Balfour shares lifted to a low ceiling by overseas growth

Still under construction Balfour Beatty’s efforts to rebuild its fractured infrastructure business and reputation as a sound investment clearly have some way to go, although […]

Still under construction Balfour Beatty’s efforts to rebuild its fractured infrastructure business and reputation as a sound investment clearly have some way to go, although […]

Balfour Beatty’s efforts to rebuild its fractured infrastructure business and reputation as a sound investment clearly have some way to go, although there are promising signs in its finals.

The latest short-term negative hits come from a disappointing widening in its full-year loss to £59m from £35m, and suspension of the final dividend.

The deeper loss (£80m on an underlying basis) is worse news than the dividend cut, which had largely been expected.

That the bottom line is cratering further, including an additional write-off of £118m in its most problematic unit, UK construction, tells us the board is still in kitchen-sinking mode.

On that basis revenues ticking down by £6m to £8.79bn (+2% with currency effects stripped out) illustrates the essentially static state BBY has remained in over the year as it continues to revamp.

On the more promising side, international growth continues apace with a 24% uplift overseas (mostly from Hong Kong). That needs to be balanced by a £15m underlying loss in Middle East operations.

Most importantly, Balfour can again state that it has a net cash balance at the end of the year–with £219m on the books and assets worth £1.230bn vs. £1.035bn.

The net cash improvement is underpinned by Balfour’s affirmation today that it expects to finally be rid of the “problem” legacy projects (won during Balfour’s era of recklessly low-margin bidding) within the next couple of years.

Of course whilst such a statement provides a reassuring time frame, it also implicitly extends Balfour’s recuperation timeline by another 6 months, at least.

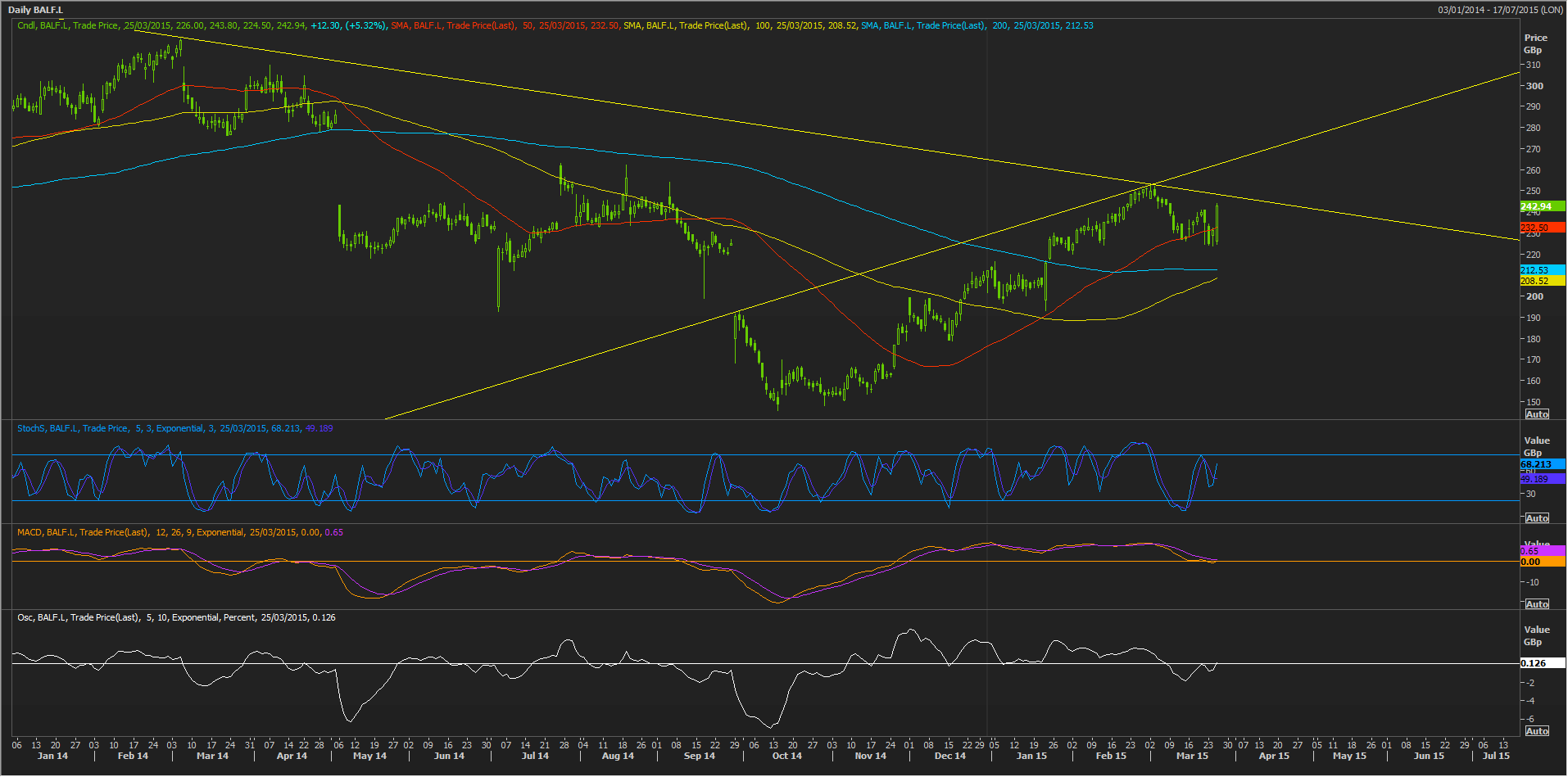

BBY appears to have stopped publishing common equity value in June last year when it was about £250m underwater by my reckoning on a tangible book value basis.

