

“The challenging external environment is not an excuse for our performance. We are not unwitting victims,” its CEO Bill Winters said.

That was well in line with his notorious ‘Nuclear Winter’ caricature, tasked with clearing up decades of complacency and inefficiency.

No bonuses for his execs this year, and no dividend for shareholders either.

For Winters things may still be going according to a grim plan.

But investors are correct to worry that even when StanChart emerges at the other end of retrenchment (having dumped risky loans, reduced commodities exposure and taken a $1.85bn hit for restructuring) what then?

China’s economic transformation…OK, slowdown, and globally weak base rates are here to stay, for the foreseeable.

What will that future look like for Standard Chartered?

It is now the 34th global bank in Tier 1 Capital terms from 33rd last year, according to thebankerdatabase.com.

The threat of localised, less-encumbered rivals, with implicit or actual state backing is real.

StanChart operating income was down 15% in 2015, ROE went a fraction negative from 1% in the year before.

The rot has stopped in capital, after rights issue pain and no dividend gain.

12.6% Tier 1 puts StanChart well ahead of its pack, with room for more if it can get shot of more loans.

But organic net income potential is harder to project.

So whilst the future looks ‘less than optimal’ for StanChart and BHP, the closer of the pair to the ‘complex’ may have a moderate near-term advantage.

Even though neither is the subject of challenging expectations after (probably) washing out huge volumes of investors in recent years.

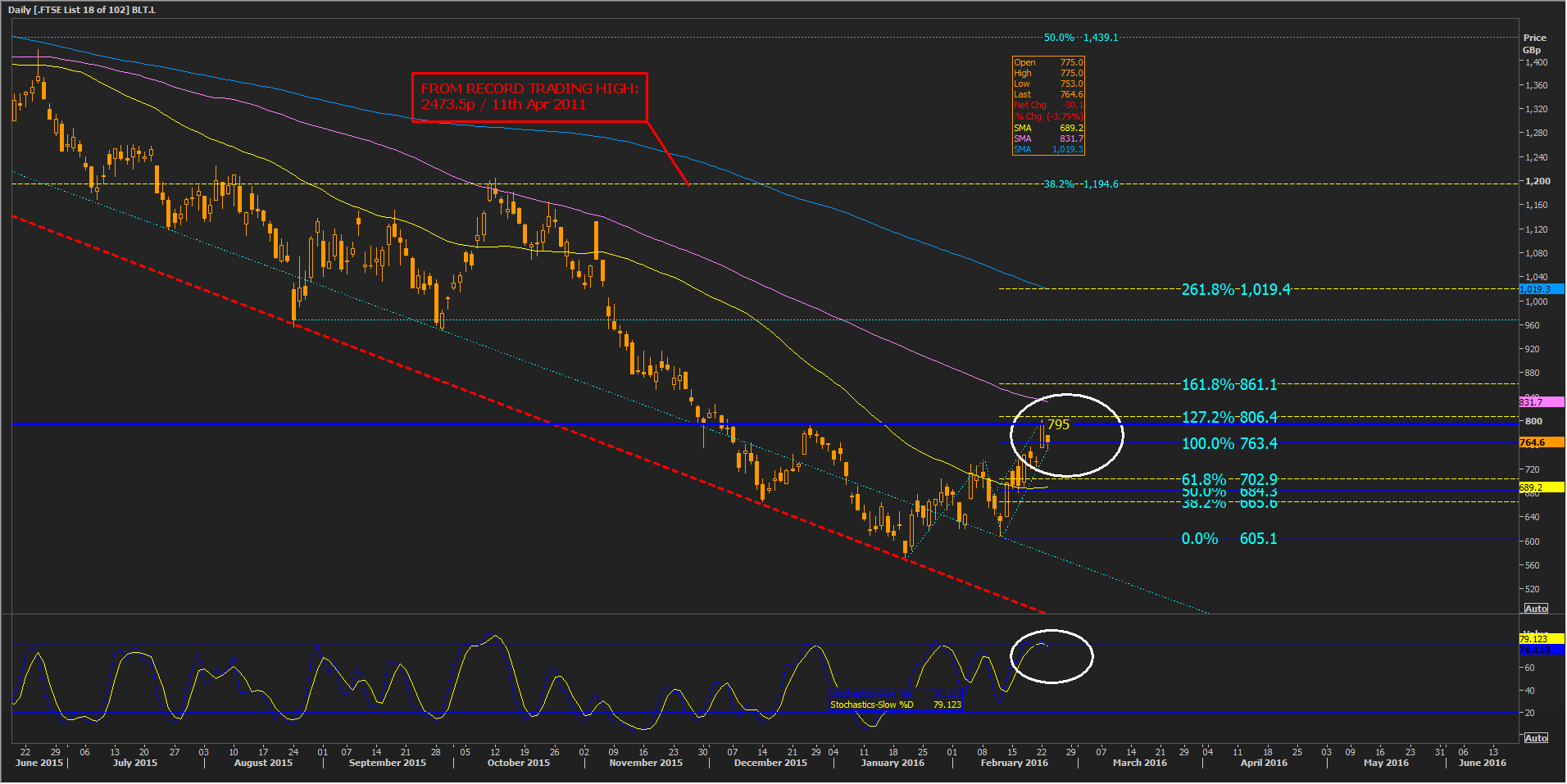

Please click image to enlarge

For BHP’s London shares, two distinct descending trends have been visible since March 2015, a weak one and a firmer one.

