Ashraf Laidi 2015 FX outlook

Federal Reserve and the USD The Federal Reserve’s main challenge will be maintaining its intention to normalise monetary policy without risking prolonged declines in inflation […]

Federal Reserve and the USD The Federal Reserve’s main challenge will be maintaining its intention to normalise monetary policy without risking prolonged declines in inflation […]

The Federal Reserve’s main challenge will be maintaining its intention to normalise monetary policy without risking prolonged declines in inflation from plunging commodities and a surging US dollar. 2013 saw the Fed primarily using employment forward guidance to prevent bond yields from surging above 3.0%. 2014 involved the use of both employment and price guidance, recognising marked improvement in the former, while acknowledging downside risks in the latter.

In 2015, the Fed’s priority will be preventing disinflation while ensuring underemployment drops further.

Most bond traders are pricing interest rates to start increasing from Q2 2015. We think that’s too optimistic.

At its December FOMC statement, the Fed changed its language to “monitor inflation developments closely”, suggesting that downside price risks are now the Fed’s top priority. The consumer price index (inflation) showed the sixth slowdown in seven months and a 0.3% decline was the biggest month-on-month contraction since November 2008. More importantly, the Fed’s latest focus on inflation – the five-year forward rate for breakeven inflation – fell to fresh six-year lows at 2.6%, a level low enough to have brought fresh policy easing in the past. The Fed is also increasingly watching wage growth as an informal guidance for normalising policy. The important point here is that prolonged declines in the unemployment rate will not allow the Fed to raise rates if slow wage growth and low inflation persist.

Fed chair Yellen inferred that interest rates could start rising around spring or summer 2015. The case for doing so is supported by fresh six-year lows in the unemployment rate, strong services and manufacturing surveys and increased capacity utilisation. But none of these may be enough for the Fed to effect a rate hike at the risk of endangering a deflationary spiral. In the event the Fed does raise interest rates, it would likely be accompanied by a generous provision of policy accommodation such as reinvesting the proceeds of coupons from maturing bonds.

Among the most striking dynamics in currency markets has been the breadth of the rally in the US dollar. The greenback has shown advances not seen since 2005, which was the last year the currency rallied against all majors, including the Japanese yen. Unlike any of the USD advances of the past six years, when USD advances mainly reflected debt and austerity woes in continental Europe and the UK, but failing to stem the tide of JPY-bound risk aversion, today’s USD strength is about domestic US strength and the deep policy divergence between the Fed and the three other major central banks (ECB, BoJ and BoE).

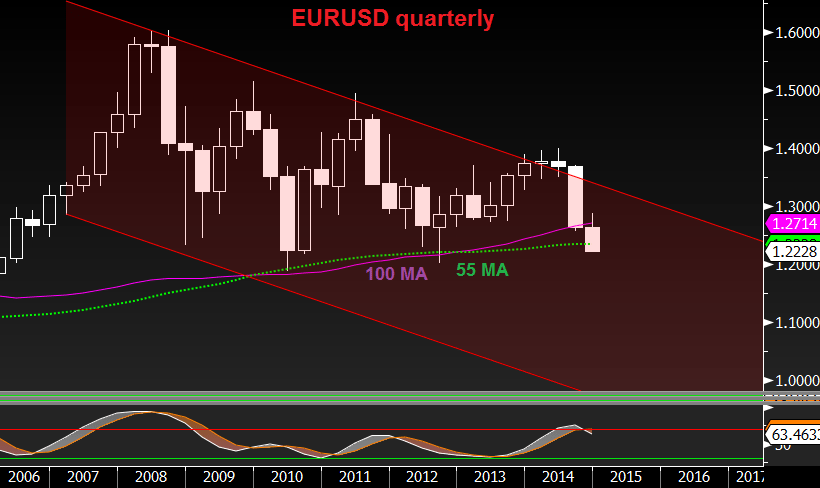

Will the European Central Bank finally join the rest of major central banks in the QE universe?

After descending in its fourth operation of long-term financing to banks and the purchasing of covered bonds and asset-backed securities, the ECB has little choice but to begin purchasing Eurozone sovereign bonds at its January 22nd meeting as a way to prevent prices from falling into deflation from their current ultra-low growth of 0.3%.