Therefore net cash on the books might well be a signal moment in BBY’s turnaround and can give its stock some room on the upside in the short term.

The shares are unlikely to be ready to break formidable wedges that have formed a ceiling over the price action for the last several years.

All things remaining equal, the current limit to the upside might well be 247p, especially with underlying momentum not that emphatic as regards the upside

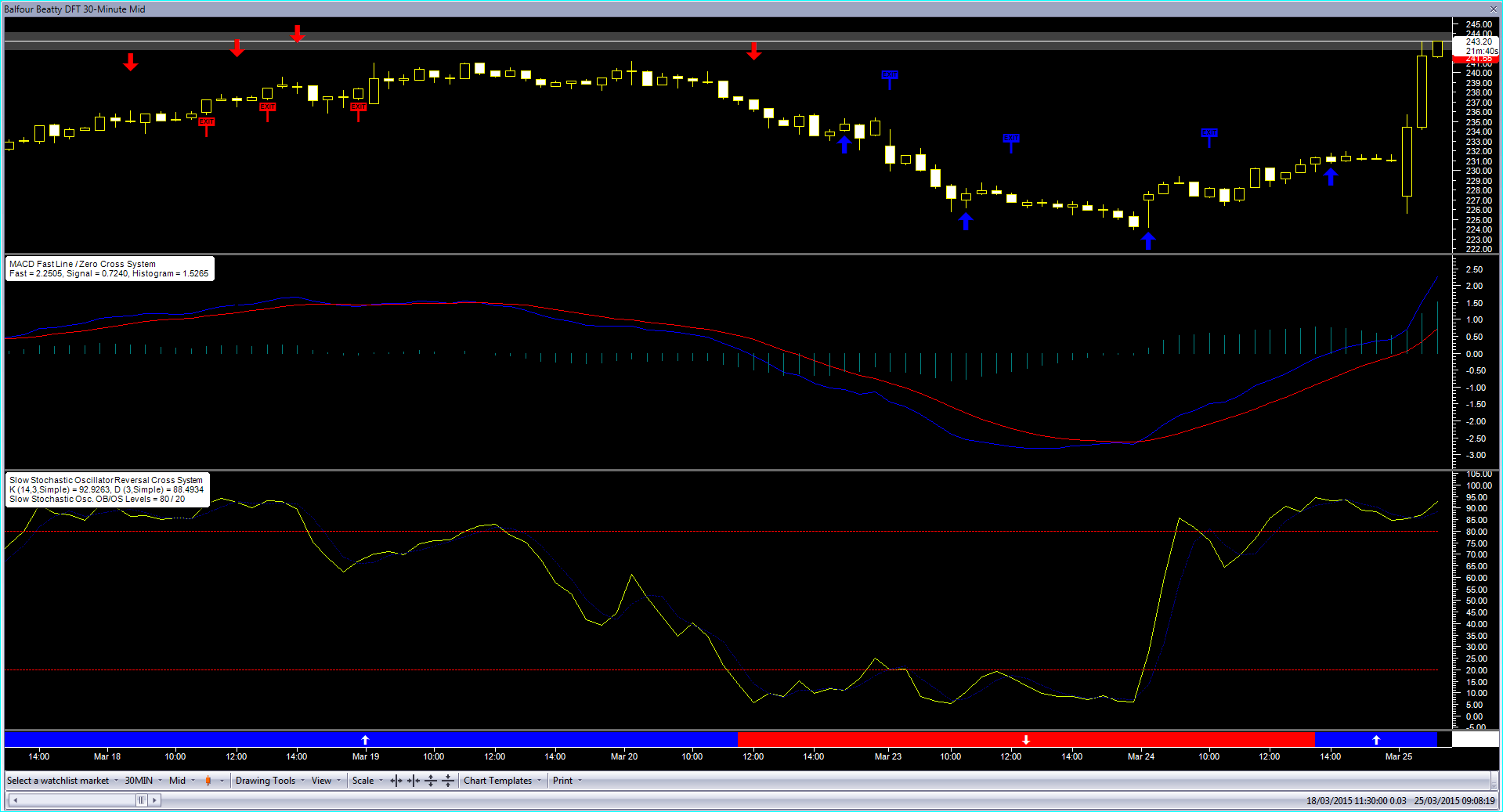

In our standard half-hourly view of trade in City Index’s most active Balfour Beatty title, the Daily Funded Trade, careful longs may have exited yesterday morning, when an overbought signal was flashed by the attached Stochastic Reversal Cross System—both moving averages ‘out of bounds’, shorter-term (blue) crossing under the longer-term (yellow).

But on an even narrower, view, Moving Average Convergence Divergence (MACD)-based trading still revealed some froth that could be skimmed off this title, and the MACD-focused system issued a theoretical ‘buy’ at 1400 GMT on Tuesday.

It has paid off.

However, overstretched tension in positive territory coupled with questionable buying momentum in the underlying in my view presents a strong risk of a lower close by CI’s DFT and in the underlying stock on Wednesday.

Current peak gains of 6.1% to 244.94p on the day are likely to be too tempting for shareholders who have been stoic enough to hang on to Balfour over the last year, and these profits will probably be taken today, in my view.