The shares look to be in the middle of their latest attempt to escape.

The peak of BLT’s last try was 795p and needs to be turned into a success this time (though watch out for the 127.2% interval above at 806p.)

Prospects weren’t all that impressive on Tuesday, with Slow Stochastic lines having crossed on the day before whilst ‘overbought’ and pointing lower.

Consolidation close to the 50-day moving average could create a near-term floor.

But few would rule out re-tests of the multi-year lows seen in January.

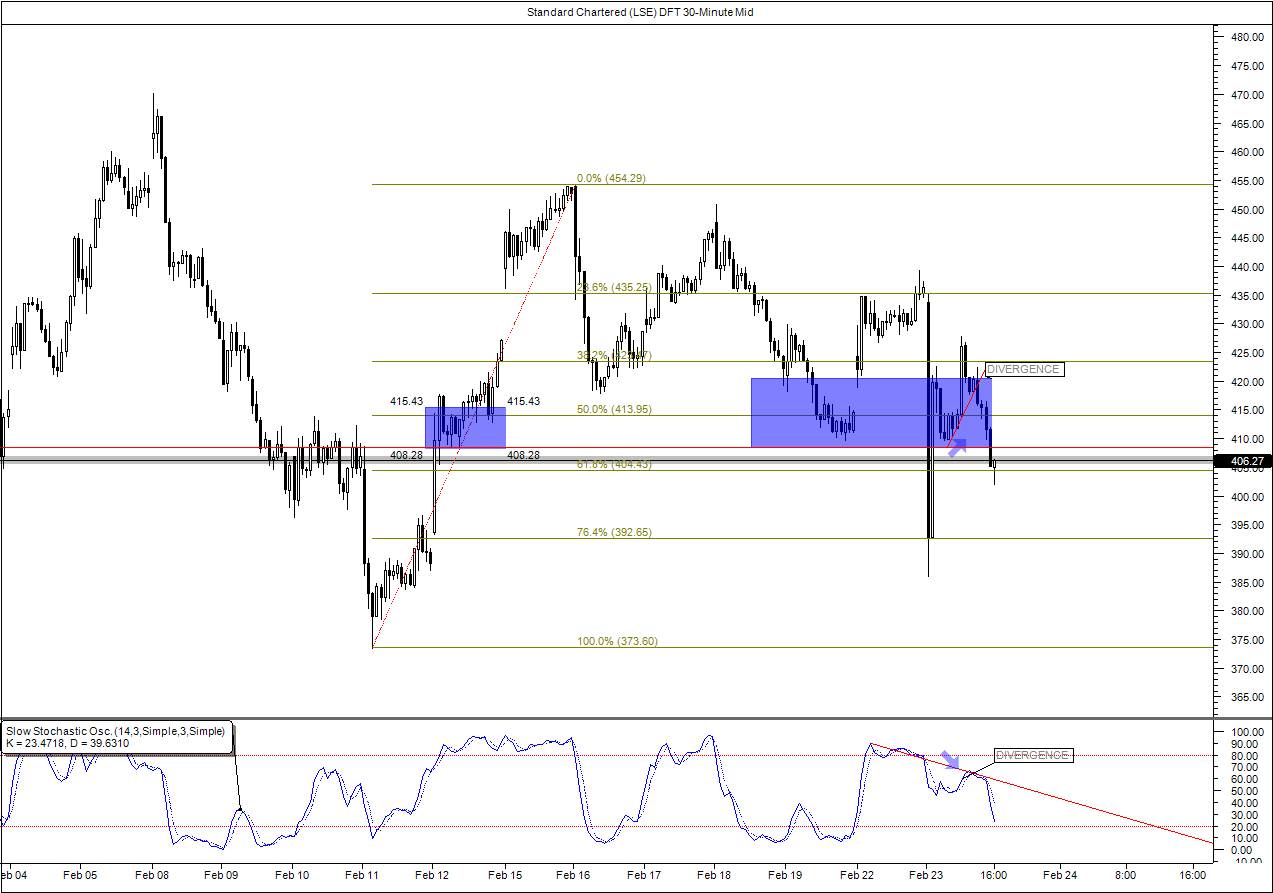

Please click image to enlarge

StanChart has been more volatile on the day, though its shares have also been hugging a clean ‘commodities-style’ downtrend—in this case since December 2013.

Traders of City Index’s Daily Funded Trade may have noticed recent resistance and support came close to Fibonacci intervals that are not the most closely followed: 23.6% and 76.4% respectively.

A support zone with a base at 408/409 looked more obvious—though even that cracked as I updated this article.

Visible price/momentum divergence in the half-hourly view suggests expectations of a complete retracement of February’s rise have good chances of near-term fulfilment.

I would not discount the less-familiar 76.4% to give the trade pause on the downside given it did this on Tuesday.

Please click image to enlarge