Even Germany’s figures are borderline recessionary as the latest manufacturing PMI was revised to 49.5, its weakest reading since June 2013, showing the second contraction in German manufacturing over the last three months. Germany’s IFO and ZEW surveys of investment and business sentiment ticked up in November, but the historical relationship among the three surveys indicates that German PMIs have had a better track record in leading the German business cycle than the IFO and ZEW surveys. The negative feedback loop from sanctions against Russia has also eroded demand for Germany’s valuable mid-sized companies.

Markets have good reason to anticipate outright QE in January. Not only both targeted long-term refinancing operations attracted poor demand from banks, but also ECB president Draghi is no longer regarding low inflation as a temporary occurrence. Even if Draghi fails to secure majority in the Governing Council in favour of QE in January, we expect this to materialise later in Q1 or Q2 2015. The deflationary situation will not abate any time soon.

For currency traders, the situation is becoming more straightforward. Regardless of whether QE takes place or not, Draghi has assured the ECB’s balance sheet will return to 2012 levels, which means it will increase by at least €550 bn to €750 bn over the next two years. And regardless of the policy mix pursued, euro weakness will be part and parcel of it.

PM Abe’s elections victory enables him to secure a fresh four-year cycle that would guarantee Abenomics’ hold over the four arrows of stimulative policy, including more asset purchases from the Bank of Japan. The economy slipped back into recession in Q3 after inflation slowed again. The Bank of Japan has already expanded its monetary base by 80 trillion yen per year from the previous 60-70 trillion yen. It also plans to increase the purchase of exchange-traded funds by about three trillion yen and real estate investment trusts by about 90 billion yen annually.

Japan’s Government Pension Investment Fund has finally moved to implement the long-awaited rebalancing of its investment portfolio. The world’s biggest pension fund will boost its holdings allocation for both local and overseas stocks to 25% each from 12%. Allocation to foreign bonds will rise to 15% from 11% and domestic debt allocation will fall to 35% from 60%. The early phase of the rebalancing has been instrumental in contributing to the Q4 slump in the yen. We expect fresh yen-selling as the portfolio shift progresses further.

Despite the anticipation of massive flows out of Japanese yen and 80 trillion yen in annual bond purchases by the BoJ, raising inflation would be a mirage if companies fail to increase wages and salaries. In 2013, big companies agreed to increase wages by an average of 2.3%, which was the first time annual wages had been hiked by more than 2.0% since 1999. But more will be needed as nominal wages continue to fall faster than inflation despite improved labour productivity. PM Abe and BoJ’s Kuroda will continue to pressure companies in stepping up wage growth and corporate windfalls from the 27% depreciation in the yen of the past two years.

Abe’s sales tax delay did not go unnoticed by the credit rating agencies. The delay of an additional sales tax to 2017 may have been good news for consumers but not for government revenue. National debt equals 240% of GDP, businesses and consumers remain cautious to spend. On December 1st, Moody’s downgraded Japan’s sovereign rating to A1 from Aa3, followed eight days later by Fitch decision to place Japan on downgrade watch. With both agencies’ rating standing one notch below Standard & Poor’s AA-, this means S&P could be the next agency to downgrade, especially that it hasn’t changed its rating since February 2011.

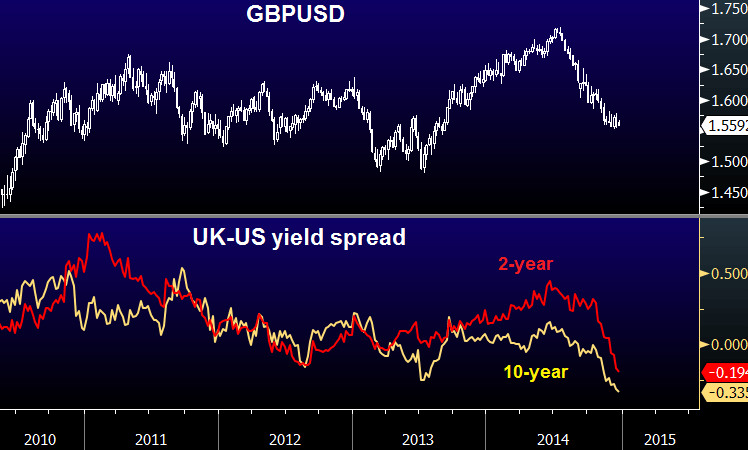

2014 was a tale of two halves for the British pound, unleashing a powerful rally in the first seven months, courtesy of returning growth, UK-bound capital flows from Europe, East Asia and the Middle East and expectations of monetary policy normalisation. But the second half of 2014 saw falling inflation, retreating business activity and escalating political uncertainty.

As UK inflation endures a prolonged decline below the BoE’s 2.0% target, sterling will not be in a hurry to recover lost ground against the USD. Two of the nine members of the BoE’s monetary policy committee continue to vote for keeping rates unchanged, with the usual two hawks (Weale and McCafferty) demanding higher rates. If the majority of MPC members were deemed hesitant in raising rates in 2014, then further fiscal consolidation and lower tax receipts will reduce the case for a 2015 tightening.

At a 12-year low of 1.3%, UK inflation is expected to further diverge from the BoE’s 2.0% target and fall below 1.0% as the contraction in food and energy prices filters through retail prices. The BoE’s latest take on inflation coupled with the November figures have pushed out expectations for the first rate hike to occur in Q1 2016 from Q4 2015.

The autumn statement revised down borrowing and the deficit for 2014-15 and 2015-16, but government tax receipts are also expected to fall, coming in £23 bn lower in 2014-15 than expected in March. Growth of income tax and national insurance has slowed to 1-2% from pre-crisis levels of 6-7%. Falling oil revenues have also weighed on receipts, in terms of both volume and price. And despite falling unemployment, low wage growth was another major element of lower income tax receipts, particularly highlighted by the increase in personal allowance i.e. the tax-free portion of income that’s exempt from tax.

Uncertainty is becoming near certainty in Westminster, stemming from the Conservatives’ loss of MPs to the anti-EU UK Independent Party and the plummeting popularity of the Lib Dems. The unlikelihood of Tory/Lib Dem coalition securing majority at the May elections means that the only way for Tories to retain majority is to strike an unlikely coalition with Labour, since striking a deal with UKIP is out of the question. Any improvement in UKIP’s polling would be detrimental to EU-UK business relations, particularly for small- and medium-sized UK companies as the party augments chances of the UK voting to leave the EU at the 2017 referendum. And with credit rating agencies already starting to warn about the risk to the UK’s sovereign rating from exiting the EU, any good news for UKIP has become an unambiguous bad news for the pound.

Unlike in 2010-2012, when tight fiscal policy operated alongside ultra-easy monetary policy from the Bank of England’s quantitative easing and the pound’s stimulative depreciation, the upcoming round of fiscal consolidation emerges alongside more hawkish market expectations for interest rates and a stronger pound.

The improved correlation between the GBP/USD rate and UK and US ten- and two-year yield spreads is forcing FX traders to keep their eyes on yields, especially as the UK/US ten-year yield spread plunged to eight-year lows. And even if the Fed refrains from tightening next year, the relative interest rate expectations remain slanted against the Bank of England.

The unavoidable conclusion for currency traders is that the Bank of England will find it nearly impossible to raise rates in 2015. The fiscal-monetary policy mix will not help, and falling government revenues from North Sea oil will outweigh any windfalls for consumers.

The December announcement by the Swiss National Bank to enter negative interest rates (-0.25% on deposits) in late January was especially prompted by the collapsing rouble situation, which will inevitably trigger fresh safe haven flows into the franc and further complicate the SNB’s protection of the 1.20 EUR/CHF rate. The rate cut will be imposed on select deposits effective January 22nd, the same day as the ECB decision makes the controversial decision to begin buying sovereign bonds.

The argument that ECB’s failure to unleash QE in January would help the euro is only valid in the short-term. Any bounce from ECB disappointment could see EUR/CHF initially stabilize via a rising EUR/USD and a neutral USD/CHF, but concerns about a dysfunctional Governing Council would eventually add to the euro’s selling as was the case in December, following no QE earlier that month.

The SNB sought to use the announcement function to manage expectations and reduce CHF speculative pressure, especially ahead of renewed uncertainty in Greek elections and the prospects that anti-bailout government takes over power. It is doubtful that the SNB move will be enough. More shall be required as the tide of escalating franc-bound flows from Russia accelerates as long as Russian currency controls are not formalised.

Switzerland’s anti-deflation fight is just getting started; franc weakness against USD remains the preferred strategy despite periodic bouts of USD pullbacks. The chart above suggests EUR/CHF will revisit the 1.2000 level ahead of the Greek elections, ECB decision and renewed shenanigans with the rouble. Perhaps the SNB action becomes a warning to the usual CHF-bound speculation in times of renewed oil-selling. But in order for traders to respect the 1.20 franc, a fresh dosage of announced intervention will be necessary. Once that occurs, USD/CHF could retest the parity resistance and extend towards the next test of 1.0151–the 100-month average, last reached in December 2002.

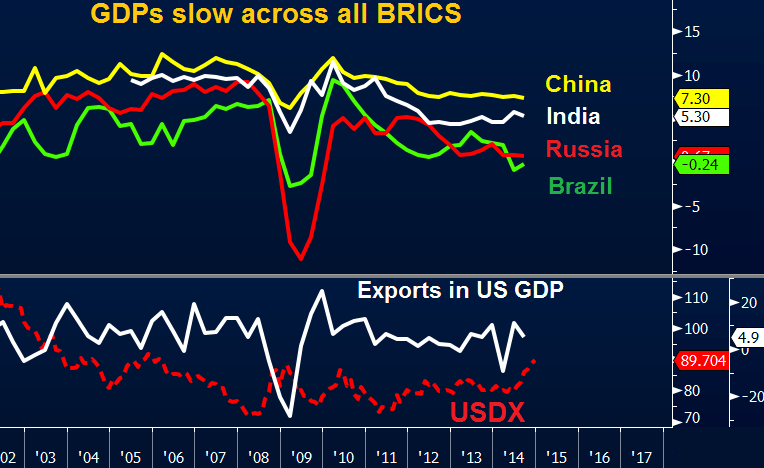

China’s prolonged economic slowdown continued to be manifested in all sectors, until the government revised down its annual growth target to 7.0% from 7.5%. Persistent weakness in retail sales and consumer credit is accompanied by 13 months of producer-level deflation and a five year low in consumer inflation. Fears and warnings of a China hard landing are their most credible status since misplaced warnings began in 2009.

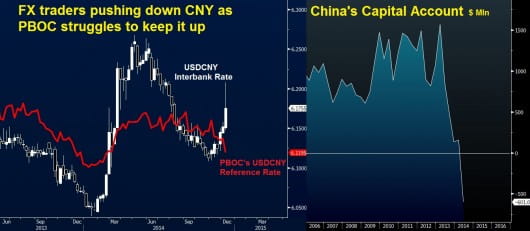

In 2014, FX traders spent the year dwelling on the machinations of the major central banks and on tumbling commodity prices. In 2015, traders will draw more focus to the People’s Bank of China and its weakening currency will be a high profile theme to watch. The Chinese yuan fell by more than 5% against the USD in late Q4 2014. We do not rule out another 7-10% decline in the yuan, which carries the risk of triggering outright deflation in the global economy as Chinese goods become cheaper to buy for foreign firms or individuals, cheapening export prices.

The People’s Bank of China is increasingly resisting traders’ weakening of the Chinese yuan, by announcing a higher rate in its daily central reference rate. But as Chinese data continue to weaken across the board, FX traders have no choice but to bet against the yuan (pushing up the USD/CNY rate). Further CNY depreciation will make Chinese products cheaper in Europe and the US, thereby further dragging down prices and potentially igniting disinflation. The chart below highlights China’s deteriorating capital account balance, which tumbled to a negative $601 million in Q2 as a result of surging capital outflows. Five years ago, China worried about rapid foreign capital flows making its currency too weak. Today, it worries about the opposite and the figures show it.

China’s November decision to cut its benchmark interest rates for the first time in two and a half years reflects the recent deterioration in economic data. The PBOC slashed its one-year deposit rate by 0.25 % to 2.75% and its lending rate by 0.4 % to 5.6%, driving down the spread between both rates to 2.85%, the lowest in 16 years. With GDP and inflation both at four-year lows, Chinese authorities cannot content themselves solely with reducing the required reserve ratio on banks as was the practice in 2011-12. Cutting lending and borrowing rates as well as banks’ required reserve ratio sends a more potent signal about the resolve of the PBOC. More CNY weakness looms large.

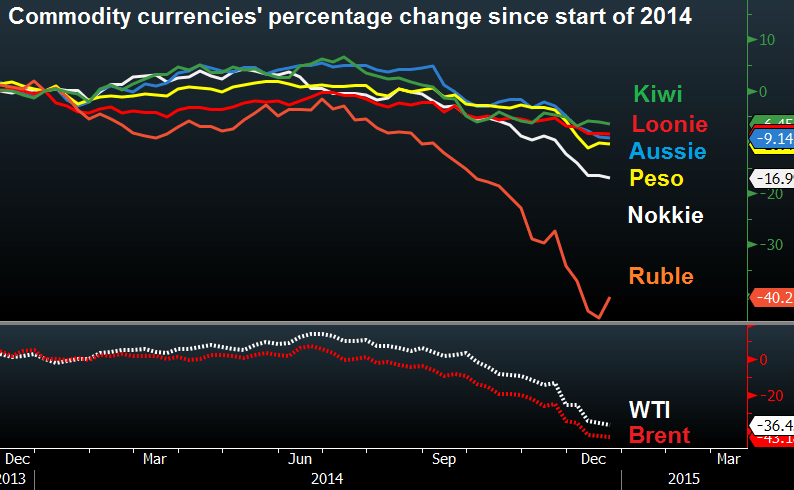

As oil fell for six straight months in the second half of 2014, plunging 47% to post its biggest decline since the 2008-09 crisis, the reaction in energy-dependent currencies has yet to unravel. The worst performing currencies so far have been the Russian rouble, down 43%, followed by the Norwegian krone and the Mexican peso at -16% and -12% respectively. The carnage in energy commodities and sell-off in metals were largely to blame. The dual among the most liquid currencies remains between the Australian and Canadian dollar as both have dropped 8% against their US namesake.

Aussie woes began in September when the currency could no longer ignore aggressive jawboning from the Reserve Bank of Australia, deteriorating fundamentals from China (shenanigans in credit markets and accelerating declines in metals) and improving dynamics in Canada and the US. Once the Aussie’s decline caught “down” with the Aussie, the performance became at par. Aussie yield differentials could deteriorate further on potential RBA action later in the year. The Reserve Bank of Australia is increasingly expected to cut interest rates in 2015.

The Aussie’s challenges are mainly highlighted by the 50% plunge in the price of iron ore, which accounts for 20% of Australia’s export revenues. Aside from other AUD-negative factors, such as Aussie consumer confidence hitting three-year lows and RBA governor Glenn Stevens aggressively talking down his own currency, the elephant in the Australian economy is China, which buys 35% of Australia’s physical exports. These are led by iron ore, followed by coal.

China had 42 consecutive months of negative produce price deflation, while consumer inflation hit a fresh five-year low. Prolonged manufacturing overcapacity and price cutting pressure on retailers are to blame. Once corporate China starts to feel the bite of eroding profit margins, job growth will further slow and weigh on the all-important household income growth. These intensifying signs of China’s slowdown, coupled with the RBA’s jawboning onslaught have bolstered the case for Aussie bears.

In the first two months of 2014, the Canadian dollar was sold off across the board on various reports from hedge funds, highlighting that Canada’s housing market was overdue for a correction as home prices were deemed overvalued by as much as 10%. But Canada’s economy and its currency defied those worries as the Bank of Canada remained the only G8 central bank to not descend into quantitative easing, leaving its overnight rate at 1.0%, higher above the rest, and unchanged for a record 65 years. CAD was the best performing “energy currency” in 2014 among industrialised nations’ currencies.

The loonie’s remarkable resilience in the face of collapsing oil prices is highlighted by monetary policy and resource diversification. The erosion in oil prices will undoubtedly impact Canada’s oil revenues, but tightening labour markets and better readiness to adapt to the slowdown in mining, than Australia for instance, will help slow selling pressure on the loonie in the event of a renewed attack on oil prices.

Canada’s mining and energy accounts for a third of exports, half that of Australia’s exposure to the ailing sector. Unlike Australia’s exposure to the slowing China, Canada’s dependence exposure to the US offers it the benefit of a falling loonie and a recovering US economy. The CAD too suffered from the occasional jawboning from BoC governor Poloz. Yet, Canada’s avoidance of QE could help the currency gain the title of “next best choice after the USD” as long as no growth shocks occur south of the border.

If you found this article useful, you might also want to read Ashraf’s other article on the dangers of underestimating deflation, Kelvin Wong’s notes on US stocks to watch next year and James Chen’s technical analysis of indices, currencies and commodities for 2015.